They who can give up essential liberty to obtain a little temporary safety deserve neither liberty nor safety.“― Benjamin Franklin.

It has been more than a year since our initial look at Paysafe Limited (NYSE:PSFE). We concluded that article by passing on any investment recommendation for the stock at that time due to the company’s heavy debt load and some other headwinds. The company did report better than expected results in its most recent quarter and also raised forward guidance, making this a good time to circle back on Paysafe Limited. An updated analysis follows below.

Seeking Alpha

Company Overview:

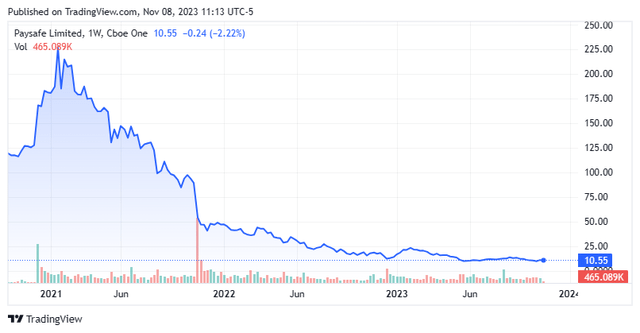

Paysafe Limited is headquartered in London, England and operates via two business segments: Merchant Solutions and Digital Wallets. The company operates a payments platform for merchants and consumers in the entertainment sectors that enables businesses and consumers to connect and transact seamlessly through capabilities in payment processing, digital wallet, and online cash solutions. The stock currently trades at around $10.50 a share and sports an approximate market capitalization of $650 million.

Second Quarter Results:

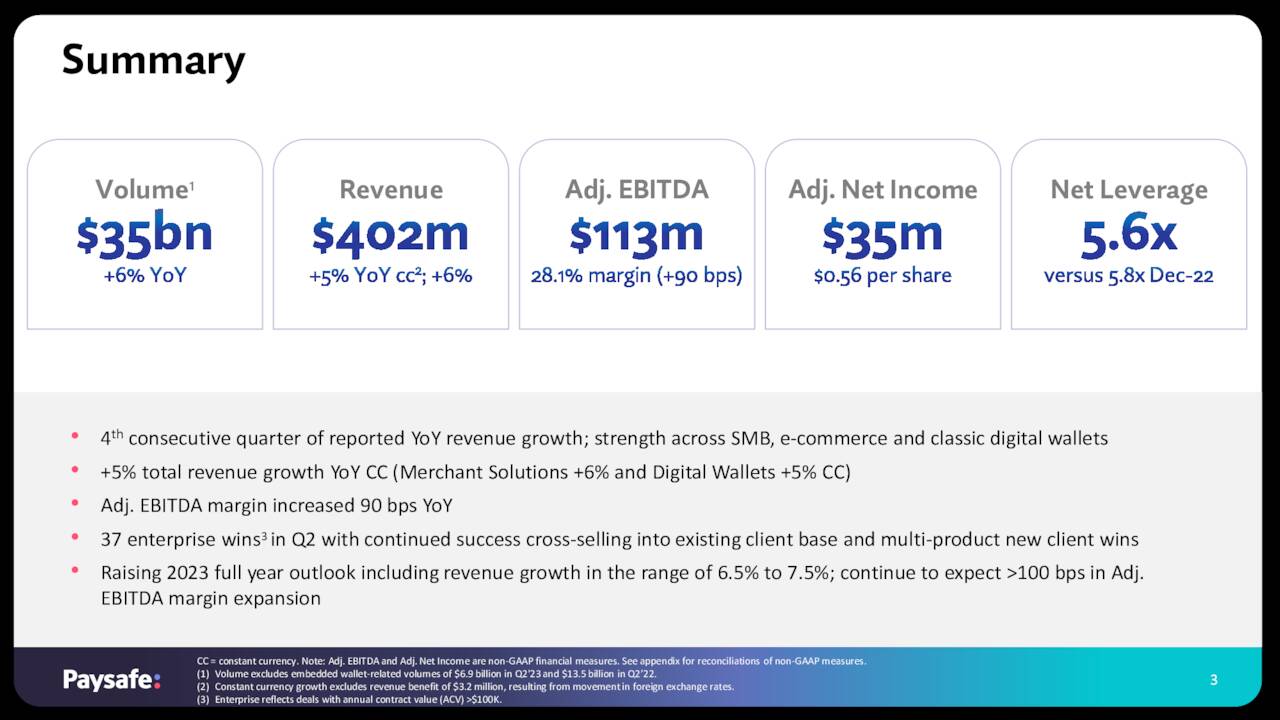

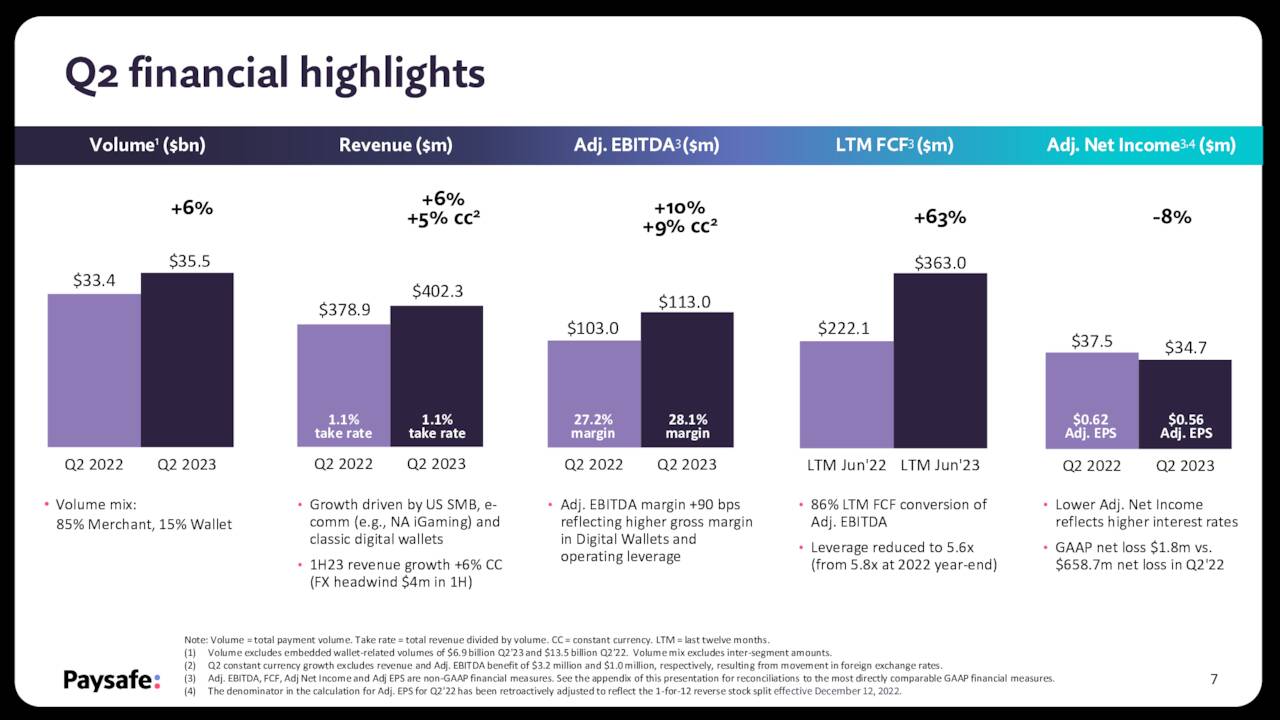

The company reported its second quarter numbers on August 15th. Paysafe delivered non-GAAP earnings per share of 56 cents, nearly double estimates. Revenues rose just over six percent on a year-over-year basis to just over $402 million, some $7 million above the consensus. Payment volume rose 6% y/y to $35.5 billion. The company attributed the stronger numbers to small business and ecommerce growth, particularly from North American gaming volume.

August Company Presentation

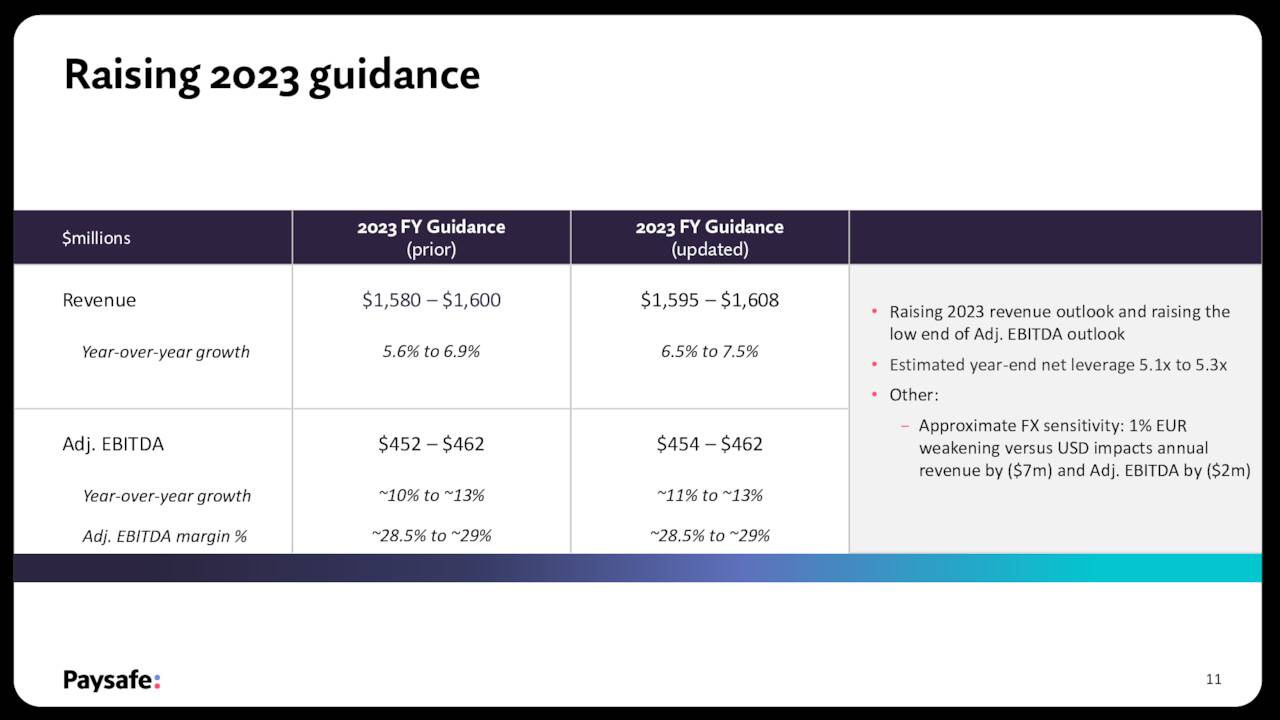

Leadership raised full year guidance calling for between 6.5% to 7.5% sales growth for FY2023 and stating its Adjusted EBITDA margin should grow by at least 100bps for the year.

August Company Presentation

Management bumped up its FY2023 EBITDA range to $454 million to $462 million from $452 million to $462 million as well.

August Company Presentation

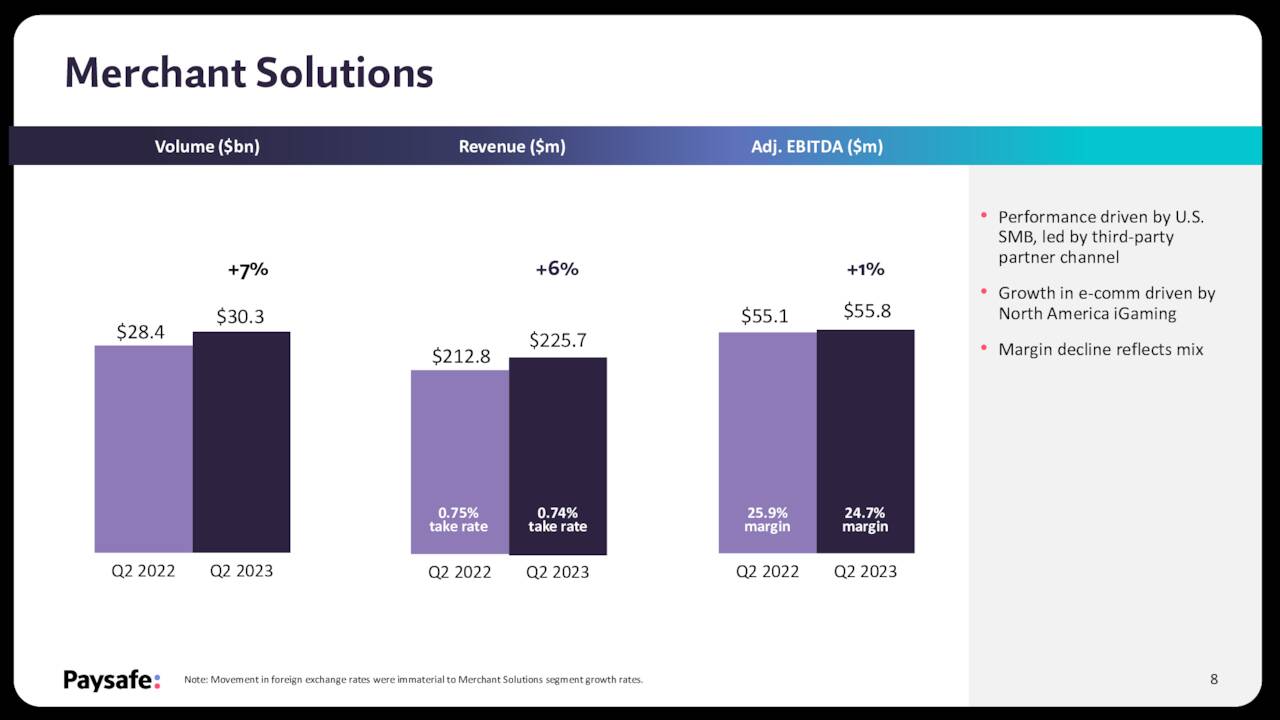

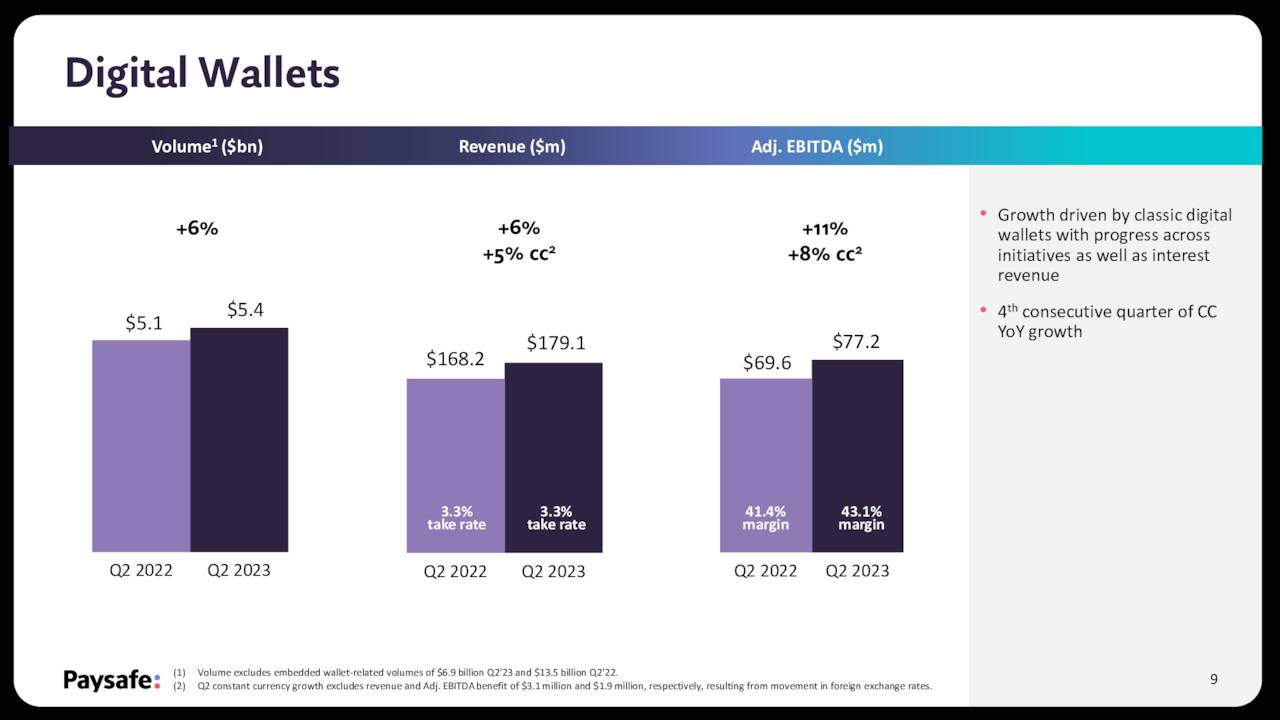

The company got solid performances from both of its main business segments.

August Company Presentation

August Company Presentation

Analyst Commentary & Balance Sheet:

Despite better than expected second quarter results, the analyst community is still negative on Paysafe’s prospects with the exception of BMO Capital, which reiterated its Buy rating and $64 price target on PSFE soon after second quarter numbers hit the wire. However, RBC Capital ($19 price target) and Susquehanna ($16 price target, up from $15 previously) reiterated their Hold ratings on the stock the same week Q2 results were posted.

Then, on October 20th, UBS initiated the stock as a Sell with a $10 price target. The analyst at UBS gave the following reasons for the negative outlook on the company.

Software-led distribution is increasingly becoming the channel required to participate in the 70% of industry revenues sourced via underlying small businesses, of which the vast majority could ultimately be running through a software platform longer-term. Those best positioned will either be owners of the software or the preferred partners to these software companies in embedding and monetization-enhancing financial services across multiple channels, products, and geographies.“

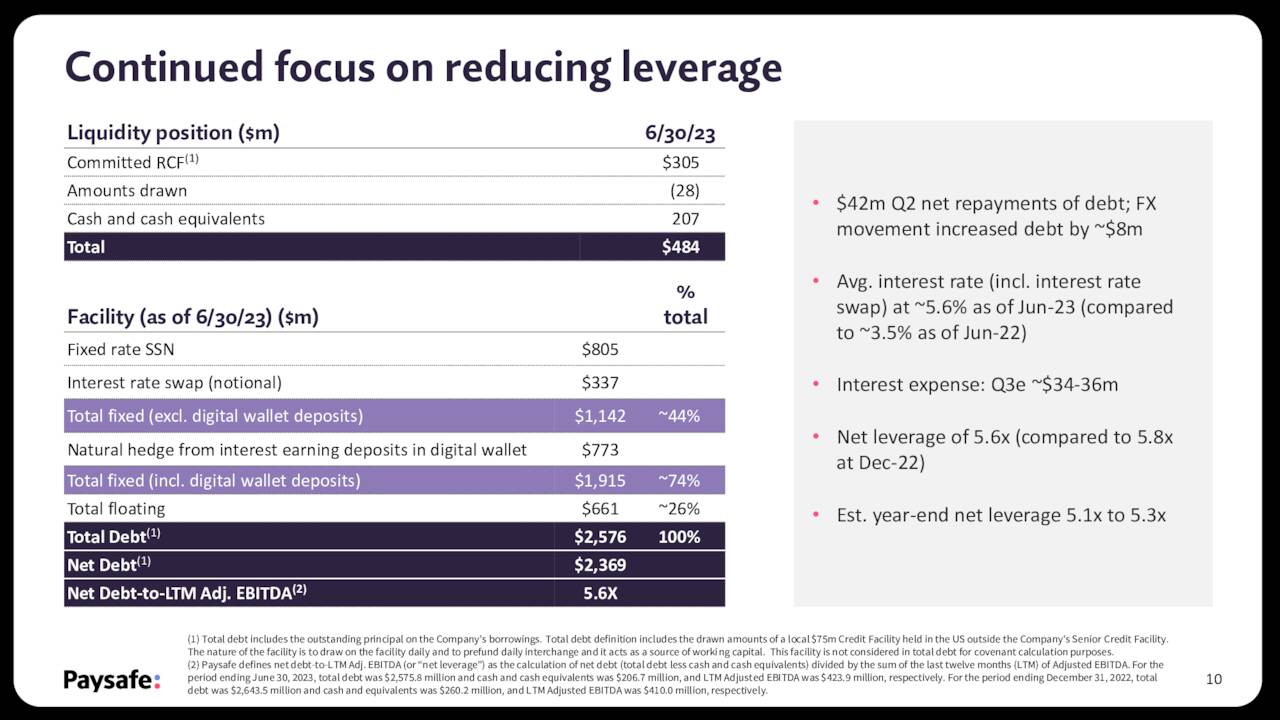

Just over four percent of the outstanding float in the shares is currently held short. The company ended the first half of the year with just over $205 million worth of cash and marketable securities against $2.6 billion in long-term debt. Paysafe did produce free cash flow of $94.7 million during the second quarter, up substantially from just under $40 million in 2Q2022. Net leverage also fell to 5.6x from 5.8x at the end of FY2022. Leverage is expected to drop into the 5.1x to 5.3x range by the end of this fiscal year.

August Company Presentation

Verdict:

Analyst firm estimates varied widely on this stock. They range from a loss of 13 cents a share to a profit of 46 cents a share in FY2023 on seven percent sales growth. They project anywhere from 32 cents to $2.38 a share in earnings in FY2024 on similar sales growth.

The company appears to have made some significant progress since we last looked at it. Debt has been pared down some along with leverage, and free cash flow has much improved. However, the company’s overall debt load still is substantial in an environment of rising interest rates. The analyst community is quite negative overall on the company’s prospects and profit estimates are all over the place. The stock also had a reverse 1 to 12 stock split last summer and came public via a SPAC, a channel that has destroyed a huge amount of shareholder value in recent years.

Given that, I am still passing on any investment recommendations around Paysafe Limited. Investors will get a fresh set of data points on the company when it reports Q3 results next week (expected pre-market November 14th), it should be noted as well.

The desire for safety stands against every great and noble enterprise.”― Tacitus.

Read the full article here