Wheels Up Experience (NYSE:UP) is a small-cap company that offers private on-demand aviation services in the US. It is similar to Uber in some ways but there are also many differences. The company is running out of time and money and it will have to show profits soon if it wants to stay in business, and I see this company as a very risky business that might not have much time left to turn things around.

The company’s business model includes a membership plan where it has about 12,000 members. The company also has a strategic partnership with Delta Air Lines (DAL) where the company’s members can enjoy special discounts from Delta flights and Delta has some equity investment in the company.

The company also has a couple side businesses that include selling used aircraft, offering safety and security solutions to third parties, consulting and training programs for individuals, government, and non-government organizations as well as corporations but these businesses make a relatively small part of the company’s total business. The company’s main business is selling on-demand flight services to its member customers.

The company has a network of 1,500 private aircraft that are vetted in terms of safety, security, and other factors which its 12,000 members can hire for flights. The company’s service area includes a pretty large portion of the US and the company doesn’t have any international exposure at the moment.

Map coverage of the company (Wheels Up)

The company’s revenues come from four buckets. First, membership fees that it collects from its 12,000 members which are recurring and predictable. Second bucket is the flight revenues which is basically what people are paying for the flights they ordered from the company’s app. This includes flights booked by both members and non-members since the company doesn’t require a membership to book flights but there are some obvious advantages to membership such as being able to get better deals. Third, the company also charges its pilots a fee in order to operate within the system and it can also charge them for a variety of services it offers such as fueling and aircraft maintenance. The fourth bucket is other services offered to third parties that I mentioned above such as consulting, training, safety solutions, and selling pre-owned aircraft.

A view of the app (Google Play)

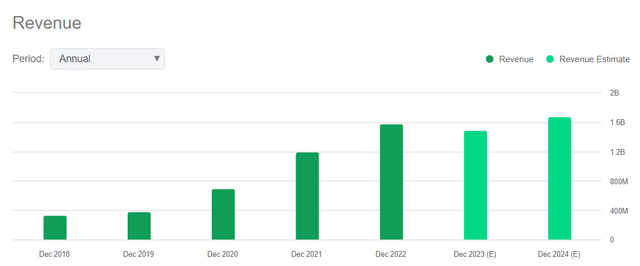

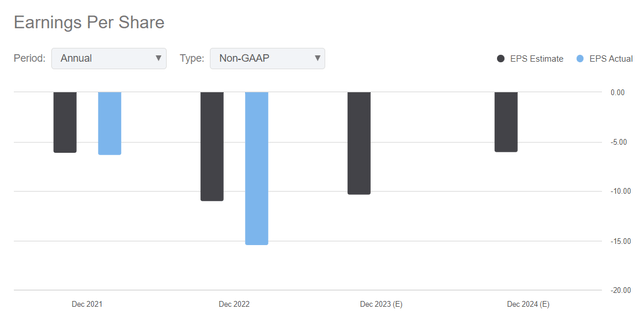

The company’s financial results so far have been very concerning. While its revenues have been growing at a healthy rate, it didn’t translate into profits or positive cash flows. Between 2018 and 2023, the company was able to grow its annual revenues from $332 million to $1.5 billion representing an average annual growth rate close to 40% but its profits and cash flow situation seemed to get worse each year instead of getting better.

UP Revenue Growth (Seeking Alpha) Up Profits (Losses) (Seeking Alpha)

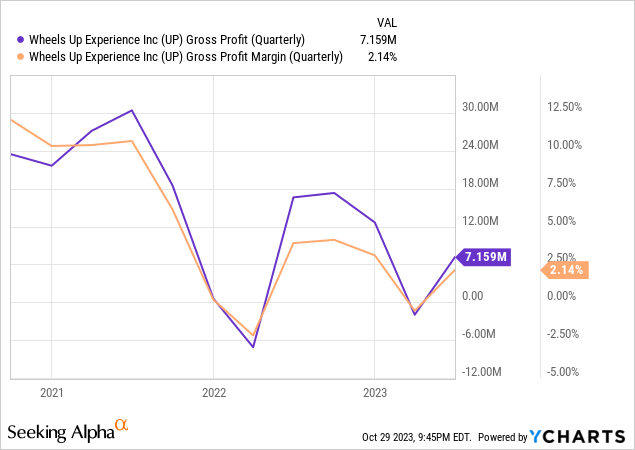

One of the biggest issues with the company is that its gross profits are close to zero. Since going IPO, the company’s gross profit margins averaged about 4-5% and it currently sits at 2%. This is before you add operating costs, debt servicing, and taxes so it is telling us that the company is mostly selling its flights at cost or only slightly above cost. There is no way the company can turn a profit if a flight costs the company $100 and it charges about $102-104 for that flight.

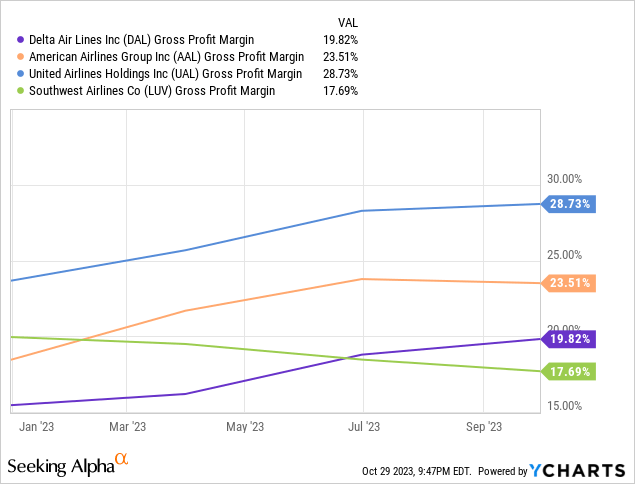

Just to serve as a reference, look at the gross margins of top 4 airlines in the US below. Their gross profit margins range from 18% to 29% and these companies aren’t awfully profitable either. One could estimate that you need a gross margin of at least 15% at bare minimum just to reach breakeven.

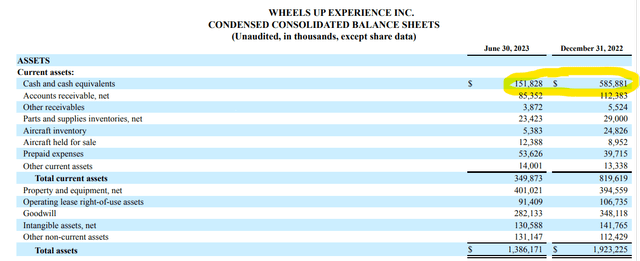

The company didn’t go through a traditional IPO process and it used a SPAC (special purpose acquisition company) as a vehicle for going public back in 2021. In this transaction, the company raised $650 million of funds but this money has already been mostly used up in the last 2 years with not much to show for. In the last 6 months, the company’s cash position dropped from $586 million to $152 million and its total assets dropped from $1.92 billion to $1.39 billion.

Current Assets (Wheels Up)

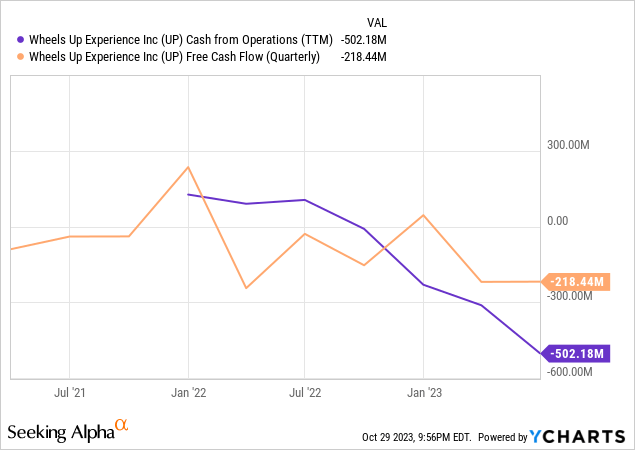

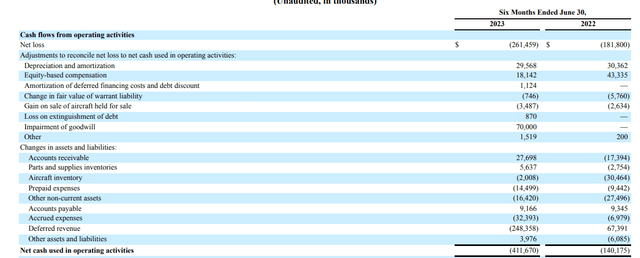

Furthermore, in the last quarter the company reported negative $502 million in its cash from operations and negative $220 million in its free cash flow.

UP Operating Cash Flow (Wheels Up)

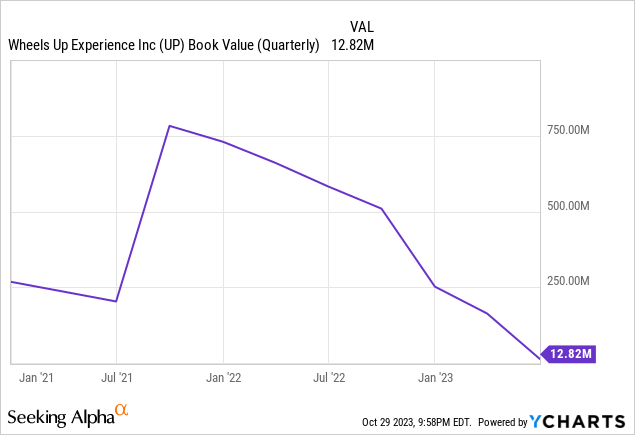

As a result of this, the company’s book value took a dive from $750 million to $12 million, which is practically zero. The company’s assets barely cover its debt.

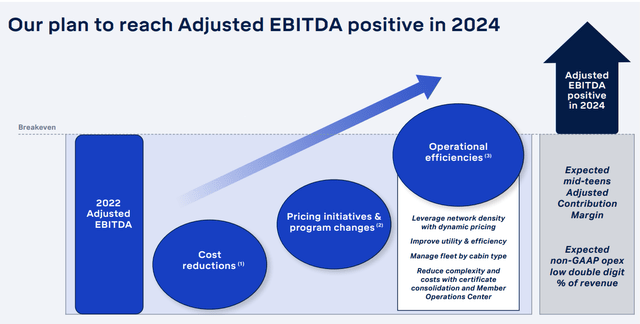

The company claims that it will reach profitability (at least on an EBITDA basis) by 2024 through cost reductions, pricing initiatives, and operational efficiencies but it’s not providing much details and specifics on these plans. For example, we don’t know what kind of cost reductions or operational efficiency improvements the company can make that can take its gross margins from 2% to 20% which is needed to reach breakeven.

Company’s 2024 Plan (Wheels Up)

One thing the company says is that it will use dynamic pricing which means it will be able to raise prices in locations and at dates where there is high demand and reduce prices or even cancel offerings in places where demand is low so that the average flight can become more profitable. If the company is unable to grow its gross margins, no amount of growth will be able to save it and it’s running out of cash (and time) very fast.

In September, the company announced that it is getting a lifeline from a group of investors including Delta Air Lines, Certares Management, Knighthead Capital, and Cox Enterprises which will make available up to $500 million in credit line which will include a $350 million of term loan, $100 million of revolving credit and an additional permit to provide additional $50 million of credit if needed. These measures will give the company at least some breathing room but this is just a band-aid solution until a more permanent solution can be developed to fix the company’s structural problems. Also, keep in mind that the company will have to issue more equity to be given to those 4 companies and they will own about 80% of the company’s new equity structure which basically means a huge dilution.

In connection with the closing of the credit facility, the lenders will initially receive newly issued Wheels Up common stock representing 80% of the company’s outstanding equity as of the closing of the credit facility, on a fully diluted basis. After approval by Wheels Up’s stockholders of an amendment to its certificate of incorporation, the company will issue to the lenders additional new shares such that the lenders will own 95% of the company’s outstanding equity as of the closing of the credit facility, on a fully diluted basis.

How does that work? Let’s say a company had 100 shares outstanding in the market. Now new investors come in and the company issues new shares to them to the extent that they will now own at least 80% of the existing company. What this means is that the company has to issue 400 new shares to make that happen (400 out of 500 is 80%). For investors, this translates into a dilution of 1 to 5, in other words, 500%.

The deal hasn’t closed yet so the stocks’ data hasn’t been updated yet. Once the deal closes, it will be reflected in multiple places. First, the company’s share count will rise significantly, second, its market cap will rise significantly, third its balance sheet, cash position, total debt amount, and book value will look different.

Regardless of dilution, this company already burned through so much cash and now it’s been given a second lifeline and perhaps a final chance to make things happen and return to sustainable profitability. If it can achieve this, things could be good but if it can’t, the company might not exist anymore in its current shape and form. One could argue that if those 4 companies including Delta are willing to give so much money to the company, they must have faith in its management and its business model, otherwise they wouldn’t be throwing good money after bad money. One could also argue that if these companies invested that much into this company they might be willing to invest even more in the future to keep it afloat and keep their investment alive. Those are valid arguments too but the company has to show something quickly and it can’t keep burning through cash at the rate it’s been doing lately.

I would either stay away from this stock or keep it at a very small speculative position because we don’t even know if the company will be able to survive in its current shape and form at the moment. It is very likely that it will need additional funding just to keep its doors open. Below is a direct quote from the company’s latest quarterly SEC report:

Until the Company can generate significant cash from operations, its ability to continue as a going concern is dependent upon management taking several actions to improve its financial position including raising capital, as well as selling a mix of non-core and core assets, strategically optimizing our asset base as we execute our member program changes…Absent the ability of the Company to obtain additional funding, the Company has concluded that there is substantial doubt about its ability to continue as a going concern for any meaningful period of time after the date of this filing.

Investors should keep this in mind if they’d like to keep investing in this stock.

Read the full article here