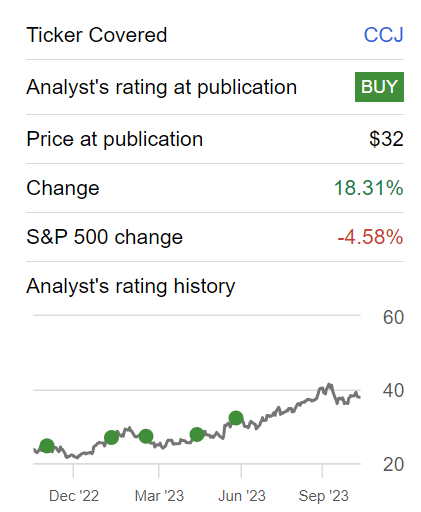

Investment Thesis

Cameco Corporation (NYSE:CCJ) just reported Q3 results of CAD$0.32 (approximately US$0.23), a big beat against the CAD$0.10 EPS analysts expected). It also declared another CAD$0.12 dividend.

As an unwavering bull of Cameco, you might expect me to be very pleased with this latest set of results.

Author’s work

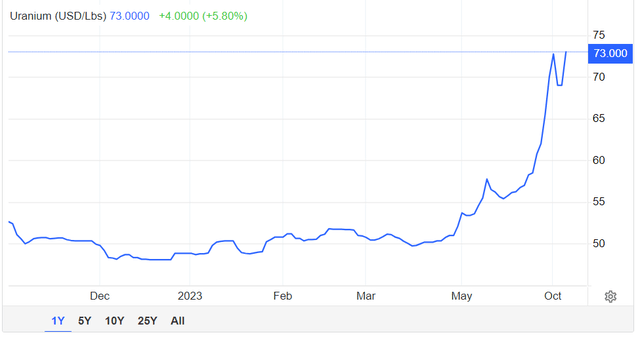

And you’d be right. What I find ironic is that the energy transition is taking hold right before our eyes, and so few investors appear cognizant of this fact. The most illustrative insight to support this contention is that we are far from the $100 WTI prices (CL1:COM) of last year, while uranium prices are now at a 12-year high. A massive contrast.

Meanwhile, as you’ll see, Cameco’s prospects remain very strong, and the stock is still very attractively priced at 17x next year’s EPS.

Why Invest in the Nuclear Sector?

Nuclear energy stands as a pivotal component in facilitating the global energy transition toward achieving the ambitious carbon emission reduction targets set for 2050.

Leveraging uranium as its fuel source, nuclear power presents a cost-effective, highly scalable, and carbon-free energy solution, offering a foundation for achieving sustainable development goals.

As countries seek (forced?) to reduce their reliance on fossil fuels, nuclear energy emerges as a dependable source of base load power, providing a consistent electricity supply without generating greenhouse gas emissions.

Its capability to operate continuously, irrespective of weather conditions, makes it an ideal complement to intermittent renewable energy sources like wind and solar. With advanced technologies ensuring improved safety standards and the potential for advanced fuel recycling, nuclear energy stands on its own as a promising, low-carbon energy source, playing a vital role in the global transition toward a more sustainable and eco-friendly energy landscape.

Trading Economics

And as you can see above, uranium prices are moving higher correspondingly.

Cameco’s Near-Term Prospects Discussed

As you know, Cameco’s production schedule hit a snag a few months back that led to its production coming down by around 9%. This wasn’t a huge reduction, but given that the stock had been on a tear, this forced the stock to take a breather.

Nevertheless, despite this reduction in production, given the strong uranium prices, Cameco was still able to raise its revenue outlook by 2%. Given everything that has already taken place in 2023, for Cameco to still have any juice left to upwards revise its revenue outlook clearly demonstrates just how favorable the uranium market environment is at present.

Cameco’s Stock Valuation — Not a Lot is Priced In, 17x Forward EPS

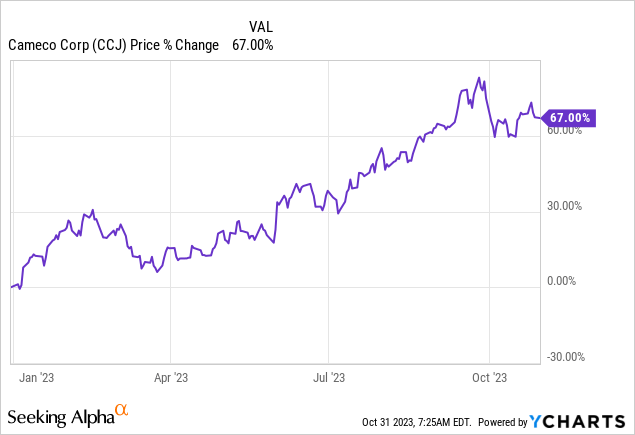

A lot of investors have made the assertion that Cameco is up 67% in 2023, therefore its prospects are already priced in. Please, allow me to make something clear. Looking back to where a share price was at the start of the year tells you nothing. Nothing about where it will be tomorrow, next month, or in 12 months.

All that matters is if the business’s intrinsic value is expected to continue to grow. And how much is already priced in? Along these lines allow me to provide some tentative perspective.

According to my estimates, Cameco is likely to deliver approximately CAD$1.00 of EPS in 2023 ($0.72). This implies that its stock is at 53x this year’s EPS.

However, we should only use this figure to provide a framework. Because the real money is made looking out to 2024.

Allow me to provide some further perspective. Cameco’s EPS went from CAD$0.03 to CAD$0.32 in twelve months. A jump of more than 1,000% y/y. That’s the power of operating leverage working in your favor. Where a 48% y/y increase in revenue can lead to such a dramatic jump in EPS.

If we extrapolate my rough estimate of CAD$1.00 of EPS this year and increase it by 200% in 2024, a feat that is meaningfully smaller than in 2023, but still very much within the realm of a likely scenario, all of a sudden in 2024 Cameco will make around CAD$3.00 ($2.17 in EPS). This puts Cameco priced at 17x forward EPS.

Now, to make something clear. I’ve not penciled in any heroics. After all, what I’ve described above about uranium’s future is the start. We are just coming out of a 12-year low winter for uranium.

This rally is only getting started. And there are still a lot of doubters around. Once everyone ”believes” in uranium’s prospects, this stock will be priced at more than 50x forward EPS. In that context, paying 17x next year’s EPS appears to be a very reasonable valuation.

Downside to Cameco?

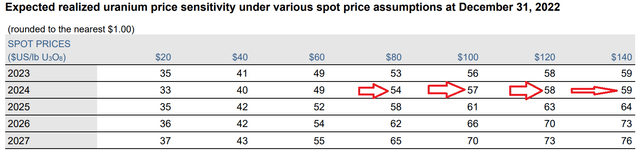

In my opinion, Cameco’s downside is that its business is hedged out.

CCJ SEC filing

As you can see above, in 2024, even if the price goes above $80 per lbs, it makes no difference in the grand scheme of things. Whereas an unhedged pure-play stock, for instance, Uranium Energy Corp. (UEC) would perform very strongly (disclosure: I’m long UEC).

Uranium Energy Corp. isn’t the only unhedged North American uranium player. But my message is this. The same as you’ve just witnessed now with this massive amount of operating leverage from Cameco, you’d get this even more from those uranium players that have very high mining cost.

The Bottom Line

In conclusion, it is evident that the uranium bull market is merely in its initial stages, with ample room for further growth and development.

Considering the current market landscape, paying 17x next year’s EPS represents an incredibly appealing entry point for Cameco Corporation investors keen on capitalizing on the burgeoning opportunities within the nuclear sector.

Rather than dwelling on past performance, investors should remain forward-looking, acknowledging the potential and enduring value that the nuclear industry, particularly uranium-related investments, is poised to offer in the foreseeable future.

With the energy transition gathering momentum, embracing the promising trajectory of uranium’s upward trend stands as a prudent move, one that’s likely to yield substantial returns and contribute significantly to a sustainable and thriving energy landscape.

Read the full article here