ETF Overview

Vanguard Mega Cap Value ETF (NYSEARCA:MGV) owns a portfolio of about 140 U.S. large-cap value stocks. It has a razor-thin expense ratio of 0.07% which makes the fund quite compelling. The fund has been rangebound since mid-2021 and currently has a valuation slightly above its historical average. However, a recession may not be too far away, and we think investors should remain cautious as there may be significant downside risk. Hence, investors are advised to stay on the sidelines.

YCharts

Fund Analysis

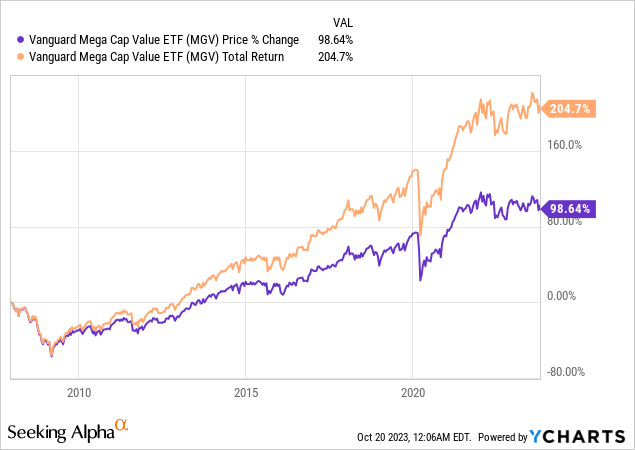

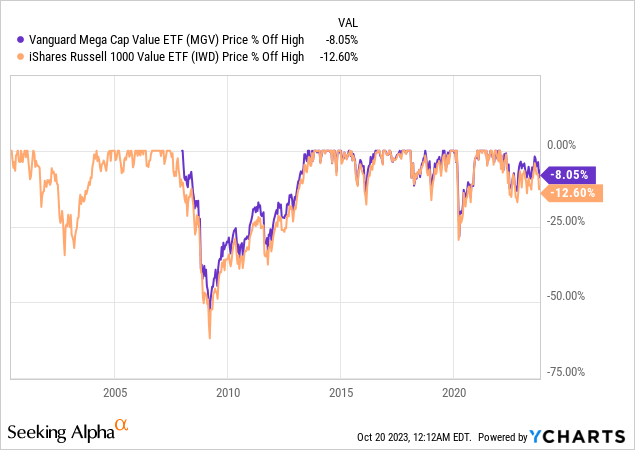

MGV’s fund price has been rangebound since mid-2021

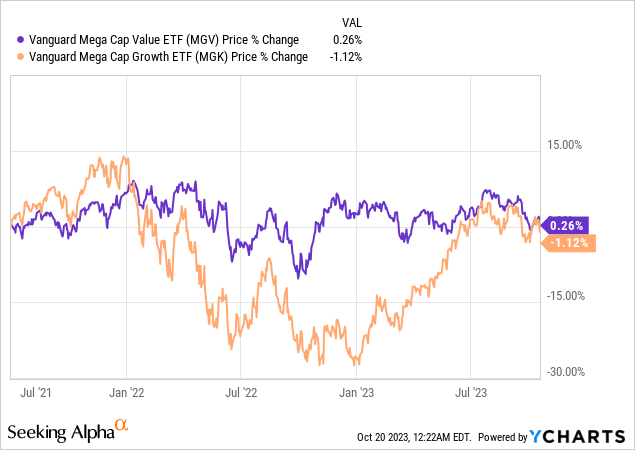

Value stocks in general fared much better during last year’s stock market correction, partly because valuations were not been inflated as much as many growth stocks during the pandemic. As can be seen from the chart below, the fund has fared very well since mid-2021. In fact, its fund price has been in a rangebound zone for the past two and a half years. In contrast, growth stocks suffered significant declines last year. As can be seen from the chart below, growth stock fund such as Vanguard Mega Cap Growth ETF (MGK) suffered over 40% decline from the peak reached in the beginning of 2022 to the end of 2022 before rebounding strongly in the first half of this year.

YCharts

Valuation still not cheap

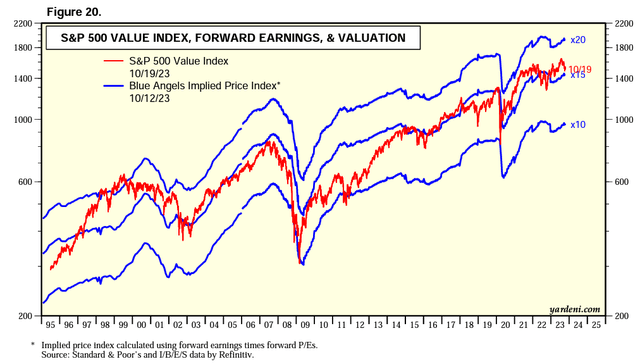

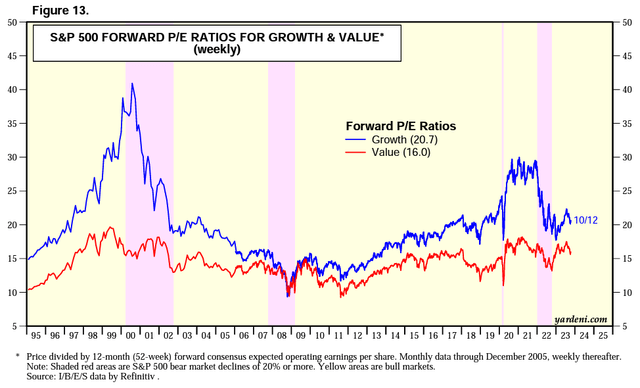

Below is a chart that shows the valuation of value stocks in the S&P 500 index. While S&P 500 value stocks are not exactly the same as the value stocks in MGV’s portfolio, there is a lot of overlap between the two, as both include large-cap value stocks. Therefore, we believe it should provide insightful information for us to evaluate MGV’s valuation. As can be seen from the chart below, the historical valuation of value stocks in the S&P 500 index typically deviates 1~2x above or below the forward P/E ratio of 15x. There were times in the past that the valuation of these value stocks went significantly below the forward P/E ratio of 15x. For example, in the past two recessions (the Great Recession in 2008/2009, and the initial outbreak of Covid-19), the forward P/E ratios of value stocks dropped down to only 10x. Other than these two recessionary environments, valuations of value stocks typically deviates by 1~2x above or below the forward P/E ratio of 15x.

Yardeni Research

The forward P/E ratio of value stocks in the S&P 500 index is currently about 16x. This is slightly higher than the median ratio of 15x, but significantly lower than the 20.7x forward P/E ratio of growth stocks. Therefore, value stocks do not appear to be expensive, nor cheap.

Yardeni Research

Investors should not ignore the downside risk

While MGV has held up very well since mid-2021, investors should not ignore the downside risk. As we have discussed earlier, the average forward P/E ratio of value stocks was compressed to only about 10x in the past two recessions. This compression can also be seen in the significant decline in MGV’s fund price. As can be seen from the chart below, MGV has declined over 50% in the Great Recession in 2008/2009 and over 25% in the initial outbreak of the pandemic in 2020. Unfortunately, this decline is comparable to the decline of the S&P 500 index. Therefore, MGV does not offer better protection in times of turmoil than the broader market.

YCharts

Is this the right time to invest?

While several economic metrics (job data, retail sales numbers) we have seen so far seems to suggest that the economy is still resilient despite aggressive rate hikes last year, we believe the economy will still head for a recession in the first half of 2024. The reason that it has yet to happen is because it generally takes a year for the effect of rate increase to propagate through the economy. While a soft-landing of the economy is possible, combating inflation may prove to be a much more difficult task than many thought of. This is because in a high inflation environment, labors will demand higher wages. This will result in higher commodity and services prices. This in term will result in labors demanding even higher wages to offset the increase in living expenses. Hence, inflation has the characteristic of spiraling upward. Therefore, the path towards the Federal Reserve’s long-term target of 2% inflation rate may take longer than the market expected. Hence, we do not see much room for the Federal Reserve to lower the rate any time soon. Unfortunately, this higher and for longer rate environment will inevitably lead to an economic recession.

As we have discussed in our article, valuation will likely be compressed significantly in the event of an economic recession. Not only that, we may also see earnings declining downward. This should result in a significant decline in MGV’s fund price. Hence, we think investors should really be careful at this stage of the economic cycle.

Investor Takeaway

MGV appears to be fairly valued right now. Given that an economic recession is not far away, we believe investors should remain cautions as downside risk can be quite high. Therefore, we suggest investors to patiently wait on the sidelines.

Additional Disclosure: This is not financial advice and that all financial investments carry risks. Investors are expected to seek financial advice from professionals before making any investment.

Read the full article here