ITT Inc. (NYSE:ITT) has had solid price action due to earnings exceeding expectations. I believe that ITT is currently a hold because although the firm has solid fundamentals regarding its core operations and financials, they are currently overvalued assuming my DCF figures.

Business Overview

ITT Inc. is a global manufacturer and distributor of specialized technological solutions and engineering key components for the transportation, industrial, and energy sectors. Motion Technologies, Industrial Process, and Connect & Control Technologies are the three business segments. The Motion Technologies business unit produces energy-absorbing components, shims, shock absorbers, brake pads, and sealing technologies, mostly for the transportation sector, which includes buses, trains, trucks, light- and heavy-duty commercial and military vehicles, and passenger automobiles.

Industrial pumps, valves, plant optimization, remote monitoring systems, and services, as well as aftermarket solutions including replacement parts and services, are all designed and produced by the Industrial Process sector. It provides services to a wide range of clients in sectors including mining, energy, chemicals, and other industrial process markets.

The Connect & Control Technologies business unit develops and produces a variety of tailored connectors and specialty control components for vital applications assisting several industries, such as energy, transportation, medical, aerospace and defense, and industrial. This segment offers control products, which include highly engineered actuation, flow control, energy absorption, environmental control, and composite component solutions for the aerospace, defense, and industrial markets. Connector products include electrical connectors, which include circular, rectangular, radio frequency, fiber optic, D-sub miniature, micro-miniature, and cable assemblies.

ITT Inc.

Financials

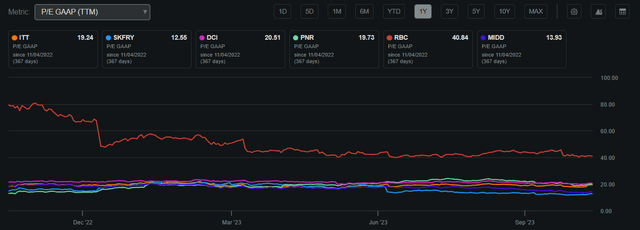

ITT’s current market value amounts to approximately $8.28 billion, accompanied by a remarkable Return on Invested Capital, resting at 16%. As for the stock price, it currently stands at $100.48 per share, exceeding its 200-day moving average of $91.24. Notably, the P/E GAAP ratio is situated at 19.24. This specific figure positions ITT at an undervalued stance relative to its industry peers, reflecting a potential for investors to consider it an attractive investment opportunity compared to its counterparts.

ITT P/E GAAP Compared to Peers (Seeking Alpha)

ITT also pays a dividend of 1.15% representing a payout ratio of 21.58% this allows the firm to create a consistent income for investors while also leaving lots of room to utilize its ROIC to improve its core business. This will create attractive value for shareholders while also having solid growth in the long term.

Seeking Alpha

Performance Compared to the Broader Market

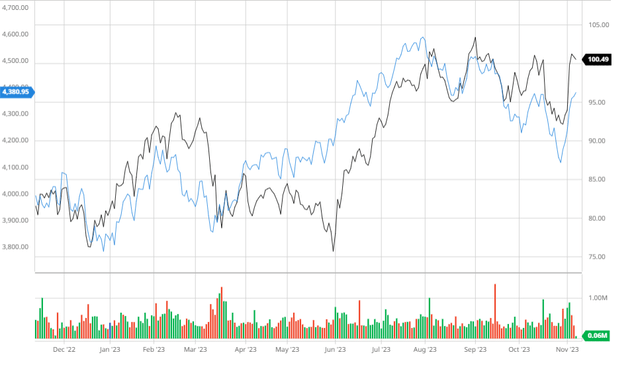

Over the past 5 years, ITT has outperformed the S&P 500 when adjusting for dividends. I believe that this is due to ITT’s allocation of FCF to create value for shareholders through business expansion and income. This outperformance demonstrates management’s ability to create long-term value through several economic cycles.

ITT Compared to the S&P 500 (Created by author using Bar Charts)

Earnings

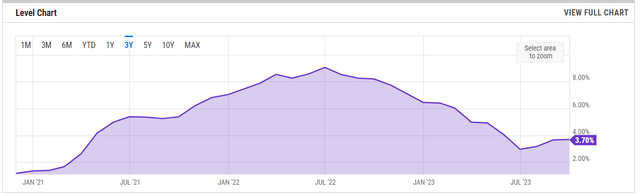

ITT reported strong Q3 2023 earnings on November 2nd with EPS beating by $0.09 at $1.37 and revenues surpassing estimates by $11.94 million at $822.1 million showing a 9.1% YoY growth. This outperformance demonstrates ITT’s ability to exceed expectations through economic headwinds and maintain solid cash flows in all environments. With EPS and revenue estimates remaining strong moving into 2024 and 2025, analyzing inflation in the near future will help us better predict volume demands from consumers. I believe that ITT’s ability to maintain solid earnings underscores the firm’s ability to create stable cash flows through diversification. As macro headwinds begin to cool off with inflation dropping and rates being held steady as shown below, ITT’s performance will only continue to improve.

Earnings Estimates (Seeking Alpha) Inflation (YCharts) Interest Rates (YCharts)

Balance Sheet

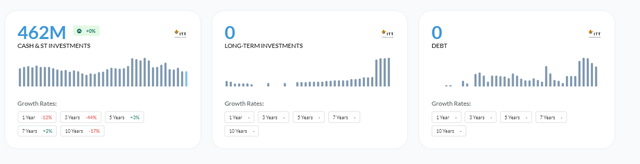

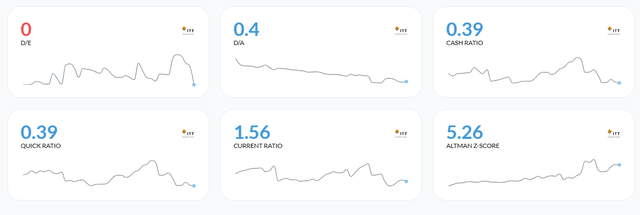

ITT’s balance sheet is also solid moving into economic headwinds with no long-term debt and a 37.19x interest coverage. This would be beneficial in times of high rates as the firm can utilize its deleveraged position and high share price to fund expansions through a lower cost of debt. With a Current Ratio of 1.56 and an Altman-Z-Score of 5.26, ITT is positioned to remain solvent in the long term.

Financial Position (Alpha Spread) Interest Coverage (Alpha Spread) Solvency Ratios (Alpha Spread)

Analyst Consensus

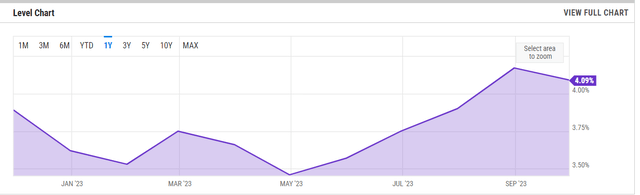

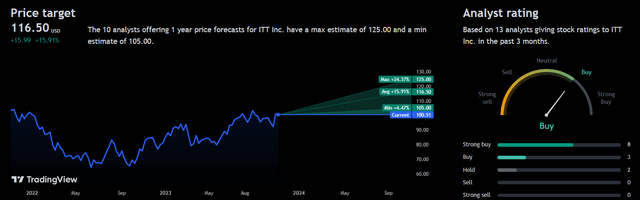

Analysts in the last 3 months rate ITT as a “buy” with an average 1Y price target of $116.5 presenting a potential 15.91% upside. I believe that analysts are bullish due to the firm’s low leverage in macro headwinds resulting in a greater ability to preserve cash flows.

Analyst Consensus (TradingView)

Valuation

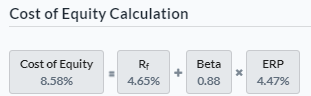

In order to find an accurate fair value for ITT, I calculated a Cost of Equity of 8.58% by using a risk-free rate of 4.65% based on the 10-year treasury yield. This represents the return demanded by investors when holding ITT.

Cost of Equity (Created by author using Alpha Spread)

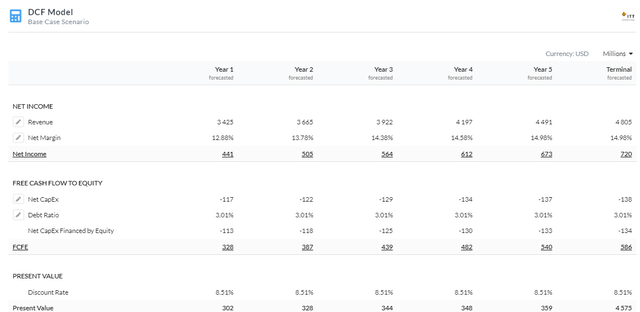

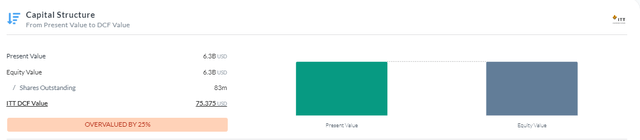

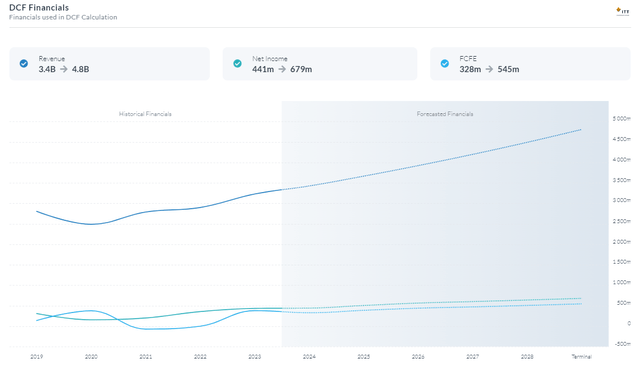

After finding an accurate discount rate of 8.51% I used a 5-year Equity Model DCF based on net income to find a fair value for ITT. I decided to maintain a discount rate of 8.51% because of the firm’s low leverage and current resilience to broad market headwinds. I also used revenue and EPS estimates in line with analyst expectations with revenues growing at mid-single-digit rates. This resulted in a fair value of ~$80.44 presenting an overvaluation of 20%. I believe that although the firm is overvalued, negative price action through broad headwinds may make ITT an attractive investment that yields solid returns.

5Y Equity Model DCF Using Net Income (Created by author using Alpha Spread) Capital Structure (Created by author using Alpha Spread) DCF Financials (Created by author using Alpha Spread)

Strategic Diversification Leading to Stabilized Cash Flows

In order to increase its resilience and profitability, ITT Inc. has taken a strategic diversification approach, entering a number of different but related businesses, including the defense sector. An example of this diversification approach is ITT’s foray into the defense sector, which offers distinct prospects as well as obstacles. ITT hopes to take advantage of development prospects in the defense industry and reduce risks related to economic volatility in other industries by forging a strong presence in the defense sector.

The creation and manufacturing of extremely specialized goods and services catered to the requirements of armed forces and defense agencies are included in the defense sector. These goods and services include a wide range of vital uses, such as night vision equipment, tactical communication systems, and other cutting-edge defense industry technologies. ITT’s involvement in this sector guarantees that its income sources are not unduly dependent on any one market, which is essential for stability in the fast-paced corporate world of today.

ITT’s diversification in the defense industry is demonstrated by the coil springs it supplies to defense and military organizations. Coil springs from subsidiary, Axtone, are necessary to keep equipment running smoothly. ITT has entered a sector with consistent demand by providing these specialist items since defense organizations are always looking for cutting-edge tools to guarantee the security and efficiency of their employees.

ITT is able to serve the essential military requirements of nations while better managing the risks associated with economic volatility in other businesses because of its diversification into the defense industry. Additionally, it strengthens ITT’s overall financial performance by offering a varied income stream and improving the business’s capacity to utilize its creative ideas and engineering know-how in a range of applications. As a consequence, ITT keeps improving its market share and profitability while skillfully controlling the risks related to industry-specific difficulties in the military sector.

Risks

Technological Change: Quick advances in technology have the potential to make current goods and services outdated. To remain abreast of technical advancements in its many businesses, ITT has to make ongoing investments in research and development.

Supply Chain Disruptions: Natural catastrophes, geopolitical crises, or other causes may cause supply chain disruptions that affect ITT’s capacity to produce and distribute goods. Setbacks in the supply chain might lead to higher expenses and longer wait times.

Conclusion

To summarize, I believe that ITT is currently a solid company that is just overvalued given current financials. With a strong balance sheet, solid growth strategy, great earnings, and solid FCF deployment, reevaluating the stock if selling pressures bring the price down to my fair value or changes occur in the core business would be the best course of action.

Read the full article here