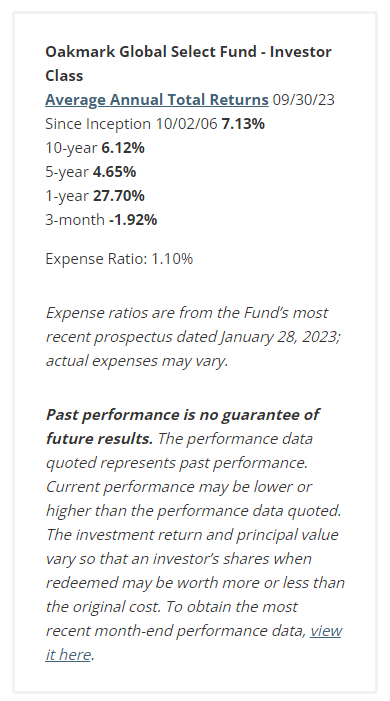

The Oakmark Global Select Fund (OAKWX, the “Fund”) returned 27.70% for the fiscal year ended September 30, 2023, outperforming the MSCI World Index (net), which returned 21.95%. For the most recent quarter, the Fund returned -1.92%, compared to the benchmark’s return of -3.46%. The Fund has returned an average of 7.13% per year since its inception on October 2, 2006, outperforming the MSCI World Index (net)’s annualized gain of 6.43% over the same period.

Charter Communications (CHTR, U.S.), a telecommunications and mass media company, was the top contributor to the Fund’s performance for the quarter. Second-quarter broadband subscriptions for Charter Communications grew by 77,000 sequentially, beating consensus expectations of 13,000 and roughly doubling its growth year-over-year. Unit growth outperformed peers, even after adjusting for Charter’s rural initiative, which contributed 26,000 subscriptions. Charter’s mobile net adds were strong at 648,000, and net adds have been over 600,000 each of the last three quarters since Charter launched Spectrum One, which includes one free mobile line for 12 months. Adjusted earnings growth was roughly flat, but we expect it to accelerate over time as the company’s financials are no longer negatively impacted by its investments in marketing personnel and the promo roll-off dynamic begins. While faster unit growth does depress adjusted earnings in the near term, we believe Charter’s strategy will prove valuable to long-term shareholders.

CNH Industrial (CNHI, Italy), which designs, manufactures, and distributes agricultural and construction equipment, was the top detractor for the quarter. CNH Industrial’s share price fell following its second-quarter results, as agriculture equipment sales rose 5% in local currency, a slowdown from the prior quarter. This performance fell below market expectations due to destocking activity in Brazil and some production ramp-up issues for its new Patriot sprayer. We believe the production issues are temporary while the destocking actions will better position the business for the midterm. Pricing power remains quite strong and increased by roughly 7%, and precision agricultural sales grew by 21%. While the market was overly focused on near-term demand and sales growth, the agriculture equipment division produced its highest quarterly margin ever at 16.8%—an encouraging development that supports our view of the company’s long-term profitability. Further, the much smaller construction business delivered strong results, including its own quarterly margin record. Management maintained guidance for the rest of the company’s current fiscal year and indicated it expects to exceed the 2024 targets laid out at a capital markets day in 2022. We recently met with CEO Scott Wine at the company’s offices. He expressed confidence in the company’s ability to drive much better through-cycle financial performance while avoiding the company’s previous mistakes. He also believes the company’s share price is materially undervalued, and although he would prefer to invest in the business, he sees an opportunity to increase returns to shareholders via share repurchases. We believe CNH Industrial remains a solid business in an attractive industry that is run by a much-improved management team.

Alphabet (GOOG, GOOGL, U.S.) was the top contributor for the fiscal year. Alphabet reported multiple strong sets of earnings releases over the past year, and its results generally exceeded consensus estimates across key metrics. Most recently, search revenue growth accelerated from 5% to 6.5% sequentially in the second quarter, a notable development given lingering economic uncertainty and broader advertising weakness. Cloud growth remained at 30%, stable versus the previous quarter, despite continued headwinds from customers optimizing cloud usage. Margin progression also continued, and cloud margins reached 5%. CFO Ruth Porat emphasized that the largest impact from the company’s cost-saving initiatives will not be felt until 2024. YouTube continues to prioritize its Shorts segment, which is experiencing strong viewership growth. Although this is a near-term revenue headwind, we believe Shorts’ monetization will accelerate over time. Addressing the year’s hottest topic, CEO Sundar Pichai said Alphabet is an “AI-first company” that is “extremely well-positioned as AI reaches an inflection point.” At Alphabet’s annual developer conference in May, it showcased an impressive array of new AI-powered consumer tools to be rolled out over the course of the year. Investors reacted positively to these presentations, which highlighted the company’s impressive innovations in AI technologies. Overall, we believe the company is positioned well to reap the benefits of the scale of its search business and years of its investment into AI capabilities. We also appreciate that the company is undergoing a transformation on how it views cost discipline and efficiency.

Credit Suisse Group (Switzerland) was the top detractor for the fiscal year. We were shareholders in Credit Suisse for more than two decades. Before the global financial crisis, we sold most of our shares due to significant share price appreciation, and then we rebuilt that position in the wake of the financial crisis. That holding period was troubled and full of controversy. Credit Suisse’s investment bank experienced repeated lapses in risk management concurrent with its attempts to compete with more scaled peers. Despite this, we (in hindsight, incorrectly) remained focused on our sum-of-the-parts valuation and gained comfort in the strong performance of the company’s wealth management, asset management and Swiss Universal Bank businesses as they continued to generate better than average returns. We believed that the three better businesses represented good value and that the investment bank was repairable. Despite numerous attempts by multiple leadership teams at Credit Suisse, our thesis was proven wrong. Finally, after the last investment banking restructuring plan and capital raise released last October, we determined it was time to reevaluate our investment thesis as we do whenever there is a fundamental change in one of our holdings. The plan provided no insight into the proceeds from the asset sales or into the costs of restructuring the investment bank. As such, we concluded that an accurate business valuation was indeterminable and compounded by inevitable years of cash outflows. In addition, Credit Suisse’s key wealth management franchise experienced elevated client withdrawals, and the risk of reputational damage to its wealth franchise brand had intensified. Ultimately, we decided to exit our position in the fall of 2022 and completed our exit in early March of this year.

We did not initiate or eliminate any positions during the third quarter.

Geographically, we ended the quarter and fiscal year with 54.7% of the portfolio in the U.S., 34.2% in the U.K. and Europe, and 11.1% in Asia.

We thank you for your continued support.

David G. Herro, CFA | William C. Nygren, CFA | Tony Coniaris, CFA |Eric Liu, CFA | M. Colin Hudson, CFA | John A. Sitarz, CFA, CPA

|

The securities mentioned above comprise the following preliminary percentages of the Oakmark Global Select Fund’s total net assets as of 09/30/2023: Alphabet Cl A 8.2%, Charter Communications Cl A 6.5%, CNH Industrial 4.2% and Credit Suisse Group 0%. Portfolio holdings are subject to change without notice and are not intended as recommendations of individual stocks. Access the full list of holdings for the Oakmark Global Select Fund as of the most recent quarter-end. The information, data, analyses, and opinions presented herein (including current investment themes, the portfolio managers’ research and investment process, and portfolio characteristics) are for informational purposes only and represent the investments and views of the portfolio managers and Harris Associates L.P. as of the date written and are subject to change and may change based on market and other conditions and without notice. This content is not a recommendation of or an offer to buy or sell a security and is not warranted to be correct, complete or accurate. Certain comments herein are based on current expectations and are considered “forward-looking statements”. These forward looking statements reflect assumptions and analyses made by the portfolio managers and Harris Associates L.P. based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Actual future results are subject to a number of investment and other risks and may prove to be different from expectations. Readers are cautioned not to place undue reliance on the forward-looking statements. The percentages of hedge exposure for each foreign currency are calculated by dividing the market value of all same-currency forward contracts by the market value of the underlying equity exposure to that currency. The MSCI World Index (NET) is a free float-adjusted, market capitalization-weighted index that is designed to measure the global equity market performance of developed markets. The index covers approximately 85% of the free float-adjusted market capitalization in each country. This benchmark calculates reinvested dividends net of withholding taxes. This index is unmanaged and investors cannot invest directly in this index. On occasion, Harris may determine, based on its analysis of a particular multi-national issuer, that a country classification different from MSCI best reflects the issuer’s country of investment risk. In these instances, reports with country weights and performance attribution will differ from reports using MSCI classifications. Harris uses its own country classifications in its reporting processes, and these classifications are reflected in the included materials. Because the Oakmark Global Select Fund is non-diversified, the performance of each holding will have a greater impact on the Fund’s total return, and may make the Fund’s returns more volatile than a more diversified fund. Investing in foreign securities presents risks that in some ways may be greater than U.S. investments. Those risks include: currency fluctuation; different regulation, accounting standards, trading practices and levels of available information; generally higher transaction costs; and political risks. All information provided is as of 09/30/2023 unless otherwise specified. |

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here