Gen Digital (NASDAQ:GEN) sells cyber security products in multiple continents. The company was formed as a result of a merger between Avast and NortonLifeLock, that should result in a good amount of cost synergies. The company has a massive amount of debt, I believe that Gen’s operations’ very stable nature makes the debt reasonable. The stock currently trades at an estimated forward P/E of 8.7, which seems very low compared to the company’s further merger prospects.

The Company & Stock

Gen Digital operates a number of antivirus products as well as other cyber security solutions. The company’s software offering includes well-known brands such as Norton, Avast, Avira, AVG, and CCleaner. For investors, I believe that the business model is very good – constant subscription-based revenues make Gen’s cash flows very stable.

Gen’s performance on the stock market has been quite good. In the past ten years, the stock has appreciated at a CAGR of 4.8%. The appreciation CAGR doesn’t represent the entirety of the stock’s return, though – Gen has had two special dividends in the period with a $4 dividend in 2016 and a $12 dividend in 2020. The company has also started to pay out a regular quarterly dividend recently, with a quarterly amount of $0.125 making the stock’s forward yield 2.84%.

Ten-Year Stock Chart (Seeking Alpha)

Merger Between Avast and Norton

Gen Digital was formed as a merger between Avast and NortonLifeLock. The companies finally merged in September of 2022 with intentions of $280 million in cost synergies. So far, the synergies have proven to proceed well for the merged company – Gen approximates to have achieved around $240 million in synergies so far with $60 million in cost synergies remaining. The company’s headcount has come down by around a thousand people from 4500 to 3500 – the merger lowered the combined company’s need for SG&A. In addition, Gen has identified a significant amount of potential revenue synergies at an estimated $200 million – the company should see increasing revenues in the coming years.

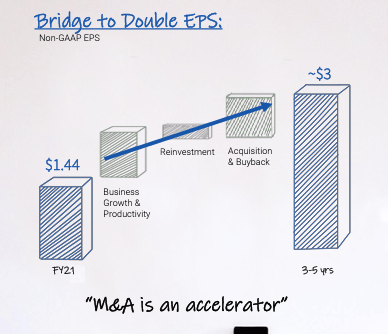

The company has plans to increase its EPS through capital allocation in addition to the targeted cost and growth synergies. In total, Gen is targeting an EPS of $3 from FY2025 forward as a result of the synergies, reinvestments and acquisitions as well as stock buybacks:

Combining Avast and NortonLifeLock Presentation (August 2021)

Financials

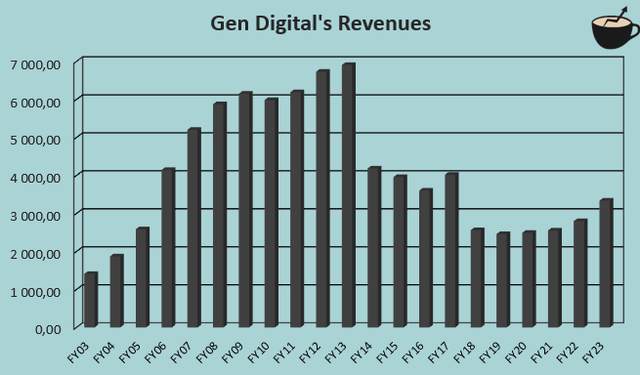

As a result of constant acquisitions and a few divestments, Gen’s historical revenues have fluctuated largely. In complete, the company’s compounded annual growth rate has been 4.4% from FY2003 to FY2023:

Author’s Calculation Using TIKR Data

When excluding M&A activities, Gen’s growth seems to be very stable. In Q1/FY2024, Gen had a pro-forma growth of 2% in the cyber safety segment. Gen also has further stability as the company’s EBIT margin is very wide – with trailing figures as of Q1/FY2024, Gen’s margin stands at 41.6% with further leverage likely to come from synergies and growth opportunities.

As a way to leverage the extremely stable operating figures, Gen leverages a very large amount of debt in the company’s operations. Currently, Gen has long-term debt totalling $9.6 billion, of which $0.2 billion is in the current portions, to be paid off within a year. Compared to Gen’s market capitalization of $11.3 billion, the debt seems quite excessive. Still, I believe that the debt is mostly a strategically well-placed way to finance the operations in a cheaper fashion – as interest expenses cover 36% of Gen’s operating income, the leveraging still seems to be on a safe level, although it does seem excessive at first glance.

Upcoming Q2 Results

Gen is reporting its Q2 results in the premarket on the 7th of November. Analysts are expecting revenues of $947.5 million compared to Gen’s guidance of $940 million to $950 million. The company’s revenue guidance range for Q2 is very shallow; I don’t believe that the stock should see very much volatility unless the guidance is either surpassed or undercut significantly. For the EPS, Gen has guided for a figure of $0.46 to $0.48. Analysts are expecting a figure of $0.47 – analysts are in line with the management’s views. I don’t see a reason to doubt the management’s views for Q2 results; I am more interested about the advancement of growth synergies that the merger has made possible.

Valuation

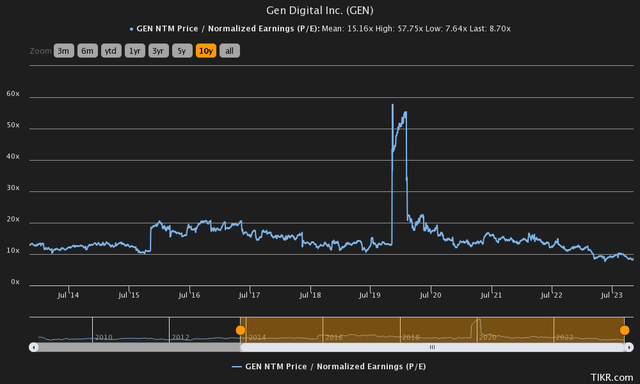

Gen seems to trade quite cheaply. The stock currently has a forward P/E of 8.7, significantly below the ten-year average of 15.2:

Historical Forward P/E (TIKR)

Although the P/E ratio alone seems cheap, I believe a further context into the valuation is justified. In my usual manner, I constructed a discounted cash flow model to further analyse the valuation and to estimate a fair value for the stock with estimates that I see as reasonable.

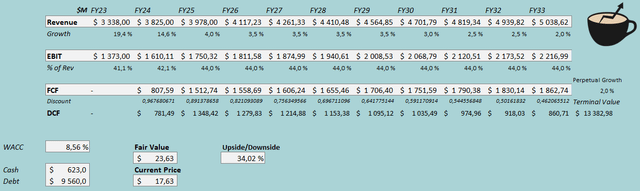

In the model, I estimate Gen’s organic growth to stay at low single-digit figures on a pro-forma basis. In the current fiscal year, I estimate a growth of 14.6%, representing the company’s revenue guidance middle point with a figure of $3825 million as the merger still adds to Gen’s growth. After the year, I estimate the growth to be 4% with organic efforts due to the potential revenue synergies. The growth slows down in steps into a perpetual growth rate of 2%. In total, the estimated revenues correspond to a CAGR of 3.1% from FY2024 to FY2033.

For the company’s margin, I estimate some leverage in FY2024 into an EBIT margin of 42.1%, one percentage point above the achieved FY2023 level. After the year, I still estimate some further leverage due to the estimated revenue growth and some marginal cost synergies – in FY2025 and beyond, I estimate an EBIT margin of 44.0%. Gen has a large amount of amortization on the company’s accounting earnings due to previous acquisitions – the company seems to have a very good cash flow conversion as a result. In total, the mentioned estimates along with a cost of capital of 8.56% craft the following DCF model with a fair value estimate of $23.63, around 34% above the current price:

DCF Model (Author’s Calculation)

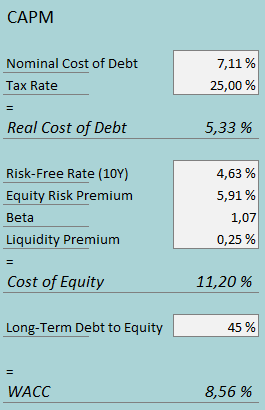

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

In Q2, Gen had $170 million in interest expenses. With the company’s current amount of interest-bearing debt, Gen’s interest rate comes up to a figure of 7.11%. As Gen seems to leverage debt very significantly, I estimate the company to have a large long-term debt-to-equity ratio at a figure of 45%. I believe that the high amount of debt can be kept up, as Gen’s overall cash flows from operations seem stable.

On the cost of equity side, I use the United States’ 10-year bond yield of 4.63% as the risk-free rate. The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the United States, made in July. Yahoo Finance estimates Gen’s beta at a figure of 1.07, used in the CAPM. Finally, I add a small liquidity premium of 0.25%, crafting a cost of equity of 11.20% and a WACC of 8.56%.

Takeaway

Gen seems to be underpriced when considering the company’s further synergies from the merger. The DCF model estimates Gen’s stock to be quite significantly below the fair value with estimates that I see as very reasonable. Although the company’s debt could potentially pose a threat, I don’t see Gen’s stable cash flows as likely to be disturbed too significantly for the debt to fundamentally change the investment case. For the time being, I have a buy rating for the stock.

Read the full article here