Investment Thesis

Barclays PLC (NYSE:BCS) share prices appear to have plateaued recently. In my view, this could be due to the reorganization that is undergoing in the company, ranging from management to resource optimization. From a long-term perspective, I am bullish on the stock because I believe this reorganization will be a major growth catalyst in the long run.

However, given the uncertainty surrounding the company’s recent reorganization, such as the cutting jobs in trading and investment bank, the short-term outlook of the company shares is neutral, as evidenced by the plateaued share prices. Additionally, from my technical analysis, the stock’s outlook is neutral, warranting a hold rating as we wait for confirmation from the technical indicators. Long-term-oriented investors can consider buying when the price breaks above the resistance level of $8.07.

Plateaued Share Price: My Thoughts

BCS share prices appear to have plateaued, indicating a neutral outlook or a potential break out.

Author Analysis On Market Screener

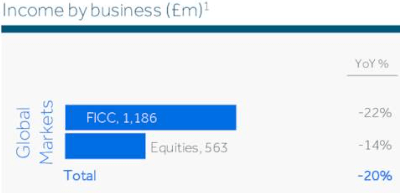

In my view, this trend could be due to several reasons. To begin with, I believe it could be due to the weak performance and outlook of its trading and investment bank segments, which account for more than 50% of its revenue. The company reported a decline in its fixed income, currencies, and commodities [FICC] trading revenue in the second quarter of 2023, which decreased by 22% year-over-year to £1.6 billion. Further, the company also reported a decline in its equities trading revenue, which decreased by 14% year-over-year to about $0.56 billion.

BCS Q2 2023 Presentation

I believe this weak performance indicates a weak financial outlook, which could have contributed to the current share price trend.

Another reason for the share trend is the uncertainty and speculation surrounding the company’s future strategy and leadership amid the pressure from its activist investor, Edward Bramson. Bramson, who owned about 6% of the company’s shares, was pushing for the company to reduce its trading and investment bank operations and focus more on its retail and commercial banking segments. Eventually, he opted to sell his stake in the company in 2021. Notably, his activist campaigns against Barclays Investment Bank date back to 2018, explaining why the company’s shares have plateaued since then.

I believe this issue could have caused the company’s shares to plateau. I tend to believe this could have influenced the company’s recent plan to cut hundreds of jobs in the trading and investment bank, which could add more uncertainty to the outlook of the company’s future performance. In a nutshell, the company’s plateaued share prices could be a result of the uncertainty in the trading and investment bank, which I expect to continue in the short and medium term, as evidenced by the recent plan to cut hundreds of jobs in the segment.

Efficiency Measures Or Bowing Down To Pressure?

Following Bramson’s campaign for reforms at BCS’ trading and investment bank, the company plans to remove hundreds of positions in the division. Furthermore, the company is considering selling a portion of its payments business in the United Kingdom. Given this context, it may look like the corporation is aiming for efficiency, but it is also possible that it is succumbing to pressure from what Bramson proposed before selling his stake.

The planned layoffs would be at least the third wave of downsizing at Barclays in the last year. The bank cut about 200 personnel in November 2022, then another 100 in April this year, primarily in investment banking, due to a drop in transaction volume in the first half of 2023. I expect the layoffs to save the company about $250 million in annual expenses. I believe the company is not succumbing to pressure from Bramson’s proposal but is eyeing efficiency because other companies, such as Goldman (GS), are also facing the same decisions. In fact, Goldman is about to execute a fourth headcount trim of the past 12 months. In summary, I believe BCS is aiming at efficiency and not succumbing to pressure, and I expect the company to realize better profit margins due to the reduced expenses.

New Appointment: Brighter Days Ahead?

Barclays PLC recently appointed Michael Del Giudice as the chairman of its financial sponsors group, which advises private equity firms on their transactions and financing. In my view, I believe this was a prudent decision because of several reasons. First, Giudice has over 30 years of investment banking experience and has worked with some of the leading private equity firms in the industry, such as Blackstone, Warburg Pincus, Carlyle, Onex, EQT, and Centerbridge, which translates to great experience and expertise.

He has also advised on and arranged financing for many transactions that helped to shape the private equity industry over the last decades. In my opinion, his expertise and connections could help Barclays attract more customers and deals in the financial sponsors market, which is a key source of revenue and growth for the company.

Secondly, his appointment could also enhance Barclays’ competitive advantage and innovation, as it could differentiate the company from its rivals, such as JPMorgan Chase (JPM), Goldman Sachs, and Morgan Stanley (MS). I believe Giudice will leverage his knowledge and experience to provide his clients with more value-added solutions and products, such as centralized fixed-income trading, algorithmic trading, and ESG integration.

Lastly, his appointment could also improve Barclays’ profitability and efficiency, as it could optimize its capital structure, reduce its costs, and increase its margins. Giudice could help Barclays to manage its risk exposure and balance sheet more effectively by selecting the most suitable and profitable deals for the company. He could also help Barclays to streamline its operations and processes by simplifying and standardizing its financial sponsor’s practice across different regions and segments. In summary, I believe the appointment of Guidice is a prudent choice as his experience can help the company come up with innovative ideas and optimize resources, resulting in more efficiency and profitability.

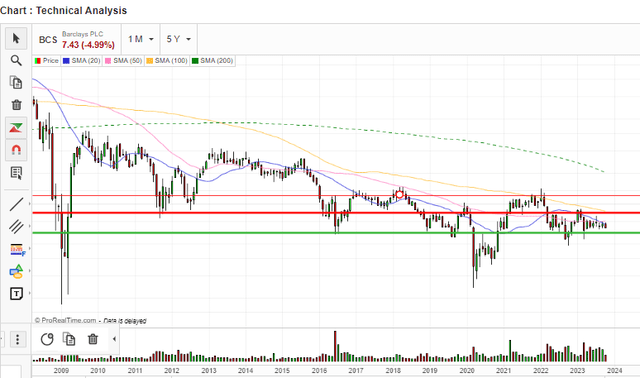

Technical Analysis

Based on different indicators, here is my technical analysis of BCS. First off, the horizontal arrows on the chart suggest that the stock is in a neutral trend. The price is bouncing between the $7.39 and $8.07 support and resistance levels. The price is also close to the mid-term moving average of $7.47, indicating a buyer-seller equilibrium.

Author Analysis On Market Screener

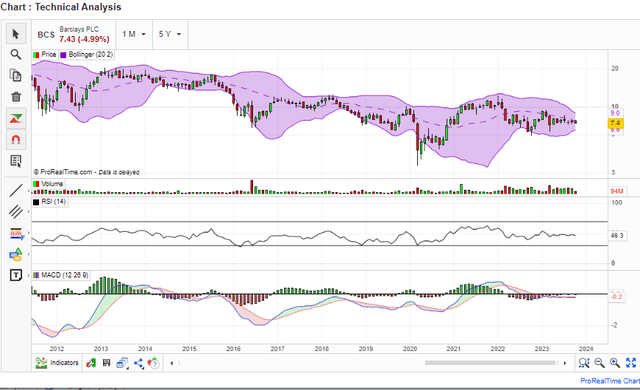

The stock has a neutral overall technical outlook, as indicated by the mixed signals from the oscillators and moving averages. The RSI is at 46.3, which is neither overbought nor oversold. The Bollinger Bands are narrowing, which implies low volatility. Further, the MACD is below the signal line, which indicates a bearish crossover.

Author Analysis On Market Screener

Based on this analysis, the stock has some alerts that may affect its future performance, such as being near or below the moving averages, being in a support area, and having a neutral RSI. These alerts may indicate a potential reversal or continuation of the current trend.

In conclusion, I recommend holding the stock for now and waiting for more confirmation from the technical indicators before making a buy or selling decision. If you are looking for a long-term investment, you may consider buying the stock when it breaks above the resistance level of $8.07, which would confirm the bullish long-term trend. If you are looking for a short-term trade, you may consider selling the stock when it breaks below the support level of $7.39, which would confirm the bearish short-term trend.

Risks

Investing in BCS, like any other investment, has some risks. Here are some of the risks associated with investing in the company.

- Regulatory probes and sanctions: Barclays is being probed by the UK financial regulator for suspected persistent failings in its compliance and anti-money laundering systems. This could result in fines, penalties, reputational damage, and bank business loss.

- Management Changes: The company has been undergoing reforms that have extended to management changes. In my view, new management comes with new visions, which, in some cases, could be detrimental. As a result, investors should be wary of the recent management changes in BCS.

The Bottom Line

According to my analysis, BCS is confronted with uncertainties that appear to have plateaued its share price movement. Given the current restructure centered on management changes and efficiency-focused strategies, the corporation may be preparing for a long-term growth objective. However, patience is required before making financial judgments based on technical analysis. According to my analysis, long-term investors could consider buying when the price breaks over the $8.07 resistance level.

For those looking for a short-term trade, you may consider selling the stock when it breaks below the support level of $7.39, confirming the bearish short-term trend. In general, I recommend patience as we wait for these entry points and as the company takes shape following the recent restructuring taking place.

Read the full article here