Alpine Income Property Trust, Inc. (NYSE:PINE) is a small cap REIT that owns and operates a portfolio of single-tenant net leased retail properties. The company model is similar to the earlier version of Realty Income (O). Realty Income has a market cap of $34.0 billion, while PINE has a market cap of $238.5 million, placing it at the lower end of the small cap range in size. Alpine says its goal is to “seek attractive risk-adjusted returns and generate dependable cash dividends by….operating a portfolio of single tenant net leased commercial income properties.” As of October 2023 it had 138 net leased properties located in 35 states. Alpine is a young REIT and its IPO launched in November 2019, offering 7.5 million shares at an opening price of $19.00. Since then the stock has been range bound trading between $13.00 and $20.61; the current price is $15.70, see the chart below. Recently, shares took a precipitous dive after the October 19h Third Quarter earnings call, dropping from $16.55 to $14.43, a change of 12.8%. I last covered this REIT in September.

PINE Share Price History (Seeking Alpha Charting)

Why Shares Dropped After Q3 Earnings

Two events caused the selloff: the bankruptcy of one of PINE’s tenants and a cut in the earnings estimates for the year. One of the smaller tenants, Mountain Express, had been in Chapter 11 bankruptcy and instead elected to liquidate through Chapter 7. Alpine had leases with Mountain Express for seven gas stations branded as Valero. These are now vacant and are located in Mississippi and Ohio. They total 13,256 Square feet and had generated about $640,000 in annual revenues. According to the third quarter earnings report, these properties will now be sold off. In the interim, PINE will be responsible for carrying property taxes and insurance. In terms of its overall portfolio, the Valero stations represented 0.3% of the square footage and about 1.6% of the annualized base rent. The company took a one time impairment charge of $2.86 million in the third quarter, or about $0.21 per share. This was partially offset during in Q3 by a gain on the sale of several retail properties in the amount of $2.59 million. Management now expects to have all the Valero properties sold and the issue resolved by the end of the fourth quarter.

The second issue for investors was the downward revision of earnings in 2023, related to the Mountain Express bankruptcy and other factors. Per the company’s Senior Vice President, the revision was also about the “the timing of asset sales and investments…and slightly higher interest expense.” The company revised the FFO estimate for 2023 to $1.45-$1.47 per share, down from $1.50-$1.53 per share. AFFO was revised from $1.52-$1.53 per share down to $1.46-$1.48 per share, a drop of about $0.06. These revisions are a downward change of 3.0-4.0%, meaningful, but not significant. Many companies have revised estimates downward of late due to rising interest expense, particularly in the utility and REIT sectors.

The Current Property Portfolio

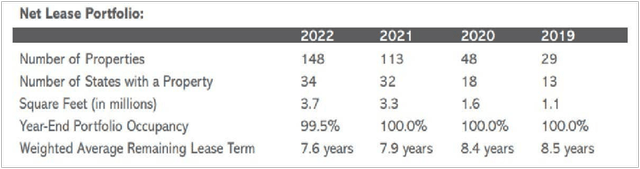

Alpine currently owns properties in 35 states, the majority of which are east of the Mississippi in New Jersey, New York and Ohio. There are also some in Texas. Many of these are freestanding big box retail stores and stores in power centers that are on their own parcel. As of year-end 2022, the company had 3.6 million square feet of retail space. As of the Third Quarter 2023, this number increased 8.3% to 3.9 million SF. The space is leased at an average rate of $11.06 per SF, per the 2022 Annual Report.

PINE Portfolio Change by Year (2022 Annual Report)

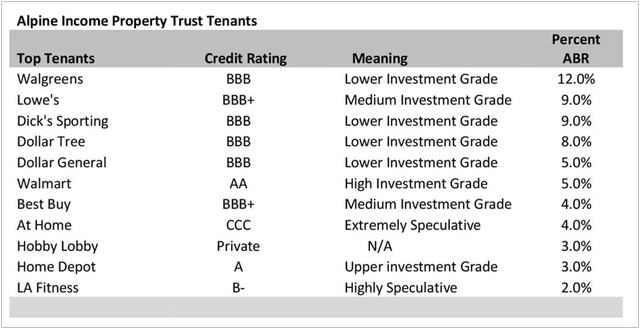

I have located the top 10 tenants in the company’s 3.9 million square foot third quarter portfolio, based on square footage leased and ABR. Lowe’s (LOW), Walmart (WMT), DICK’S Sporting Goods (DKS), Dollar Tree (DLTR) and Dollar General (DG) are the standouts. The top tenants are presented below with their current S&P credit rating.

Top Tenants and Credit Ratings (2023 Investor Presentation)

In addition to the largest tenants above, the company’s portfolio also consists of leases in much smaller percentages to Advance Auto Parts, Big Lots, Burlington, Buffalo Wild Wings, O’Reilly and Harbor Freight. There is a unique lease for the Alpine Valley Music Theatre, in East Troy, Wisconsin. This is an entertainment venue consisting of a two-sided, open-air, 7,500-seat pavilion, an outdoor amphitheater with a capacity for 37,000, and over 150 acres of green space. The tenant is Live Nation Entertainment and the lease generates $634,000 per year in rent. There is also a Long John Silver fast food restaurant that is ground leased. Other than these two properties, the leases are straightforward net, either fixed or with rental escalations.

Of course the most worrying tenant of this group is At Home, a Dallas based furniture store, which currently occupies 179,362 square feet. As the REIT acquires more properties, this At Home has dropped from 4.91% of Alpine’s Portfolio in the second quarter, to 4.6% in the third quarter. In May of 2023, Standard & Poor’s downgraded At Home, regarding a new $200 million private placement, stating as follows: ““We view the transaction as distressed and tantamount to default because consenting unsecured note holders will receive less than the original par amount promised. We lowered our issuer credit rating on the company to ‘SD’ (selective default) from ‘CCC+’ (substantial risk).” This company currently pays Alpine $1.44 million in rent per year. This is about 3.7% of the total annual rental income of $39.2 million.

Another company of concern is Academy Sports (ASO) a sporting-goods store headquartered in Houston with 268 locations, primarily in the south and southeast. It is rated non-investment grade speculative and leases 5.07% of Alpine’s total space. However, ASO earnings per share increased 5.2% in 2022 to $7.49 and a new CEO is in place, the company’s former head of merchandising. Guidance for 2023 is slightly lower, at $6.65 to $7.35 per share, but stable. There’s also some slight overlap here with DICK’S Sporting Goods (DKS), which has a higher credit rating of BBB, or lower investment grade. Like Target (TGT) before it, Dick’s said last week that retail theft is damaging its business and would lead to lower annual profits. This caused a 23.0% drop in second quarter profits, and more problems in the third quarter. Dollar General also says shrinkage is a concern. However, DKS is the largest US Sporting Goods retailer and has been around a long time, since 1948. I believe it’s likely to survive current shrinkage trends and consumer wallet-tightening.

If we make the hypothetical assumption that At Home goes away, it would remove $1.44 million in income. Funds from operations at the end of 2022 were $23.72 million and dividends were $15.12 million, leaving a difference of $8.6 million, easily covering any shortfall due to At Home. As a business, though, At Home has proved resilient in the past: it survived a 2004 bankruptcy filing, and was revived with a new name and new investors, see story. In 2023, FFO is estimated to be about $1.47 per share or $20.14 million total, and dividends are estimated at $15.07 million, so still easily covered without At Home’s revenues. If we also remove the $640,000 rent generated by Mountain Express, I estimate the payout ratio would still only be 77.3%.

Notes on Lease Structure and Expirations

According to the company’s annual report, 38% of the leases in its portfolio have annual increases in the long term rent. Nearly all of the leases are triple net, in which the tenant pays for all costs associated with the property including taxes, insurance, and common area maintenance [CAM] if any. Structural reserve in this type of lease may be paid by either the landlord or the tenant. Occupancy across the portfolio was 99.5% as of mid-year 2023; however the departure of Mountain Express dropped this number to 99.0%, still very strong.

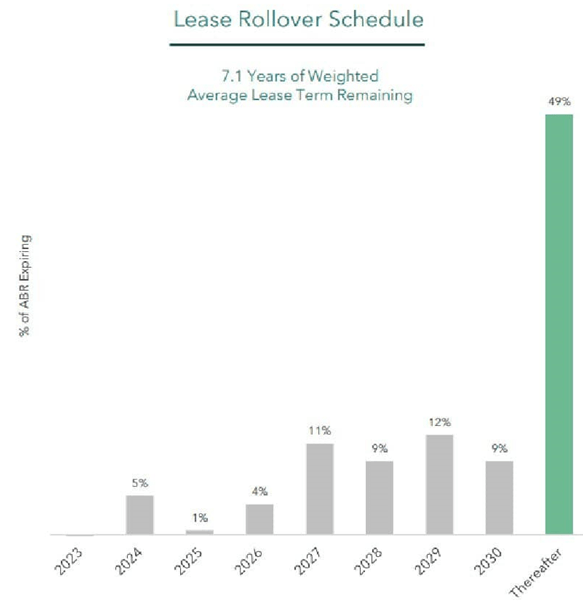

The weighted remaining lease term duration is 7.1 years as of the third quarter 2023, see chart below. Ideally this period would be longer. At lease expiration, tenants can renew their lease or depart, so there is an element of risk here. However, Net Lease Advisor has research on the term of leases for various retail tenants nationally. For example, the typical Family Dollar net lease is 15 years with successive option periods of five (5) years each. Hobby Lobby leases typically have a base term of 15 years, with three, 5-year renewal options. Walgreens apparently used to require eight to ten renewal options of five years each, but recently they ask for 75-year leases with cancellation options every year after year 25. In my real estate experience I have found that most triple net retail tenants have multiple renewal options, often five years in length, and usually at a pre-negotiated rate. This rate is higher than the base lease, but may be favorable compared to the current market. The probability of a tenant staying in place is usually higher than 50%, due to relocation costs and other factors. This means that while some leases will start expiring after 2030, many of Alpine’s tenants are likely to have five-year renewal options, or more, so I look at this risk as not being excessive.

Current lease Rollover Schedule (2023 Investor Presentation)

Updated Share Valuation

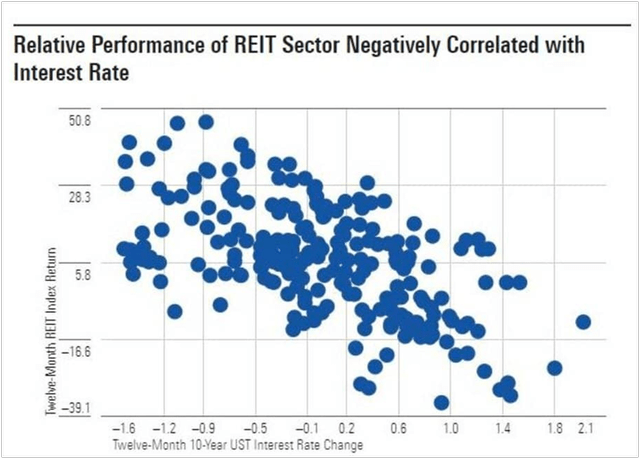

REIT valuations are down this year, and according to Morningstar, “The sector was down 7.2% in the third quarter, while the broader market was down 2.3%.” The performance of this segment is generally inversely correlated with increasing interest rates over time, as illustrated below. And REITS likely use borrowed funds, which now have higher rates.

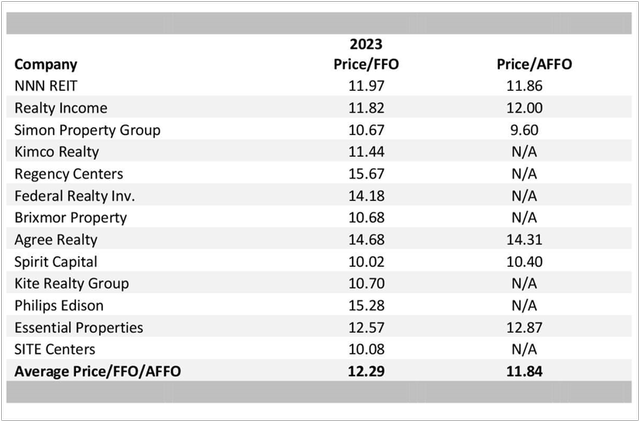

The market approach to valuation for REITs is Price/Funds From Operations (FFO), or Adjusted Funds From Operations (AFFO) if that number is available. FFO is essentially the REIT cash flow and Alpine publishes this metric and AFFO in its annual report. In the third quarter 2023, the company’s FFO outlook was revised downward to $1.45-$1.47. AFFO was revised to $1.46 to $1.48, nearly identical. Below is a list of price to FFO multiples for 13 different publicly listed retail REITs of various market caps. The average for this group was 12.29, lower than this multiple would have been six months ago. For the few that published AFFO, the average was 11.84.

Interest Rate and REITs are Inverse (Morningstar) FFO and AFFO Multiples (Author Sourced)

Using the FFO and AFFO third quarter consensus of $1.47, the valuation of PINE calculated using both multiple averages would be: 12.29 X $1.47 = $18.07, and 11.84 X $1.47 = $17.40. At the current share price of $15.70, PINE is between 10.0% and 13.0% undervalued, or 10-15.0%, rounding.

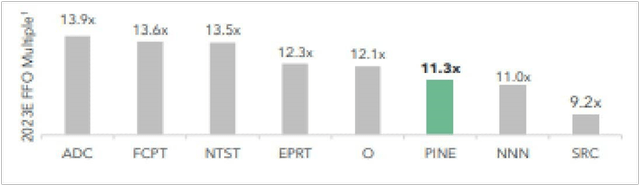

Looking at the value the other way, at Alpine’s current share price is $15.70 and estimated earnings of $1.47, the current multiple is 10.68, exceptionally low compared to other REITS. Below is a relatively recent chart of retail REITs that are similar in strategy to Alpine, and considered its peers, including Agree Realty (ADC) and Four Corners Trust (FCPT). The average multiple for this group is 12.2.

FFO Multiples of Peers (2023 Investor Presentation)

Dividend Still Looks Safe

At the current share price of $15.70, the dividend yield is 7.0%. This is significantly higher than most of Alpine’s peer group, which have yields of 5.0-6.0%. Historically, Alpine’s first dividend payment was December 2019 in the amount of $0.06. Alpine’s dividend was $0.658 in 2019, $0.82 in 2020, $1.015 in 2021, and $1.09 in 2022 and $1.10 in 2023. I calculate an annual compound growth rate of 13.7%.

PINE Dividend vs. Peers (2023 Investor Presentation)

There have been three dividends paid in 2023, at $0.275 per quarter and there should be an increase in the next, or the fourth, quarter. The dividend payout ratio has varied from 63.0% to 66.7% of FFO and for 2023 the company is estimating a higher payout of 74.0%, still well within industry norms and easily covered. FFO at the end of the third quarter was $0.37 per share and the dividend was $0.275 per share. The payout ratio for the quarter when Mountain Express vacated its stores was 74.3%.

The current yield of 7.0% is superior to that of many other retail REITs trading on the market right now. Realty Income (O) is currently paying 6.58%, Four Corners Property Trust (FCPT) is paying 6.38%, Agree Realty (ADC) is paying 5.18% and Essential Properties (EPT) is paying 5.1%.

Risks to Outlook

The primary risk to my value estimate is if the Fed raises rates once or twice further, lowering valuations in the REIT sector again. We know REITs move in the opposite direction to interest rates. The other risk is that another tenant succumbs to a slowing economy; it could be one of several possibilities like At Home. My previous concern with this company was the percentage of non-investment grade tenants at the end of 2022, about 10% of the total square footage. However, Alpine began addressing this in 2023 by divesting of most of its Academy Sports spaces and rotating into Starbucks and Marshalls and adding more space leased to Lowe’s. These are all investment grade tenants.

Conclusion

Management may have been caught a little off guard by the Mountain Express Chapter 7. The company was previously looking at reorganization and there was deadlock in negotiations with the largest unsecured creditor. Thus the company liquidated. But the seven Valero stations that closed represent only 0.3% of the square footage and about 1.6% of the annualized base rent in PINE’s portfolio. The third quarter report in which the consensus earnings for the year were lowered did not help either. But this was an adjustment of 3.0-4.0%, not surprising in a rising interest rate environment. Today, I believe Alpine is well managed and has been steering its retail mix toward more investment grade companies like Lowe’s, Marshalls, Starbucks and Chik-Fil-A. As management says, once the fourth quarter 2023 is over, the properties that were vacated by Valero will have been sold. The $2.86 million charge off related to Mountain Express is already a thing of the past. I believe the stock will be a good long-term value after the current credit issues are resolved. And the lower valuation has increased the yield to a very appealing 7.0%.

Read the full article here