Vir Biotechnology, Inc. (NASDAQ:VIR) is a commercial-stage immunology company focused on infectious diseases. VIR has a portfolio of drug candidates, primarily at the Phase 2 clinical stage, and has successfully brought a drug to market in the form of sotrovimab which was one of the initial treatments for the COVID-19 virus.

The stock has been hammered over the last several months. On July 20, 2023, VIR announced that its VR-2482 candidate to treat influenza didn’t meet either primary or secondary endpoints. Shares fell by 40% in response and have continued to trend down, though this has been true of the general biotech market as evidenced by the S&P Biotech ETF (XBI) being down close to 20% since that time as well.

All this has left VIR selling at extremely depressed levels. At the current share price, VIR’s market capitalization sits at $1.15B; its cash on hand alone is $1.9B, leaving the stock trading at a massive 40% discount to its cash alone, essentially valuing its portfolio at a negative expected value. This article investigates the optionality and value proposition that VIR provides.

Optionality

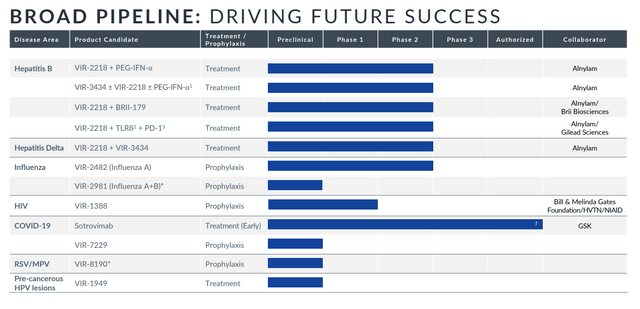

VIR has a very broad pipeline of drug candidates, with the majority at the Phase 2 clinical stage:

Company Presentation Sept 2023

Phase 2 candidates typically have greater upside than other phases as this is when the first determination of whether a candidate is effective or not is made. Phase 1 candidates are focused on the safety of the treatment, while Phase 3 candidates expand on the Phase 2 results and lead to eventual commercialization. A recent study on clinical trial attributes and their effect on share prices from September 2022 bears this out. My strength is certainly not in discussing the efficacy of the science, but VIR does appear to be near a sweet spot for catalysts in the near term based on its portfolio of candidates.

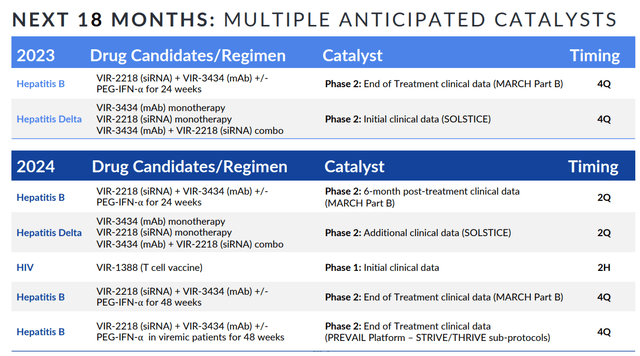

According to the company, it has the following expected catalysts within its portfolio over the next 18 months:

Company Presentation Sept 2023

The VR-2218/VR-3434 candidates focused on Hepatitis B both have End of Treatment clinical data setups during this period which could catalyze the stock.

Valuation

The valuation prospect is very clear. The company has a $1.9B cash pile compared to its $1.15B market cap, putting an EV of -$750m on the above portfolio of drug candidates. This would indicate the market is expecting the company to essentially keep burning cash with a null outcome. VIR has gone through over $400m in the last 12 months, so going at that rate would give it about 2 years of runway before its cash meets its current market cap, which is essentially the period for most of its current trials.

A counterpoint to this is that the market may not see any value in these drug candidates which is why it has a negative EV on the portfolio. I believe the recent hirings the company has made indicate that its staff and management have more faith than the market does:

- June 2023 – hiring of Sasha Ellis (ex-Marinus Pharmaceuticals) as Chief Corporate Affairs Officer

- May 2023 – hiring of Jeff Calcagno (ex-J&J) as Chief Business Officer

- February 2023 – hiring of Sung Lee (ex-Gilead) as Chief Financial Officer, in organized transition from long-time CFO Howard Horn

The CBO hiring paid immediate dividends as the company was able to land a $50m funding grant in October 2023. The pedigrees of these employees indicate that they see a bright future ahead for the company.

The question I would ask is, assuming the portfolio has some expected value, why would one of VIR’s partners not launch a takeover offer? Even offering a 25-35% premium at this point, a takeover would essentially be paid for by the cash on hand, allowing the acquirer to essentially obtain the portfolio for nothing (after closing and transition costs).

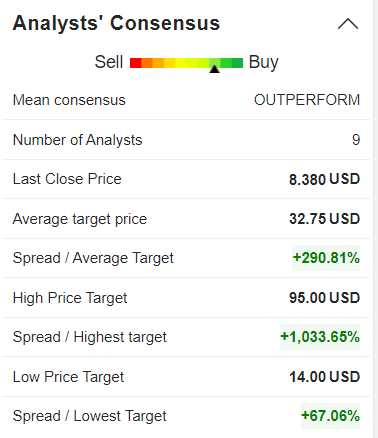

There would likely be pushback from investors and that kind of offer would likely put the company in play with other suitors. Current analyst targets range from $14 to $95 US, with the $14 being driven by a recent downgrade from Bank of America:

MarketScreener

The Takeaway

The combination of the negative influenza results and a general malaise in the entire biotech sector has seen the valuation of VIR drop down to extraordinary levels. With the portfolio expected to see major potential catalysts over the next 24 months, if the company continues as a standalone entity, even negative results could see some value still left in the company in the form of cash on hand. The best-case scenario sees positive results from any of its trials with a re-rating in line with the analyst targets or seeing the company put into play.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Best Value Idea investment competition, which runs through October 25. With cash prizes, this competition — open to all contributors — is one you don’t want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

Read the full article here