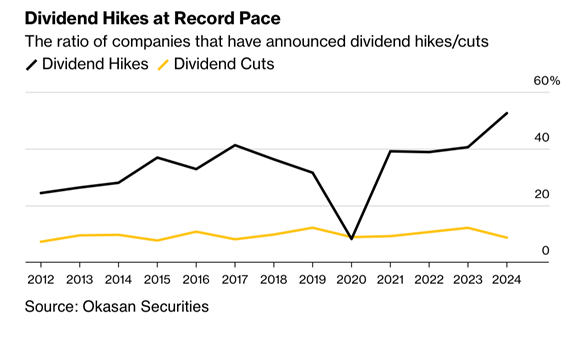

There are clear economic and investment tailwinds blowing across Japan right now. The land of the rising sun has enjoyed rising equity prices in the last few years as its currency weakens substantially. The Bank of Japan’s hand may further be forced, given that it was recently reported that the world’s fourth-largest economy endured a third consecutive quarter of negative GDP growth.

Still, both the Nikkei and Topix are in long-term uptrends despite pullbacks from their Q1 2024 peaks. What’s more, Warren Buffett has come out bullish on Japan, and firms on the island country have been increasing dividends at a torrid pace over the past 12 months.

I reiterate a buy rating on Toyota Motor (NYSE:TM). I see shares as undervalued with EPS upside ahead, while its technical chart shows price approaching key support.

Japanese Companies Raising Dividends

Bloomberg

According to Bank of America Global Research, Toyota is one of the world’s largest automakers and operates in Automotive, Financial Services, and All Other segments. It contends with global leaders VW Group and GM in sales volume. Following the 2008 financial crisis, TM struggled with quality issues in the US and production cutbacks due to Japan’s earthquake, but regained top global market share in 2012. The US market is its traditional earnings driver, but it has tapped into emerging markets such as ASEAN and India. TM boasts the highest domestic production rates of Japan’s big three (Toyota, Nissan, Honda).

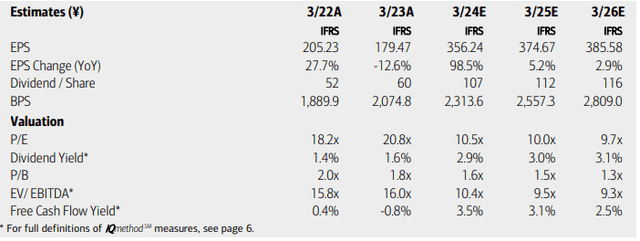

Earlier this month, Toyota reported FY GAAP EPS of ¥365.94 while revenue of ¥45095.32 billion was up 21% from year-ago levels. Operating profit jumped 96% year-on-year, with a very strong operating margin of 11.9% for the global automaker. Consolidated vehicle sales reached ~9,443,000 units, up 621,000 units from the previous year.

Toyota offered color on geographic highlights: There was a significant increase in vehicle sales and operating income in North America and Europe, while sales in Japan declined slightly. In its quarterly release, the management team said it looks to improve its position by increasing investments in its labor force and production efficiency.

Toyota seeks to capitalize on growing consumer interest in hybrid vehicles (and the related drop-off in EV). What’s more, within the release, Toyota announced a share buyback plan of up to ¥1 trillion, potentially reducing the outstanding share count by 520 million shares, per BofA. For FY 2025, the company now expects sales revenue of ¥46 million with earnings per share attributable to Toyota Motor of ¥264.95 (basic).

On valuation, analysts at BofA see earnings rising about 5% this year and inching up another 3% in the out year, though those numbers will likely be revised following TM’s updated guidance. With FY 2025 now just getting underway, the bottom line is seen easing from a major jump in FY 2024, but during the earnings announcement, the management team said that the pause was in an effort to strengthen its foothold in the industry, so I don’t see the EPS drop as part of normal operations.

The Seeking Alpha consensus estimates show $22.18 in non-GAAP EPS on the ADR shares (about ¥3500), and that figure is expected to hold about steady through next year. Dividends, meanwhile, are expected to increase at a high rate through FY 2026, offering shareholders a normalized yield near 3%. With a low earnings multiple and solid free cash flow, fundamentals appear strong for the OEM.

Toyota: Earnings, Valuation, Dividend Yield, Free Cash Flow Forecasts

BofA Global Research

If we assume normalized operating per-share earnings of $22 and apply a 12 multiple, between TM’s 5-year average and the sector median, then ADR shares should trade near $264, unchanged from my valuation call earlier this year.

Even if the profit growth narrative is not the best, shareholder-friendly moves like the recent buyback announcement should help support the stock price.

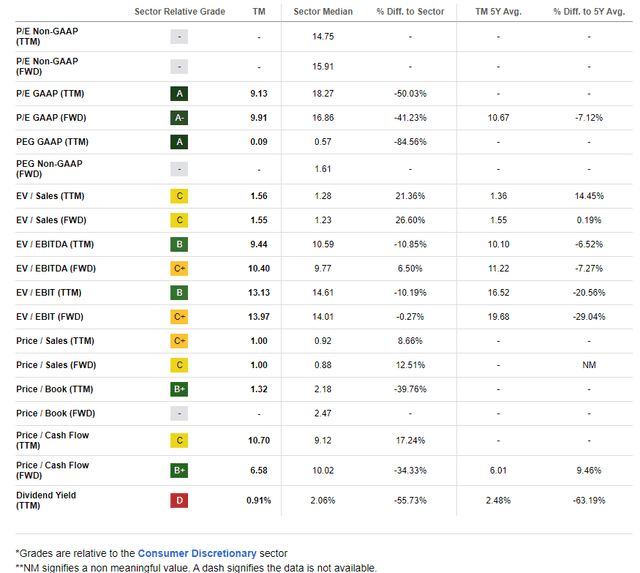

Toyota: Remains a Value, Strong Free Cash Flow

Seeking Alpha

Compared to its peers, TM features a solid valuation rating, while its recent growth trajectory has been stellar. Of course, much will depend on Toyota achieving its guidance targets and executing share-repurchase initiatives.

Either way, the firm is known for its steady profitability trends and efficient operations, and share-price momentum has been decent in the last handful of months. Finally, while the EPS revisions grade is weak, there has been just a single sellside downgrade in the last 90 days.

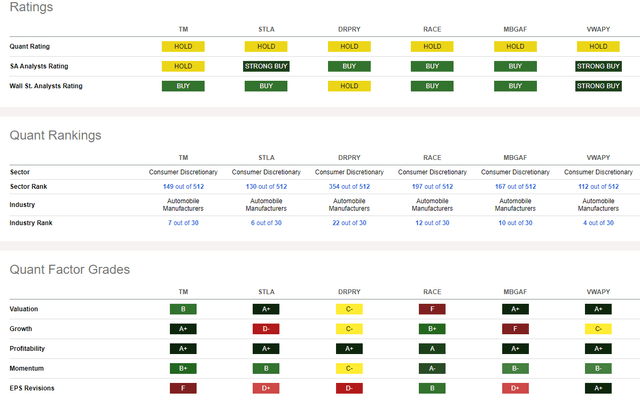

Competitor Analysis

Seeking Alpha

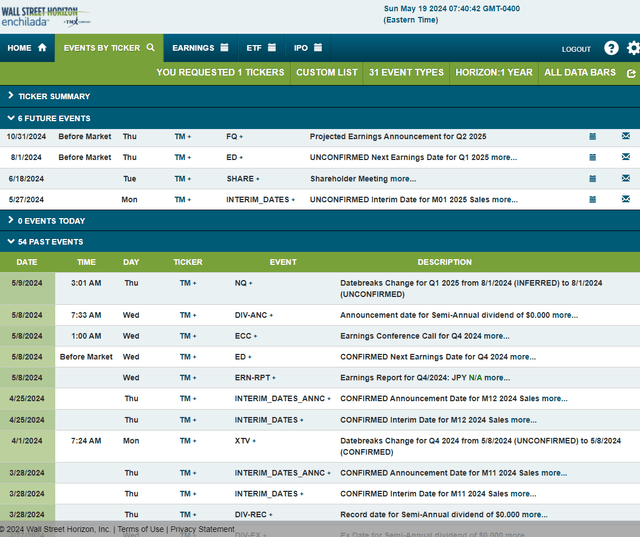

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q1 2025 earnings date of Thursday, August 1 BMO. Before that, the company will report monthly auto sales interim data on Monday, May 27. Toyota also hosts its annual shareholder meeting on Tuesday, June 18 which could also bring about volatility in the stock price.

Corporate Event Risk Calendar

Wall Street Horizon

The Technical Take

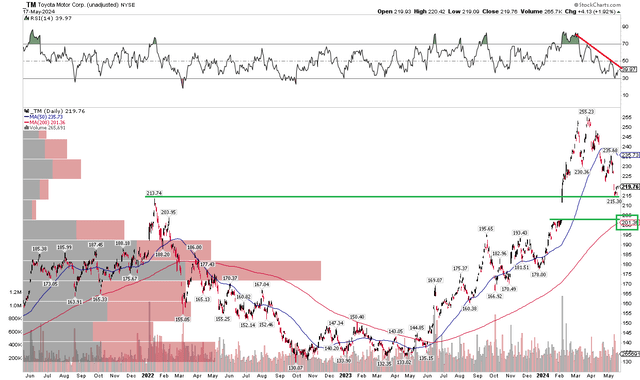

With a reasonable valuation and shareholder-first policies, Toyota’s technical view is intriguing right now. Notice in the chart below that shares neared my intrinsic value target earlier this year, but have since retreated to key support. I expect buyers to step in the $210 to $215 range – $213.74 was the previous high from early 2022. Also, there is a gap in the ADR price chart which could get filled in the low $200s – very close to where the rising 200-day moving average comes into play today. So, there’s a confluence of reasons why there could be limited downside from here.

Also, take a look at the RSI momentum indicator at the top of the graph – it is mired in a downtrend, which is not encouraging. So, a bit more downside in price could be in the cards. But with a rising long-term 200dma, the bulls still command control of the primary trend.

Overall, TM is at a favorable risk/reward spot on the chart today in my opinion.

TM: Shares Fall To Support as Momentum Dips

Stockcharts.com

The Bottom Line

I reiterate a buy rating on Toyota Motor. Despite the intentional profit-growth pause in FY 2025, I see the automaker as a decent value today, while shareholder-friendly activities should offer support for the stock.

Read the full article here