By Kevin Flanagan

Halloween season is now upon us and if you look at recent price action within the U.S. Treasury (UST) market, it looks as if the spooks have started already.

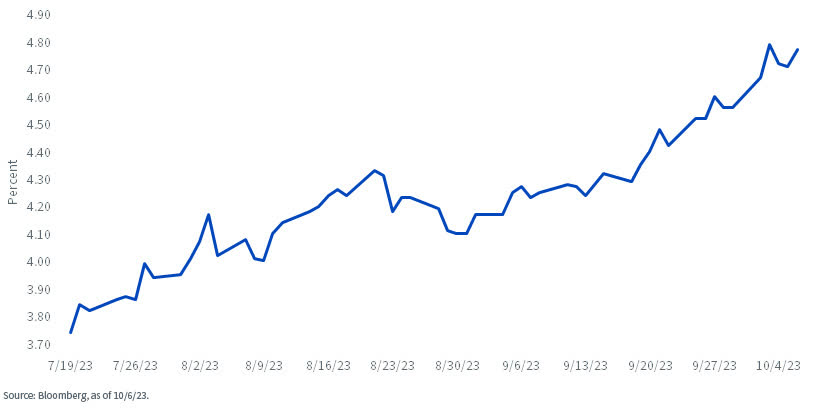

Indeed, the recent surge in the UST 10-Year yield to 4.80% caught many observers by surprise and has led to some commentary in which it appears as if investors are freaking out just a little bit.

Well, I’m here to try and allay some of those heightened anxieties and get to the root cause of why the 10-Year yield is at its highest level in 16 years – but doesn’t necessarily mean we are in a scary place for the bond market.

U.S. Treasury 10-Year Yield

I’ve discussed even before this latest increase in Treasury yields that what investors are witnessing is really more of a normal scenario for the U.S. bond market.

To be sure, the period between the global financial crisis and the end of the Covid pandemic was not truly representative of where the UST 10-Year yield should reside.

Factors such as the Federal Reserve’s zero interest rate policy, quantitative easing (QE) and negative rates abroad all helped to create a rate environment that was abnormal, in my opinion. So, what we are seeing now is what happens when the pendulum ultimately shifts back.

Really, the root cause of this most recent uptick in the 10-Year yield begins with the fundamentals. Yes, inflation has cooled off, but guess what – the U.S. economy has not.

That’s right, the recession that everyone was expecting to have reared its ugly ahead by now is actually an above 2.0% real GDP setting. In fact, the Atlanta Fed GDPNOW gauge is looking for Q3 growth to come in at 4.9%!

Behind this surprising performance has been a continued solid labor market landscape, which was just underscored by the September jobs report. To provide perspective, total nonfarm payrolls rose by a much stronger-than-expected 336,000, essentially double consensus forecasts.

Meanwhile, the unemployment rate remained at a historically low 3.8%. Looking ahead, weekly jobless claims (a leading economic indicator) also remained historically low, suggesting a visible weakening in the labor markets doesn’t seem to be imminent.

Obviously, a more restrictive Fed policy than expected (plus ongoing quantitative tightening) has combined with the resilient economy to give the bond market a one-two punch.

But what else is the Treasury market looking at? Certainly, burgeoning U.S. budget deficits have been gaining a lot of attention. I blogged on this very topic and opined how this factor is not necessarily a primary driver for rate action, but that it can be a secondary force.

In fact, one has to wonder if investors are finally waking up to the premise of baseline trillion-dollar deficits for the foreseeable future and what that means for the supply of Treasury securities that will be needed to fund these enormous shortfalls.

Finally, what about those foreign sovereign debt yields? Government bond yields throughout Europe are now no longer at or below zero, where countries such as the U.K. and Germany are witnessing their own 10-Year rates of over 4.50% and nearly 3%, respectively.

Now, you can even add Japan to the mix, with the 10-Year JGB yield at 0.80%. In other words, the UST 10-Year is not the only game in town anymore.

Conclusion

Back to my intro about bonds not being scary. The rise in U.S. bond yields is arguably a positive development from an investor’s perspective because it returns fixed income to its more traditional role in the asset allocation process. And, if you’re still uneasy, then I suggest utilizing the time-tested barbell strategy for your bond portfolio.

Kevin Flanagan, Head of Fixed Income Strategy

As part of WisdomTree’s Investment Strategy group, Kevin serves as Head of Fixed Income Strategy. In this role, he contributes to the asset allocation team, writes fixed income-related content and travels with the sales team, conducting client-facing meetings and providing expertise on WisdomTree’s existing and future bond ETFs. In addition, Kevin works closely with the fixed income team. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S in Finance from Fairfield University.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here