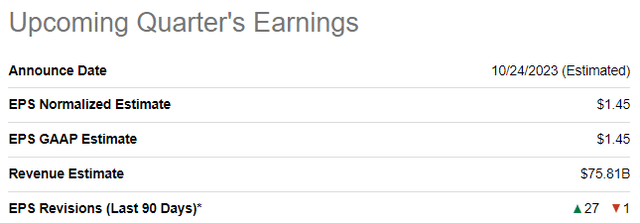

Heading into its Q3 2023 report, Alphabet (NASDAQ:GOOG)(NASDAQ:GOOGL) was projected to deliver revenues and normalized EPS of $75.8B and $1.45, respectively.

SeekingAlpha

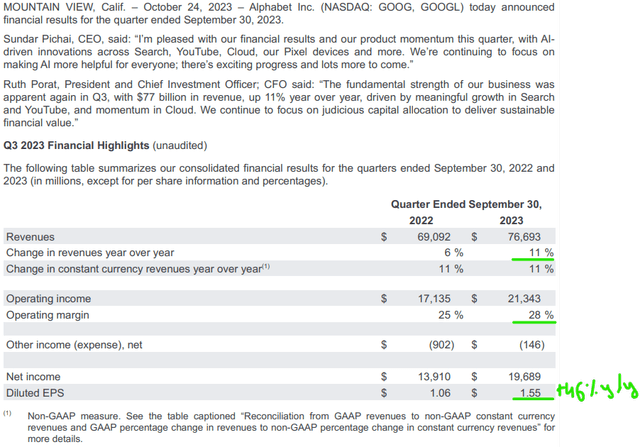

While Alphabet beat estimates on both top and bottom lines [revenue: $76.9B (up 11% y/y), normalized EPS: $1.55 (up 46% y/y)], the stock is down nearly -6% to $130 per share at the of writing. Given the stock was running ahead of our fair value estimates going into earnings, I’m not entirely surprised by Mr. Market’s negative reaction to this report, but I do see a couple of negatives in the report that might be driving the sell-off. Let’s jump straight into the Q3 2023 numbers.

Alphabet Q3 2023 Earnings Report

Despite facing challenging macroeconomic conditions and increased competition, Alphabet’s Search business remained incredibly resilient in Q3, with search business growth re-accelerating to +11% year-over-year. Clearly, Microsoft’s new AI-powered Bing is not making any inroads into Search advertising, a market where Google has monopolistic dominance.

Alphabet Q3 2023 Earnings Report

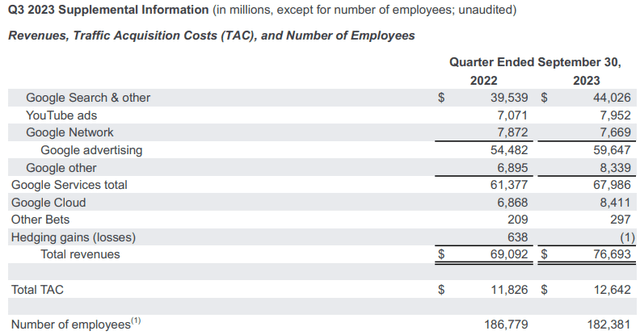

In Q3, YouTube revenues rose 12.45% y/y, marking further (somewhat expected) re-acceleration at a time when the writer and actor strikes in Hollywood are pushing consumers toward other entertainment platforms.

As I see it, Alphabet’s Ads businesses are firing on all cylinders as the digital advertising market rebounds from the abyss of the last several quarters. However, I’m also seeing a real weak spot in Alphabet’s report, with the Google Cloud business decelerating to +22% y/y growth (down from +28% y/y in Q2 2023). This deceleration is particularly alarming due to strong results at Microsoft Azure, and in my view, Alphabet’s Cloud performance is the major factor behind Mr. Market taking a glass-half-empty view of these otherwise solid set of financial numbers.

Overall, Alphabet’s revenue grew by +11% y/y in Q3 2023, with strength in Search and YouTube driving extending the ongoing re-acceleration. And as we have discussed in the past, AI opportunities can unlock the next leg of growth at Alphabet.

Let us now look into Alphabet’s profitability.

Growing hopes of a soft landing have been driving a recovery in ad spending. And this positive inflection in the business environment coupled with management’s cost-cutting measures drove Alphabet’s Q3 2023 operating income up to $21.34B (up +24.57% y/y vs. +12.3% y/y in Q2 2023) and operating margin up to 28% (vs. 25% in Q3 2022).

Alphabet Q3 2023 Earnings Report

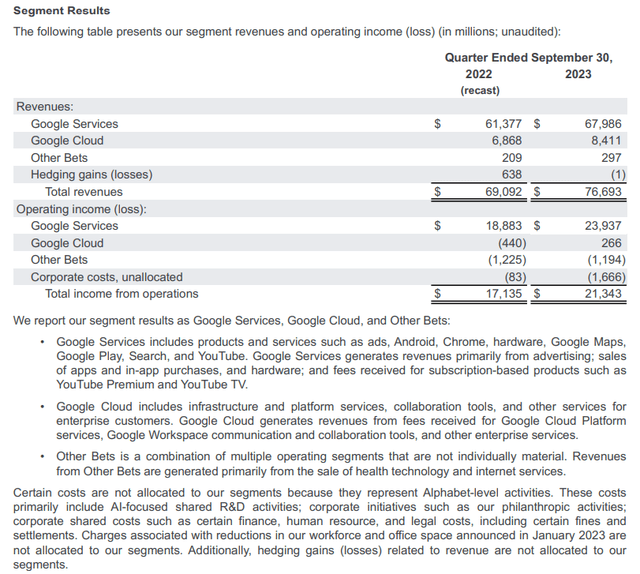

Despite experiencing a sharp revenue growth deceleration in Q3, Google Cloud managed to record another quarter with positive operating income, which is a big positive, in my view. As we know, Alphabet’s leadership team is still re-engineering the cost base, and given high Search margins there’s clearly more upside room on the operating margin (profitability) front.

However, management warned about increased capex spend (elevated level of investment in technical infrastructure) in Q4 2023 and 2024 during the Q3 earnings call, and so, I think the margin trends could worsen here for a while (before improving again in 2025 or 2026).

That said, in my past reports on Alphabet, I have labeled the digital advertising giant as a free cash flow machine and an infinite buyback pump due to its robust cash generation and humongous capital. And I see no reason to change my opinion here. During Q3, Alphabet generated $22.6B in free cash flow and returned $15.8B to shareholders via stock buybacks.

Alphabet Q3 2023 Earnings Report

As of the end of Q3, Alphabet’s net cash balance stood at nearly $106B giving the company a fortress-like balance sheet, which in my opinion, is the strongest among all big tech companies due to very little long-term debt.

Alphabet Q3 2023 Earnings Report

Considering Alphabet’s monopolistic dominance in the digital advertising market, promising growth opportunities in AI, robust free cash flow, and strong balance sheet, I believe that Alphabet’s management has all the tools to drive solid shareholder returns over the next five years by employing financial engineering techniques such as stock buybacks.

To illustrate this, we can use our Valuation Model.

Alphabet’s Fair Value And Expected Return

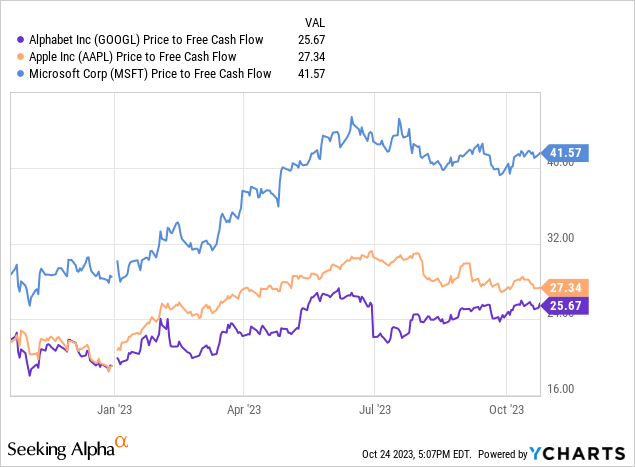

In the past, I have highlighted Alphabet’s lopsided exposure to a cyclical advertising market as a good reason for its stock to trade at a discount to some of its big tech peers. However, Alphabet’s financial performance is at par with rivals such as Apple (AAPL) and Microsoft (MSFT), and so, GOOGL stock shouldn’t really be trading at a ~20-25% discount to its peers on a relative basis.

Data by YCharts

With a rally in Alphabet and a sell-off in Apple, the valuation gap between those two tech giants has narrowed significantly in recent weeks. However, Microsoft continues to trade at an astronomical valuation. Given the spectacular run-up in long-duration Treasury yields to ~5%, I think a de-rating to ~20x P/FCF for the big tech giants is a real near-term possibility.

From a relative valuation standpoint, I no longer see a valuation upside in Alphabet stock. However, let’s deduce the absolute fair value for Alphabet using TQI’s Valuation model before reaching any conclusions.

In my previous note, I wrote –

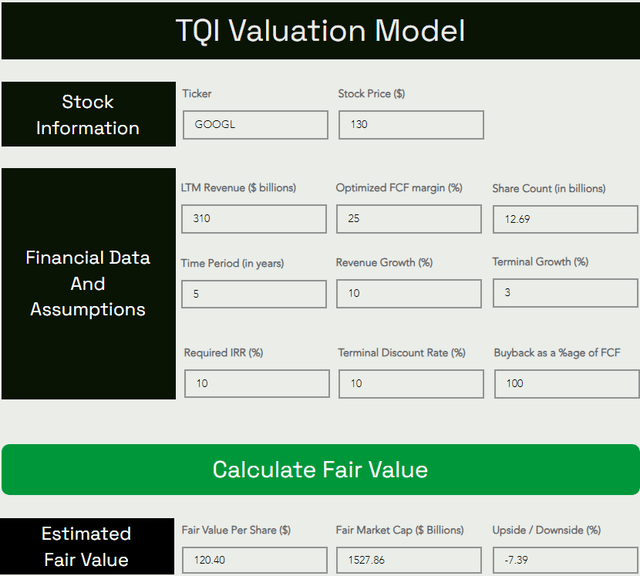

With Alphabet currently growing at low to mid-single-digit rates, a re-acceleration to double-digit growth looks implausible right now; however, I believe that AI could unlock massive new revenue opportunities for Alphabet. For my model, I have assumed a 10% CAGR revenue growth rate for the next five years. Furthermore, I have assumed an optimized FCF margin of 25%. Generally, I utilize a 15% discount rate in my DCF models; however, I think Alphabet’s business resilience and robust cash flow generation warrant a lower discount rate. For this exercise, I assumed a required IRR (discount rate) of 10%, which is what I have used only for Microsoft and Apple in the past.

Source: Google: Q2 2023 Earnings, Valuation, Technicals, And More

Given Alphabet’s business has re-accelerated back to +11% y/y in Q3 2023, I’m feeling more comfortable with my five-year growth projection. Despite solid margin improvement, I’m sticking with my conservative optimized FCF margin assumption of 25% to implement a margin of safety in our model.

Here’s my latest valuation model for Alphabet (including estimate Q4’23):

TQI Valuation Model (TQIG.org)

As you can see above, Alphabet’s fair value is ~$120.40 per share (or $1.53T market cap). With the stock currently trading around $130 per share, Alphabet stock is still overvalued by ~7%. That said, Alphabet has a positive net cash balance of ~$106B (or roughly ~$8 per share). If we were to add this net cash back to its fair value (derived by DCF), Alphabet would be more or less fairly valued right here.

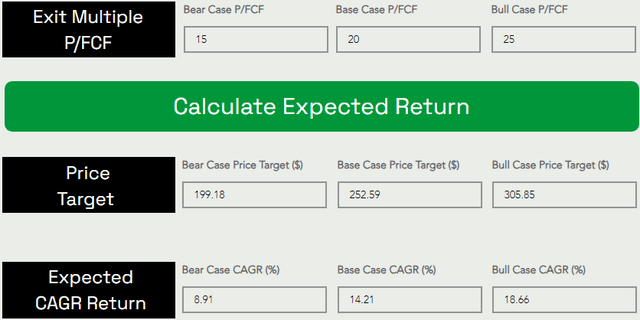

Assuming a base case P/FCF (exit) multiple of ~20x for 2027-28, Alphabet’s stock could rise from $130 to $252.6 per share at a CAGR rate of 14.21% over the next five years.

TQI Valuation Model (TQIG.org)

Since Alphabet’s expected CAGR return is still slightly lower than my investment hurdle rate of 15%, I’m not an eager buyer of Alphabet at current levels. That said, Alphabet is a decent buy for investors willing to accept somewhat lower returns (~14% per annum) in exchange for lower volatility.

Concluding Thoughts: Is Google A Buy, Sell, Or Hold After Q3 2023 Earnings?

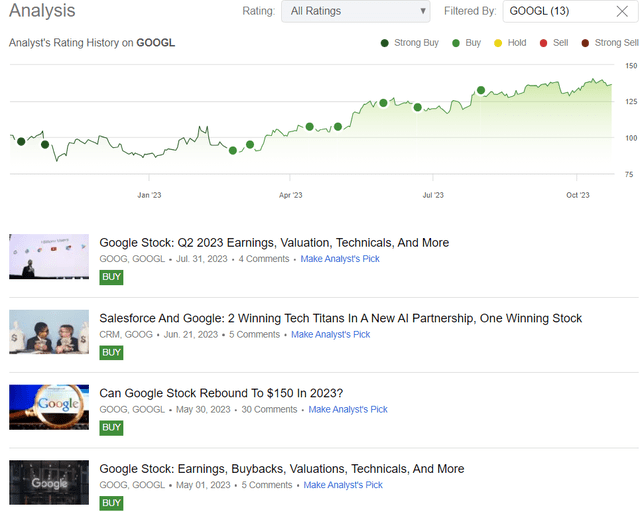

Last October, I rated Alphabet stock a “Strong Buy” in the $90s in Google: My Favorite Contrarian Bet In This Uncertain Market, and since then, I have published numerous bullish recommendations on GOOGL stock:

Author’s history on GOOGL (SeekingAlpha)

And, in my previous note, I expressed the following thoughts on GOOG stock:

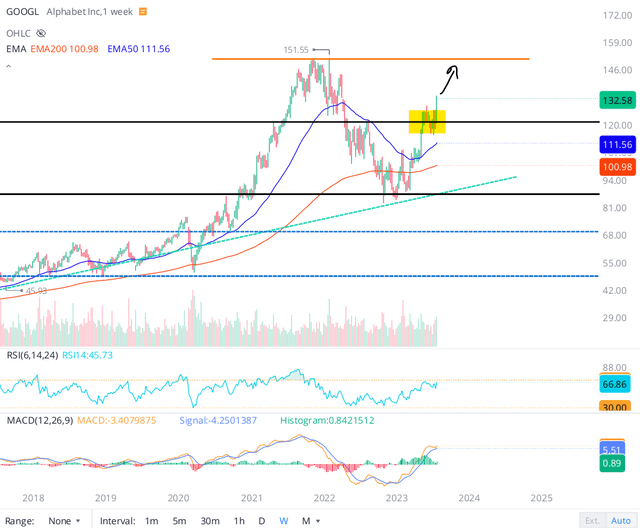

Having consolidated at the $120-$125 range before breaking out to the upside (after the announcement of Q2 earnings), Alphabet looks poised to take a run at its all-time highs of ~$150 in the coming weeks and months.

WeBull Desktop

Conversely, a breakdown below $120 could lead Alphabet to pull back down into the $90s. Technically, the risk/reward in Alphabet is quite balanced; however, momentum supports a bullish position.

Source: Google: Q2 2023 Earnings, Valuation, Technicals, And More

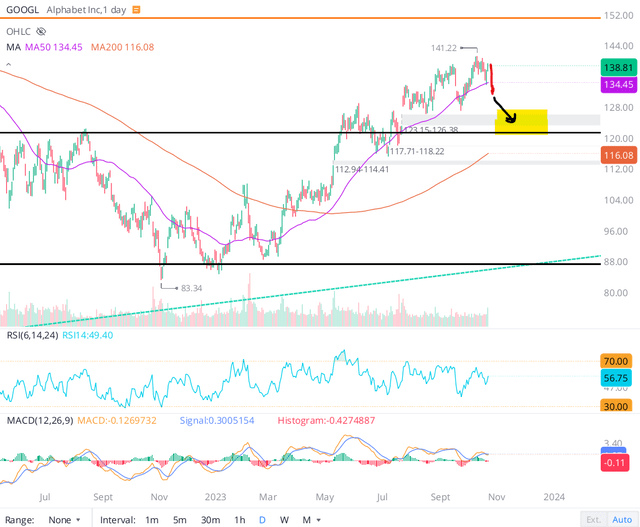

With today’s after-hours sell-off, Alphabet stock has dropped slightly below the $130 level, and technically, a re-test of the $120-125 zone is very likely now given the magnitude of the post-earnings move and the gap at $123-126.

WeBull Desktop

Heading into a potential recession, my overall outlook for “Magnificent 7” big tech stocks is bearish. However, Alphabet looks fairly valued in light of its post-Q3 sell-off. In the event of a hard landing, I would expect to get a sizable discount on GOOGL stock, but as a long-term investor, I continue to like the business and intend to hold my long position in Alphabet stock for years to come. While I won’t be buying here due to my current allocation being at target weight, I will probably start accumulating shares around the 200-DMA level at ~$115-120 if GOOGL stock were to get there.

The long-term risk/reward for Alphabet remains attractive with a five-year expected CAGR of 14%. In light of its Q3 report, I continue to see Alphabet as a reasonable “safe haven” to hide out in this uncertain macroeconomic environment, with the added bonus of participation in the secular growth mega-trend of artificial intelligence.

Key Takeaway: I continue to rate Alphabet a modest “Buy” at $130, with a strong preference for slow, staggered accumulation.

If you are pondering between Alphabet’s tickers, here’s the better buy:

GOOG Vs. GOOGL Stock: 2 Ways To Buy Alphabet, One Of Them Is Always Better

Thanks for reading, and happy investing. Please share your thoughts, concerns, and/or questions in the comments section below.