GAMCO Global Gold, Natural Resources & Income Trust (NYSE:GGN) occupies a unique moderate growth position for longer-term investors. The marketplace that GAMCO invests within, precious metals and oil, is somewhat range-bound. But, in time, that is likely to change, perhaps drastically. This article continues our bullish stance on GAMCO ownership with a deeper dive into the kind of growth. In the past, our thoughts focused on growth without considering the limiting effects from selling covered calls. In this one, our target exposes qualitatively possible limitations. In our view, the wings of growth have been partially clipped though still beautiful, while investors get paid nicely.

The Investment

Global Gold, Natural Resources Fund invests “80% of its assets in equity securities of companies principally engaged in the gold and natural resource industries. . .” The fund also uses covered call options for cash generation. In summary, the fund in its last report includes:

- Long Positions

- Metals and Mining: 50.1%

- Energy and Energy Services: 32.15

- U.S. Government Obligations: 17.8%

- Short Positions

- Call Options Written: (1.8)%

- Put Options Written: (0.2)%

A sampling of the major holdings includes:

- Exxon Mobil Corp. (XOM) 5.3%.

- Northern Star Resources Ltd. (OTCPK:NESRF, OTCPK:NSTYY) 3.8%.

- Chevron Corp. (CVX) 3.6%.

- Franco-Nevada Corp. (FNV) 3.6%.

- Newmont Corp. (NEM) 3.3%.

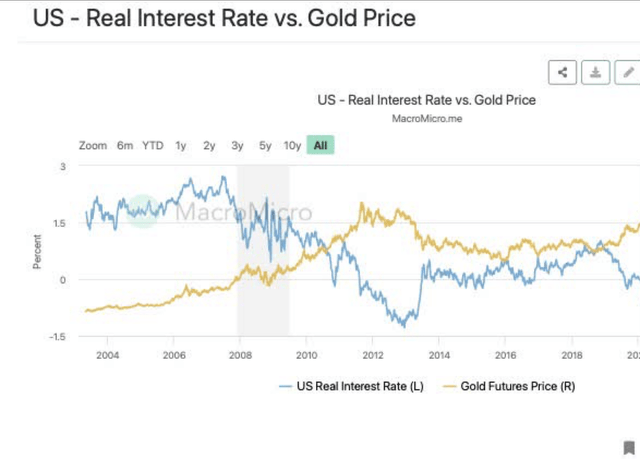

The Precious Metals

With gold pricing, an inverse relationship exists between interest rates and itself. At higher interest rates, the current status, gold trends lower, and vice versa. A graph from MacroMicro illustrates this trend.

MacroMicro

Volatility in Oil Price

With the correlation established for gold, understanding the relationship between interest and crude price is discussed next. From Investopedia,

“One of the basic theories stipulates that increasing interest rates raise consumers’ and manufacturers’ costs, which reduces the amount of time and money people spend driving. Fewer people on the road translates to less demand for oil, which can cause oil prices to drop.”

Although the two generally follow an inverse relationship, in recent weeks, an unusual positive link emerged between the dollar and crude. Tsvetana Paraskova of OilPrice wrote detailing a strange reversal. Many economists believe this is temporary. A threat of war and production cuts by key players drove the change.

Capital Growth Hinges on Interest Rates

Both investments within Gabelli’s gold and natural resource fund are in a synergy relationship with interest rates. Comments about the last Fed meeting suggest only one more quarter of a percent hike is coming.

“Along with their September rate decision, policymakers on the rate-setting Federal Open Market Committee (FOMC) signaled in new economic projections that they’re expecting to lift interest rates one more time this year.

If approved, the move would bring the Fed’s key benchmark interest rate to a new 22-year high of 5.5-5.75 percent. But it could also possibly be the last. Just one official sees the rate rising higher than that, the Fed’s new projections show.”

Also, noted above, bullish oil prices continue being driven by both outstripping demand in the long term and risks on world oil production. The fund resides in a sweet spot for future growth. For investors, it becomes a game of deciphering management actions.

Dividends & Coverage

Keeping track of dividend coverage and strategy finishes the story. Beginning, the total share count equals 154 million paying out $0.36 per year in dividends costing $55 million per year. According to the semi-annual report, expenses equal approximately $8 million per year. The total cash costs per year are approximately $63 million. On the generation side, four different sources, bonds, dividends from holdings, short options, and equity growth supply the necessary cash. A table shows a summary of the first two.

| Dividends/Interest | Interest | Value | Payment |

| Government Treasuries | 5% * | $125 million | $3.2 million |

| Company Holdings | Dividend | ||

| Varied by entity | $7.7 million | ||

| Total | $11 million |

* First half of the year.

For a year, the company earns approximately a third of its cash from the two above categories. With the increases in interest rate dynamics, investors might expect an increase to $7 million per year.

The company sells calls and by doing so creates additional returns. One investor, Richardson, asked,

“Could you specify what percent of GGN equity positions are exposed to covered calls? I would like to get a handle on how much GGN would participate when/if natural resources became strongly bullish.”

An included table offers a partial answer:

| Options * | Shares | Options | Percent of Holding |

| Company | |||

|

Barrick Gold Corp. |

1,138,519 | 11385 | 100% |

|

Chevron Corp. |

151,548 | 1515 | 100% |

|

Exxon Mobil Corp. |

345,000 | 3450 | 100% |

|

Freeport-McMoRan Inc. |

523,300 | 5200 | 100% |

* From the last six-month report.

At the end of June, management hedged at high rates of 100% of four major holdings.

Our next view considers percent return from options in the six-month time frame for near-the-money and outside-of-the-money opportunities.

* Approximately 10% above the price.

** Approximately 25% above the price.

The value provided to investors from the above table illustrates the ability of the fund to increase Total Net Assets (NAV) or growth. In essence, the fund generates approximately $22 million from interest and dividends leaving the balance of approximately $40 million from other sources, i.e., short options or capital growth. With a value for common shares equaling near $650 million, options by themselves must average a yearly return of 6%, an achievable result with options 15% or more out of the money leaving a space for modest growth.

Continuing, with a fund using major positions in short options to pay the investors, a gotcha exists with price volatility. With the price of the entities falling the net asset value falls with it, lowering the stock value. Options can be sold on the way lower with this caveat, a risk on the reversal in losing shares at low prices forcing a repurchase of fewer shares at higher prices. To monitor management’s ability to handle this, a review of the long-term NAV is included. In the two periods of inflation and higher interest, net assets grew or remained stable while paying out $0.36 during this last period since 2020. In low interest periods, the NAV dropped.

Conclusion & Risk

This fund is designed for income during inflationary or higher interest periods and performs nicely. It can and will generate muted growth during periods of individual asset growth. Again, it will be muted, but growth is likely. We rate this a buy with the likelihood of higher interest rates continuing for several years. In our belief, the day for easy money is gone, maybe for good. Investors shouldn’t expect high growth rates with the model; rather they can expect nice dividends with modest growth. During periods of bearish oil or low interest rates, this is a sell. In between, with interest rates falling at some point in the future, oil and gold, and precious metals will head up becoming a tailwind for asset increases. Again, for now, we continue a buy rating.

Read the full article here