Since we last wrote about utility equities, they have continued their downward trend. Rising interest yields on U.S. Treasury bills and bonds are typically inversely related to utility stock dividend yields. As a result, the sector has struggled. In fact, of all the utility stocks we track, only two have a positive total return as of this writing.

Many utility stocks are trading at low valuations and decade-high dividend yields. Although they may go down further, it is a buying opportunity for those seeking income with dividend growth. Eventually, interest rates will stabilize and turn, and investors may turn to utilities for income.

We discuss three undervalued utility stocks that are also dividend growth stocks for long-term income.

An Opportunity to Buy Utilities

American States Water

American States Water (AWR) is the first stock on our list. The utility operates in California but has a presence in eight other states. Although mainly a water and wastewater utility, it also provides electricity. The firm is the parent company of Golden State Water Company (69% of 2022 revenues) and Bear Valley Electric Service, Inc. (8% of 2022 revenues). In addition, its American States Utility Services, Inc. (23% of 2022 revenues) provides water and wastewater services to 11 U.S. military bases through 50-year military contracts.

In total, American States Water serves roughly one million customers. Total revenue was $491.5 million in 2022 and $579.2 million in the last twelve months.

AWR Investor Relations

The utility is mainly a pure-play regulated utility with a monopoly in its service area, making it attractive. Although it does have unregulated contracted services, the risk is low because it is to the military with decades-long contracts providing stability and a guaranteed revenue stream. Revenue grows slowly because of the small service footprint and focus on organic growth. However, earnings per share have increased by about 8.3% in the past five years.

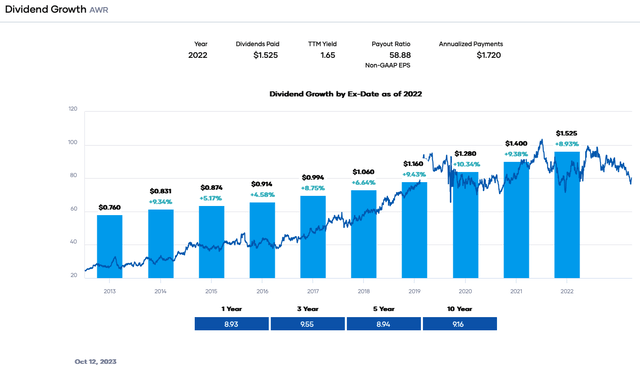

From a divided perspective, American States Water is second to none. It has the longest dividend growth streak at 69 years. Moreover, it is one of the three water utilities that are Dividend Kings. The average annual dividend growth rate is about 8% to 10% annually. The last dividend increase occurred recently, in August 2023.

The forward dividend yield is only ~2.1%, the highest since 2017. The utility has yielded more in the past, but the popularity of water utility stocks has lowered the percentage. That said, the forward dividend yield exceeds the five-year average of ~1.7%.

The yield comes with solid dividend safety, too. A 59% payout ratio is moderate for utilities and suggests more increases to come. It is unlikely that American States Water will stop the growth because of the 69-year streak. Operating cash flow (OCF) of $78.7 million in the past twelve months covers the dividend payout of $58.8 million. Coverage is usually higher because OCF is generally $100+ million.

The balance sheet is sound, with an A+ upper medium investment grade credit rating. Additionally, Portfolio Insight’s dividend quality grade, a measure of safety based on growth, profitability, and the balance sheet, is an ‘A+,’ meaning little risk of a cut exists now.

American States Water is rarely undervalued. The equity usually trades at a price-to-earnings (P/E) ratio of 30X to 40X. Today, the forward P/E ratio is ~29X earnings. We view the stock as a long-term buy.

Portfolio Insight

Spire

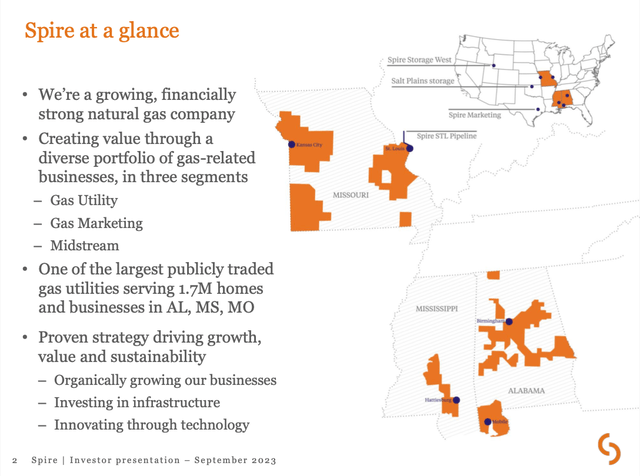

The second stock on our list is Spire (SR), a natural gas utility in Missouri, Mississippi, and Alabama. Besides the regulated operations, the company has unregulated segments, including marketing, midstream, and storage. Spire Midstream owns the MoGas 263-mile pipeline, while Spire Storage West owns a 23 bcf facility in Wyoming with five transmission pipelines.

The utility serves approximately 1.7 million residential, commercial, and industrial customers. Total revenue was $2,198.5 million in 2022 and $2,670.1 million in the past twelve months.

SR Investor Relations

Spire has become one of the largest regulated natural gas utilities through acquisitions. What was once a small firm has become a much bigger player. The firm is seemingly focusing on its unregulated operations. It has acquired Spire Salt Plains, another ten bcf storage facility in Oklahoma, and is purchasing Omega, a pipeline connecting to Fort Leonard Wood.

Revenue has grown by almost 7% annually in the past decade. However, EPS has grown only at 3.3% CAGR over the same time because of regulatory adjustments, mild winters, lower gas prices, and higher interest payments. Spire has also struggled with the STL pipeline court case and integration of acquired assets. However, the new CEO may emphasize operations and organic growth, increasing profitability.

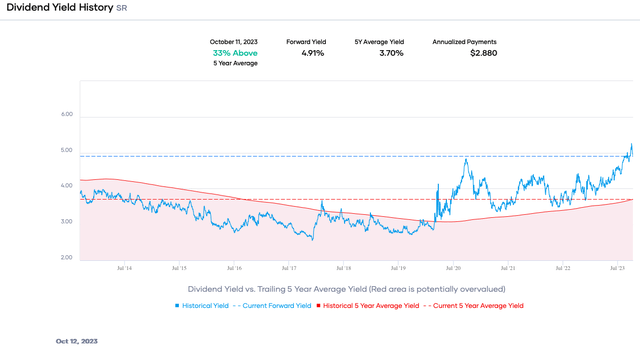

Spire is another dividend growth utility with 20 years of increases, making it a Dividend Contender. The growth rate is around 5% annually. The nearly 16% drop in the share price has pushed the dividend yield up to ~4.9%, just short of a 10-year-high. It was more than 5% before the share price bounced back. The lofty yield comes with a payout ratio of ~72% based on earnings and 64% on OCF. But OCF was higher in the past two years, and coverage was better. Moreover, the dividend quality grade is solid at a ‘B+.’

Spire’s share price has declined because of challenges specific to it and rising T-bill and bond yields. As a result, the earnings multiple is approximately 13.5X, at the bottom end of the range in the past five years. Spire is a long-term buy, and investors are paid to wait.

Portfolio Insight

NorthWestern Energy

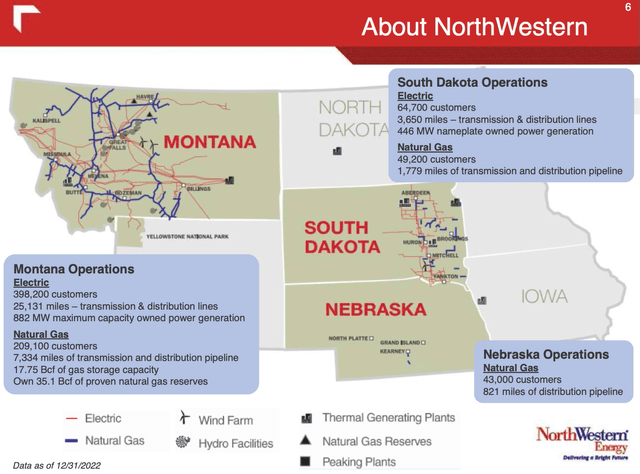

The third stock on our list is NorthWestern Energy (NWE), a regulated electricity and natural gas utility. The company serves 764,200 residential, commercial, and industrial customers in Montana, South Dakota, Nebraska, and Yellowstone National Park. NorthWestern obtains about 55% of its power from hydro, solar, and wind sources, with the remaining from coal and natural gas.

Total revenue was $1,477.8 million in 2022 and $1,505.4 million in the last twelve months.

NWE Investor Relations

NorthWestern mainly grows organically by adding customers and increasing the rate base. Montana, South Dakota, and Nebraska have low unemployment rates of 2.4%, 1.7%, and 2.3%, respectively, creating higher demand. Further, the state populations are increasing at a rate greater than the national average. As a result, revenue and EPS have climbed at ~3%+ annually. The growth rate may be better in the future because of base rate increases in Montana and South Dakota.

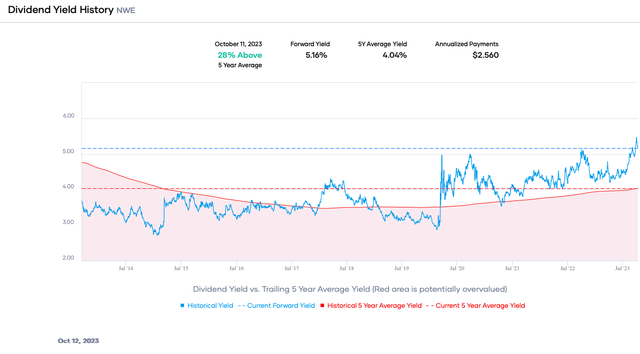

The utility is a consistent dividend grower with 19 years of increases, making it a Dividend Contender. The growth rate is about 5% annually. The declining share price has caused the forward dividend yield to spike to about 5.2%, the highest in a decade. The dividend safety is acceptable, with earnings and OCF payout ratios of ~79% and ~40%, respectively. In addition, the dividend quality grade is good at a ‘B+.’

NorthWestern Energy is undoubtedly undervalued based on a P/E ratio of ~14.5X, below the 5-year and 10-year ranges. Investors seeking income and dividend growth at a reasonable price can find it here.

Portfolio Insight

Read the full article here