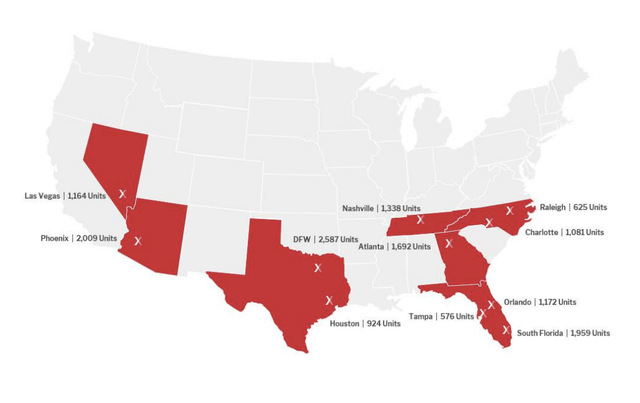

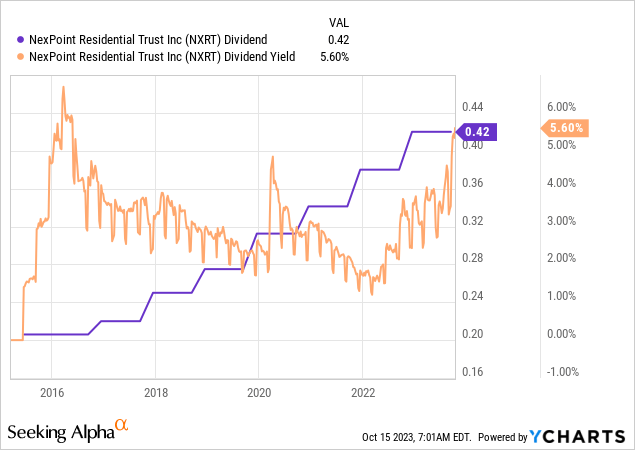

NexPoint Residential Trust (NYSE:NXRT) has been rocked by rising interest rates with the common shares down 29% year-to-date to trade at its lowest level since 2018. The pullback has been material with the externally advised REIT now swapping hands at a price to trailing 12-month funds from operations of 9.01x, around 30% lower than its peer group median. The REIT focuses on multifamily properties primarily located in the Sun Belt region with a portfolio of 40 apartment properties. The portfolio’s stats as of the end of the fiscal 2023 second quarter were good with physical occupancy at 93.9% across its 15,127 units which held a weighted average effective monthly rent of $1,497 per unit. NexPoint last declared a quarterly cash dividend of $0.42 per share, unchanged from its prior payout and for a 5.6% annualized forward yield.

NexPoint Residential Trust June 2023 REITWeek Presentation

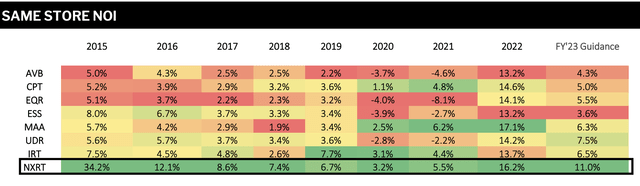

The REIT targets investments in class B multifamily properties that broadly come with a value-add component where NexPoint can invest capital to provide amenities while maximizing returns for shareholders. The REIT’s value-add program forms a distinctive part of its investment thesis as it seeks to provide its tenants with a range of lifestyle amenities typically found in newly constructed multifamily properties from pool areas, to fitness centers, and playgrounds at a reasonable price. Hence, NexPoint has realized same-store net operating income that’s trended above its peer group with the second quarter seeing year-over-year NOI growth of 7.6%. NexPoint is guiding for a full year 2023 NOI growth of 11%.

NexPoint Residential Trust June 2023 REITWeek Presentation

Debt Represents A Headwind

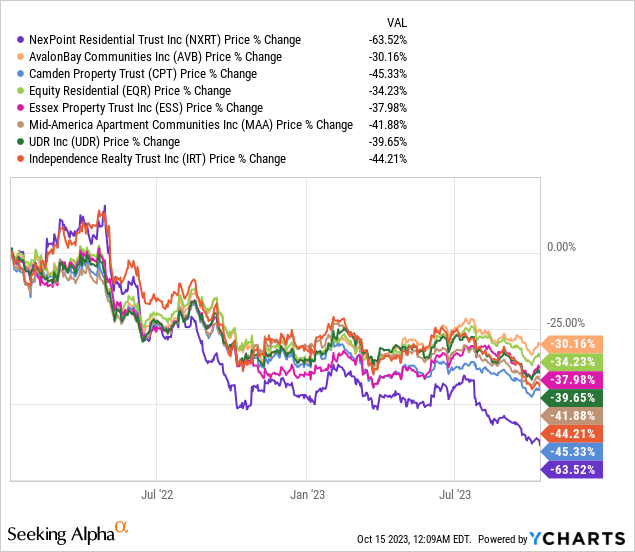

NexPoint currently swaps hands at $30 per share, falling markedly from its 2022 peak of just under $93. The REIT has dipped around 63.5% since the start of 2022, to become the worst performing multifamily property owner against the bulk of the multifamily REIT universe. REITs have fallen to record lows on the back of a Fed funds rate currently sitting at 22-year highs of 5.25% to 5.50% with higher for longer spelling an elongation of interest expense and refinancing headwinds.

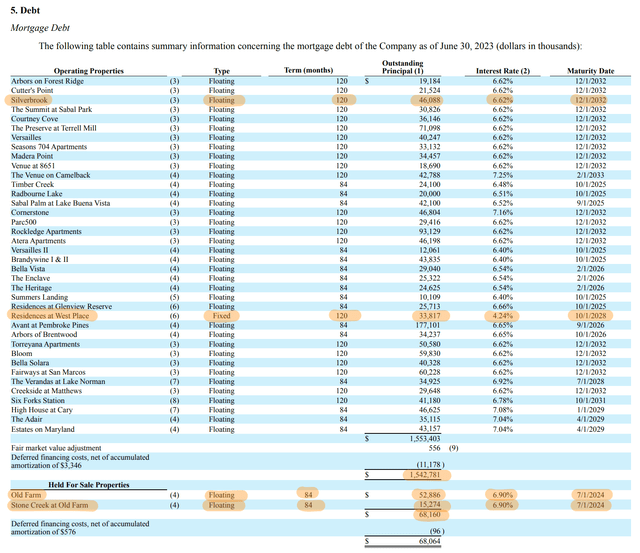

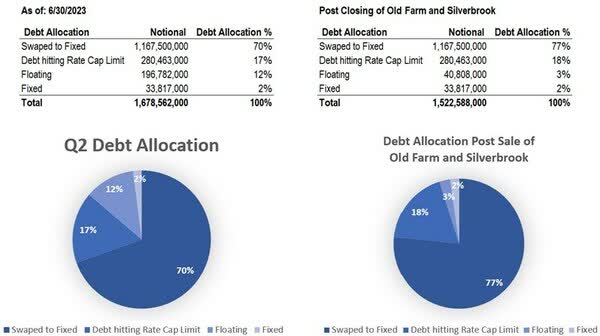

What’s with the difference in performance especially with NexPoint sporting strong NOI outperformance over its peers? Floating-rate debt and flagging core FFO. NexPoint held a total debt of $1.67 billion at the end of its second quarter. This was mainly comprised of $1.54 billion in mortgage debt that’s 97.8% floating rate mortgage debt with interest rates ranging from 6.62% to 7.25%. The fixed-rate mortgage actually holds the lowest interest rate at 4.24% with maturity coming up in 2028. NexPoint’s debt maturities on the floating debt are very long-dated with the bulk of the debt coming in 2032. There are no real debt maturities in 2023 with around $68.1 million coming due in 2024 from properties held for sale.

NexPoint Residential Trust Fiscal 2023 Second Quarter Form 10-Q

The REIT realized a quarterly interest expense of $14.5 million during its second quarter, up 17% from its year-ago period. The divestiture of two properties, one of which was held for sale at the end of the second quarter, was completed post-period end for $67 million to $69 million in net sales proceeds. This was at a combined trailing nominal cap rate of 4.96% and means NexPoint can address its 2024 maturities. However, it’s worrying that NexPoint has had to proceed with the divestment of both of these. Selling off properties to address debt is not controversial in itself but with a portfolio of just 40 properties, the sale would represent 5% of its portfolio.

FFO And Dividend Coverage

NexPoint Residential Trust

Around 77% of NexPoint’s debt has been swapped to fixed rates, up from 70% prior to the divestitures. The REIT is also now chasing the sale of another three properties, Timber Creek, Radbourne Lake, and Stone Creek at Old Farm, by the end of the first quarter of fiscal 2024 to continue to deleverage its portfolio. The 40 property portfolio drove second-quarter revenue of $69.6 million, up 5.8% year-over-year but still missing consensus estimates. Same-store properties average effective rent increased by 7.9% with NexPoint reporting a net loss of $4 million. FFO came in at $19.8 million, up from $17.6 million in the year-ago quarter.

Core FFO came in at $20.4 million during the second quarter, up marginally from $20.3 million in the year-ago comp but down by roughly 1 cent on a per share basis with core FFO at $0.77 per share. This provided a significant 183% coverage against the dividend or a 55% payout ratio. Hence, the current payout is safe even against the interest rate disruption with the REIT possibly having enough leeway to hike its payout again sometime next year. The debt load is also manageable on the back of its long-dated maturities and the use of swaps. The current yield has moved beyond the early 2020 crash for its highest since 2016 however I’m rating the commons as a hold as the portfolio gets disrupted by the property sales.

Read the full article here