Business Overview

Rocket Companies (NYSE:RKT) is a Detroit‑based company consisting of tech-driven mortgage, real estate and financial service businesses. Its portfolio includes: Rocket Mortgage (mortgage lender), Amrock (title insurance), Rocket Money (personal finance app), Rocket Homes (home search platform and real estate agent referral network), Rocket Loans (personal loan), Lendesk (Canadian software company), and other fintech companies. RKT’s flagship business is Rocket Mortgage, which has provided nearly $1.6 trillion in home loans since inception.

RKT originates mortgage loans that are sold either to government backed entities or to investors in the secondary mortgage market. Thus, it does not need to hold significant capital to grow our origination business. Its income mainly comes from the gain on sale of loans; loan origination fees (credits), points and certain costs; the change in fair value of interest rate lock commitments (“IRLCs”) and loans held for sale; the gain on forward commitments hedging loans held for sale and IRLCs; and the change in fair value of originated mortgage servicing rights (“MSRs”).

In the most recent reporting quarter Q2 2023, RKT’s results beat on both revenue and earnings and announced expectations for up to $200M of annualized cost savings. However, RKT stock prices dropped by nearly 34 percent since its last earning report in August. Since its heyday in 2021, RKT stock price has declined by about 78 percent.

In the second quarter, RKT returned to positive adjusted EBITDA of $18 million improved considerably relative to losses of $79 million and $204 million in Q1 and Q4, respectively. The company had $3.8 billion of available cash and $6.4 billion of mortgage servicing rights by the end of Q2. The $3.8 billion of available cash consists of $883 million of cash on the balance sheet and an additional $2.9 billion of corporate cash used to self-fund loan originations. RKT had ample liquidity, totaling $8.6 billion on June 30, including available cash plus undrawn lines of credit and undrawn MSR lines. Its total current asset was $11.2 billion and total current liability was $2.7 billion. By the end of Q2, RKT’s mortgage servicing portfolio included more than 2.4 million loans serviced with approximately $500 billion in unpaid principal balance. The company expected adjusted revenue to be in the range of $850 million to $1 billion.

The Fundamental Reason Why Rocket Mortgage has Great Potential

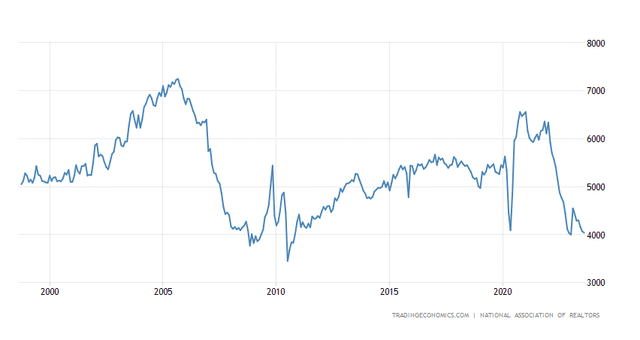

RKT’s performance is closely linked to the health of US housing market. The current housing market is depressing as the existing home sales is near its lowest level in the past 25 years as shown in the following chart.

US Existing Home Sales

Tradingeconomics

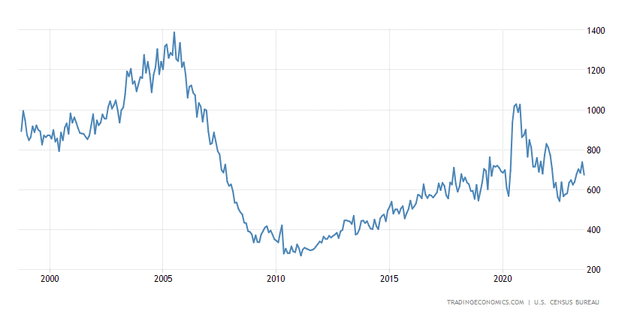

The shock of rapidly increased interest rate had forced many people to pause or postpone their housing hunting for the moment. Many would-be house sellers do not want to sell right now because they do not want to give up the ultra-low mortgage rates they enjoyed. But the demand for housing is strong. Thus, it caused the new home sales to rise since last year. But the increase in the new home sales cannot compensate for the deficit of shrinking existing home sales.

US New Home Sales

Tradingeconomics

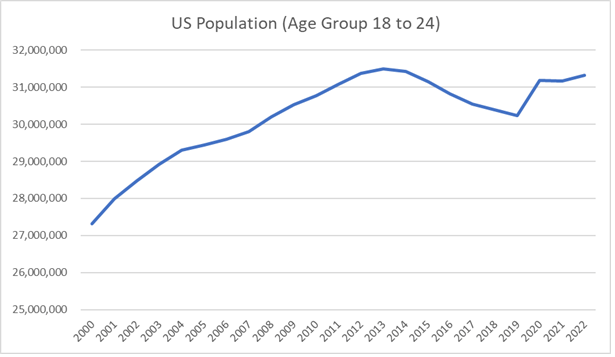

On the other hand, the demographic trend suggests that demand for housing is close to its peak right now. See the following chart using data from the Census Bureau. In 2013, the US population of the age group 18 to 24 was at its peak around 31.5 million. Ten years later as of today, these people are in the age range of 28 to 34. They are at the stage of forming households and considering homeownership in the life. The limited housing supply and the high interest rates may temporarily prevent many of them from meeting their goals. But, their demand is still there and will be unleashed once the supply side is unfrozen.

The US Census Bureau

The demographic trend is a powerful force that would eventually overcome the obstacle of high interest rates. The unbalance of housing demand and supply today suggests that the current low level of home sales is not sustainable. I expect the housing transaction volume to rise significantly in the next few years.

Rocket Mortgage is Well-Positioned to Benefit

Although RKT had an operating loss during the first six months of FY2023, its second quarter is profitable. The loss was largely due to the change in fair value of mortgage servicing rights (MSRs) during the first quarter. In the second quarter, the change in fair value of MSRs was positive. Given that the current bond yield increases, RKT may have to experience another negative change in fair value of MSRs in the third quarter this year, but I expect that the reduction would be smaller than that in the first quarter. Also, due to the market expectation that we are much closer to the end of credit tightening cycle than to the beginning, I think the negative revision in fair value of MSRs would also be close to the end and its impact on RKT’s earnings would be diminished in the next few quarters.

The company also is disciplined in the operation. Its Q2 total expenses of $1.10B edged up from $1.08B in Q1 since spring and summer are the busy seasons. Nevertheless, the total expense dropped from $1.31B in Q2 2022 as the result of cost control.

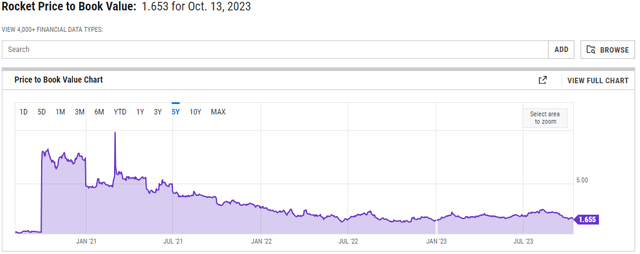

Meanwhile, the valuation of RKT is attractive. Mortgage earnings and margins are cyclical. Due to the volatile nature of mortgage earnings, it is natural that stock prices of mortgage companies like RKT and its peer UWM Holdings Corporation (UWMC) had trended downward in this credit cycle. Since earnings and cash flow of mortgage lenders tends to be volatile during the period of the rapid interest rate changes, I would like to use price/ book value since the book value can be treated as a proxy for the company earnings capabilities.

RKT’s price-to-book value ratio is currently 1.653, slightly above the lowest level in 2022. At the same time, its close peer UWMC has a price-to-book value ratio of 3.899, well above its 2022 level. If one is going to invest in the coming back of housing market, among mortgage lenders, valuation of RKT is more attractive in this sense.

YCharts

Major Investment Risk Factors

The biggest risk factor is that instead of a soft landing or a mild recession, the US faces a more severe recession in 2024. This could bring down the housing market and the existing home sales could go down to the level seen during the 2008-2010 period. Since RKT sold most of its mortgage either to government backed entities or to investors in the secondary mortgage market, somehow the credit risks such as delinquency and foreclosure should not have a direct and significant impact on RKT’s business. However, the possible stock market turmoil in this deep recession scenario would very much take RKT price down as well.

Another risk factor is the leadership transition. The new CEO of RKT has an impressive record of software product development. But he does face a highly uncertain time with many difficult macroeconomic challenges ahead and have only limited C-level executive experiences. Whether the new CEO can succeed in leading RKT go through the difficult future is still an open question.

Conclusion

The US housing market has slowed down since the high mortgage rates depressed the existing home sales. However, the powerful demographic trend suggested that underline demand is actually strong and the housing market will recover since the Fed is near the end of rate hiking cycle. Although the risk of a severe recession remains, Rocket Companies, Inc should benefit from the demographic-driven housing market recovery. The financial risk is manageable as RKT sold most of its loans to government backed entities or to investors in the secondary mortgage market.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Best Value Idea investment competition, which runs through October 25. With cash prizes, this competition — open to all contributors — is one you don’t want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

Read the full article here