By Tajinder Dhillon

Earnings season kicks off this week, and we preview the S&P 500 2023 Q3 earnings season in granular detail, providing both aggregate and company-level insights using data from I/B/E/S, StarMine, and Datastream, which are all found in the desktop solution LSEG Workspace.

Earnings Commentary

The first half of the year has been far better than expected when comparing expectations at the start of the year which was a more doom and gloom narrative along with the possibility of an earnings recession. However, both Q1 and Q2 posted a stronger-than-expected quarter with an improvement in the final earnings growth rate while narrowly avoiding an earnings recession. It is likely that Q2 was the bottom in earnings as y/y growth is forecasted to be positive for the next eight quarters.

Full-year growth expectations for 2023 are currently 2.3%, the lowest since 2020 and below the long-term average of 7.8%. Q3 is also expected to be a small contributor to the full-year growth rate with a forecast y/y growth rate of 1.3%. Instead, the bulk of growth expectations are expected in Q4 with a growth rate of 10.8%.

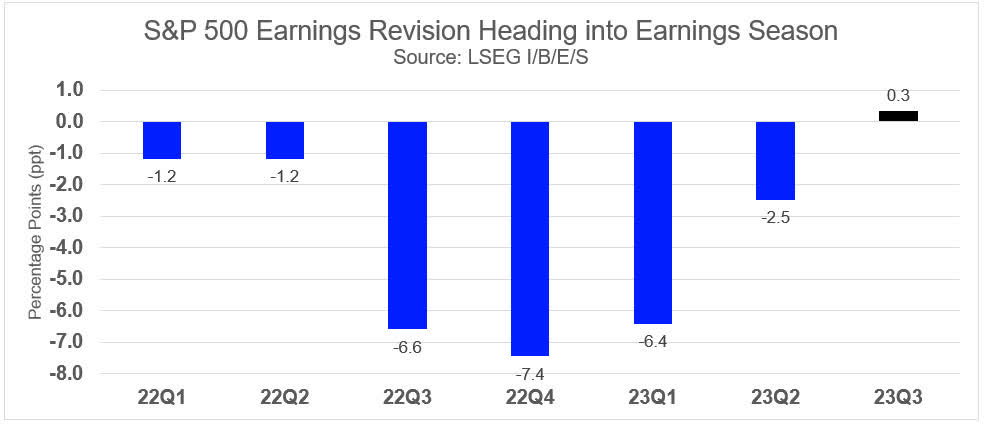

For the first time in six quarters, earnings growth expectations have risen heading into the quarter (Q3: +0.3 percentage points). The prior six quarters saw an average decline of 4.2 ppt heading into earnings season. This sets up another opportunity for Q3 to deliver a better-than-expected quarter if history repeats itself following a very strong earnings surprise rate in Q1 and Q2, which were the highest since 2021.

An interesting observation is that earnings growth expectations for Q4 and full-year 2024 have remained fairly stable since the beginning of the year considering a ‘higher for longer’ rate environment, a rise in oil prices, combined with domestic issues around labor renegotiations and student loan repayments.

An important trend to monitor is the revenue beat rate and surprise rate, both of which have been trending downward in recent quarters (to read more on this: S&P 500 2023 Q2 Earnings Review: Revenues Miss Analyst Expectations, August 15, 2023). These two factors can corroborate concerns around pricing power and its impact on net profit margins. Also, real revenue growth (adjusted for inflation) is expected to be negative for the third consecutive quarter.

Part 1 – Earnings Growth and Contribution

Using data from the October 6h publication of the S&P 500 Earnings Scorecard, Q3 blended earnings (combining estimates and actuals) are forecasted at $464.6 billion (+1.3% y/y, +2.8% q/q) while revenue is forecasted at $3,761.0 billion (+0.9% y/y, +1.4% q/q).

Ex-energy, earnings growth is forecasted at 6.2%, which marks the second consecutive quarter of positive ex-energy growth. Ex-energy, revenue growth is forecasted at 3.3%.

At a sector level, Industrials is expected to continue its streak of positive y/y earnings growth at eleven consecutive quarters, the longest of any sector. Consumer Discretionary, Consumer Staples, and Financials are all expected to see its third consecutive quarter of growth. Materials is expected to post a fifth consecutive quarter of earnings decline followed by Health Care and Real Estate at four consecutive quarters.

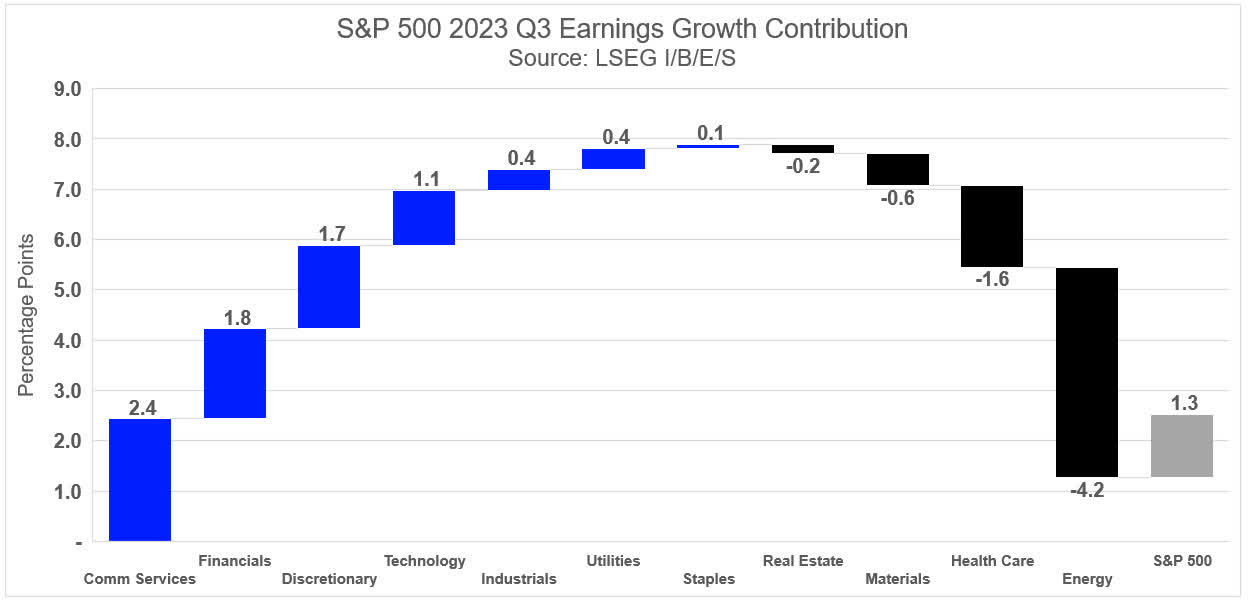

From an earnings growth contribution perspective, seven sectors have positive earnings contribution while four sectors have negative earnings contribution (Exhibit 1).

Communication Services has the largest growth contribution of any sector and is forecasted to contribute 2.4 percentage points (PPT) towards the index growth rate of 1.3%. Financials (1.8 ppt) and Consumer Discretionary (1.7 ppt) are the next largest contributors while Energy (-4.2 ppt), Health Care (-1.6 ppt), and Materials (-0.6 ppt) are the largest detractors to earnings growth this quarter.

We point out that Energy is no longer the ‘top dog’ from an earnings growth contribution perspective, which has been the trend in recent quarters. Instead, the sector now faces more difficult year-over-year comparisons going forward, given the banner year of 2022, where the sector recorded close to $200 billion in earnings. Therefore, looking at quarterly growth rates will be more effective to gauge earnings performance this year. Energy is forecasted to post Q3 aggregate earnings of $36.2 billion, which translates to a q/q growth rate of 18.7%.

Exhibit 1: S&P 500 23Q3 Earnings Growth Contribution

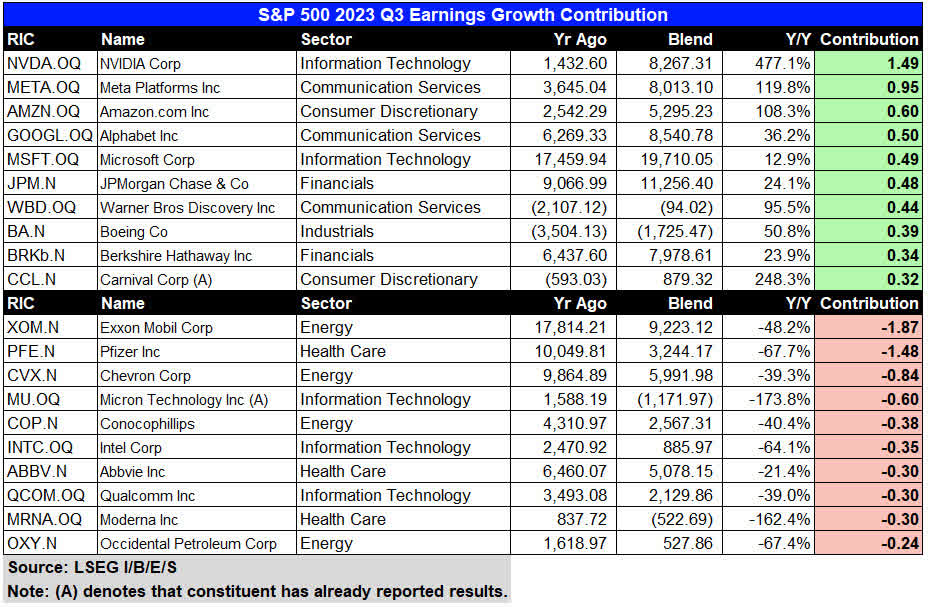

We also look at earnings growth contribution at a constituent level in Exhibit 1.1 and highlight the top 10 and bottom 10 contributors. Nvidia Corp (NVDA) is expected to deliver the lion share of earnings growth for Information Technology (1.5 ppt). The same can be said for Amazon.com Inc (AMZN) in Consumer Discretionary for the third consecutive quarter (0.6 ppt), and Meta Platforms (META) for Communication Services (1.0 ppt). In other words, the ‘Magnificent-7’ will yet again be a group to look at closely this quarter.

In the bottom half of the table, Energy dominates the top 10 as explained earlier. For the third consecutive quarter, many of the large pharmaceutical constituents are expected to post negative earnings growth from a strong 2022 when it benefitted from vaccine revenues. Interestingly, many semiconductors also appear in this group (Micron Technology (MU), Intel Corp (INTC), and Qualcomm Inc (QCOM)).

Exhibit 1.1: S&P 500 23Q3 Earnings Growth Contribution

Part 2 – Estimate Revisions into Earnings Season

Analysts have moderately raised earnings expectations heading into earnings season for the first time in six quarters. From a guidance perspective, we have seen 79 negative Q3 EPS pre-announcements compared to 41 positives, resulting in a negative/positive ratio (n/p) of 1.9, which is below the long-term average of 2.5 and in-line with the prior four-quarter average of 1.9. In Q2, we saw 62 negative pre-announcements compared to 39 positive heading into earnings season, yielding a 1.6 n/p ratio.

Over the last three months, the Q3 EPS estimate has improved modestly from $55.76 to $55.78 per share, resulting in analysts upgrading y/y growth expectations by 0.3 ppt heading into earnings season (Exhibit 2). Q3 growth expectations peaked in the week ending September 8th (+2.0%) and has since fallen. However, Q3 marks the first time growth expectations have increased heading into earnings season which may validate the idea that last quarter was the ‘bottom’ in earnings growth.

Exhibit 2: S&P 500 Earnings Revisions Heading into Earnings Season

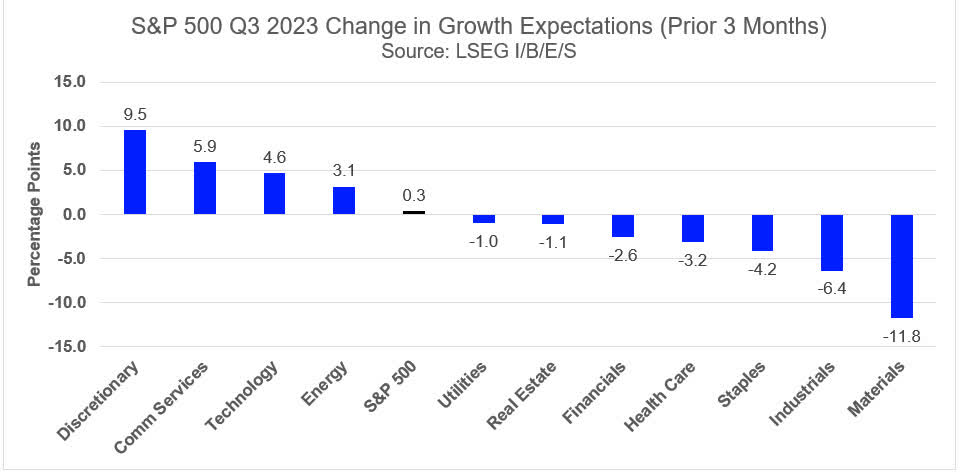

Exhibit 3 highlights earnings momentum at a sector level, defined as the rate of change in Q3 growth expectations over the last three months, expressed in percentage points. Consumer Discretionary has seen the strongest momentum heading into earnings season (+9.5 ppt) followed by Communication Services (+5.9), Technology (+4.6), and Energy (+3.1). Materials has seen the weakest momentum (-11.8) followed by Industrials (-6.4), and Consumer Staples (-4.2).

Over this same period, Communication Services has seen an upgrade in earnings growth expectations for the next five quarters (including Q3), followed by Energy (four quarters), and Information Technology/Consumer Discretionary (three quarters). Conversely, Materials, Industrials, Consumer Staples, and Real Estate have seen a downgrade in earnings growth expectations for the next four quarters (including Q3).

Exhibit 3: S&P 500 2023 Q3 Estimate Revisions

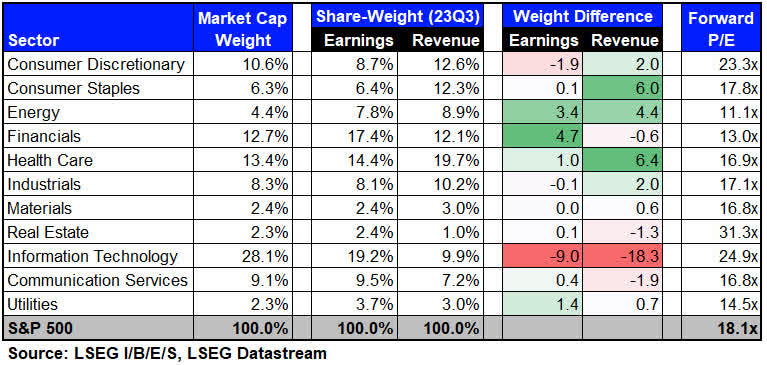

Part 3 – Market Cap vs. Earnings Weights

Exhibit 4 looks at the difference between ‘market-cap’ and ‘share-weighted’ weights for the S&P 500 sectors. The S&P 500 Earnings Scorecard utilizes a share-weighted methodology.

Information Technology has the largest earnings weight this quarter at 19.2% yet 1.5 times lower than its market-cap weight of 28.1%. This results in the largest weight differential of all sectors, highlighting the premium on the sector, which has a forward P/E of 24.9x (38% premium vs. S&P 500).

Financials saw a boost to its earnings weight in Q1 due to the GICS Classification change in March, which saw juggernauts Visa Inc (V) and Mastercard Inc (MA) move to this sector (previously resided in Information Technology). To read more about this, please look at our prior note on this subject: 2023 GICS Classification Change: Impact on S&P 500 Earnings, March 27, 2023. The sector has the largest positive earnings weight differential at 4.7% with a forward P/E of 13.0x.

While Energy’s positive weight differential has declined compared to prior quarters, the sector continues to overdeliver on earnings relative to its market cap weight (which has doubled since September 2021) and trades at the cheapest valuation of any sector at 11.1x.

The ‘Magnificent-7’ group comprising of Apple Inc (AAPL), Amazon.com Inc, Alphabet Inc (GOOG,GOOGL), Meta Platforms Inc, Microsoft Corp (MSFT), NVIDIA Corp, and Tesla Inc (TSLA) has a market cap weight of 29.9% (an all-time high) compared to an earnings and revenue weight of 15.6% and 9.7% respectively. The ‘Magnificent-7’ group has an aggregate forward P/E of 27.6x, a 55% premium to the overall index. The premium has declined materially since last quarter and when excluding the ‘Mag-7’, the forward P/E declines to 15.6x.

Exhibit 4: Market Cap vs. Share-Weight for S&P 500 Sectors

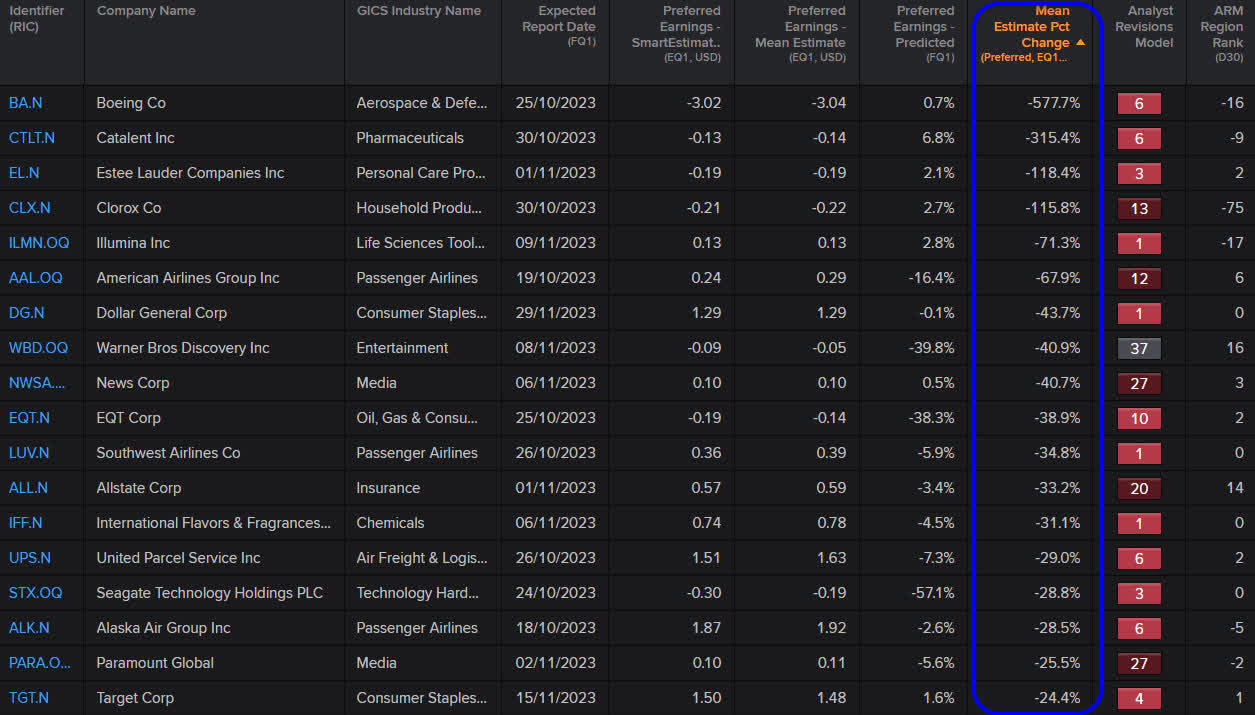

Part 4 – Which companies have seen the largest revisions heading into earnings season?

Using the Screener app in LSEG Workspace, we can screen for yet-to-report constituents that have seen the largest upgrades and downgrades heading into earnings season.

Exhibit 5 highlights companies who have seen earnings downgrades as defined by the 60-day mean estimate change in ‘EQ1 Preferred Earnings’. Preferred Earnings is defined as EPS for most companies except for Real Estate where it can be either EPS or FFOPS depending on analyst coverage.

Boeing Co (BA) has seen the largest downgrade in EPS estimates over the last 60 days (-577.7%) followed by Catalent Inc (CTLT) (-315.4%), Estee Lauder Companies Inc (EL) (-118.4%), Clorox Co (CLX) (-115.8%), and Illumina Inc (ILMN) (-71.3%). Note: values less than -100% occur when an EPS estimate turns from positive to negative.

Exhibit 5: Largest Negative Revisions for 2023 Q3

LSEG Workspace

Exhibit 5 also displays the Predicted Surprise (PS) for each constituent, which compares the SmartEstimate vs. Mean Estimate. A PS greater than 2% or less than -2% is deemed significant as our research shows that StarMine will accurately predict the direction of the earnings surprise 70% of the time.

The StarMine SmartEstimate is a quantitative analytic which is used as an input to many of the StarMine models. The SmartEstimate places a greater weight on higher ranked analysts who are more accurate and timelier.

We see a positive correlation between constituents who have seen a large downgrade and a corresponding negative PS. Furthermore, a positive correlation is shown between the mean estimate change vs. Analyst Revision Model (ARM) score (i.e., companies that have seen large downward earnings revision also have a low ARM score).

ARM is a percentile stock ranking model that is designed to predict future changes in analyst sentiment by looking at changes in estimates across EPS, EBITDA, Revenue, and Recommendations over multiple time periods. The last two columns display both the current ARM score and its 30-day change.

Looking at the Predicted Surprise and ARM columns can be very useful during earnings season to assess the likelihood of whether companies are expected to beat or miss earnings while at the same time gauging analyst sentiment.

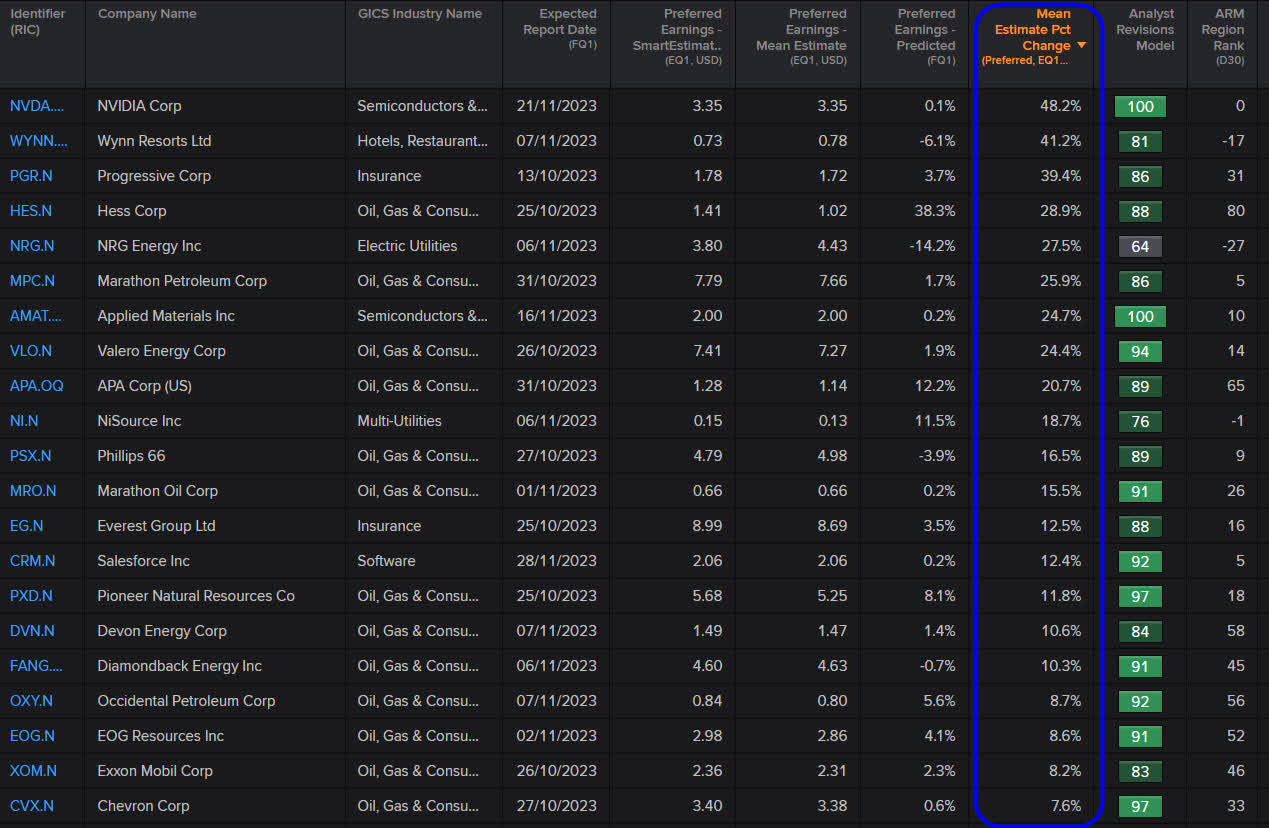

Exhibit 5.1 displays the same data for constituents with the largest upgrades heading into earnings season.

Exhibit 5.1: Largest Positive Revisions for 2023 Q3

LSEG Workspace

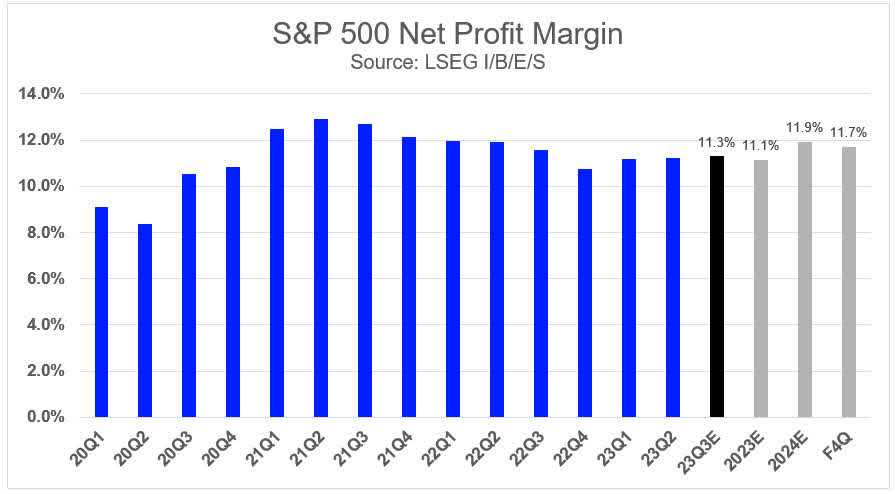

Part 5 – Net Profit Margin Expectations

Using data from the S&P 500 Earnings Scorecard, we look at quarterly net profit margins (Exhibit 6). Net profit margins peaked in 2021 Q2 (12.9%) and which then declined for six consecutive quarters and has since risen for three consecutive quarters.

The Q3 blended net profit margin is 11.3%, a slight improvement from the prior quarter. We note that Q3 margin expectations have remained steady over the last three months.

Over the last three months, seven sectors have seen its net margin estimate decline, while four sectors have seen an increase. Industrials has seen the largest decline in Q3 margin expectations (-71 bps, current value: 9.5%), followed by Materials (-57 bps, 9.5%), and Health Care (-53 bps, 8.8%). Information Technology has seen the largest improvement in margin expectations (122 bps, 23.3%).

The 2023 and 2024 full-year estimate is currently 11.1% and 11.9% respectively, while the forward four-quarter estimate is 11.7%.

Exhibit 6: S&P 500 Net Margin Expectations

Part 6 – Forward P/E & PEG Ratio

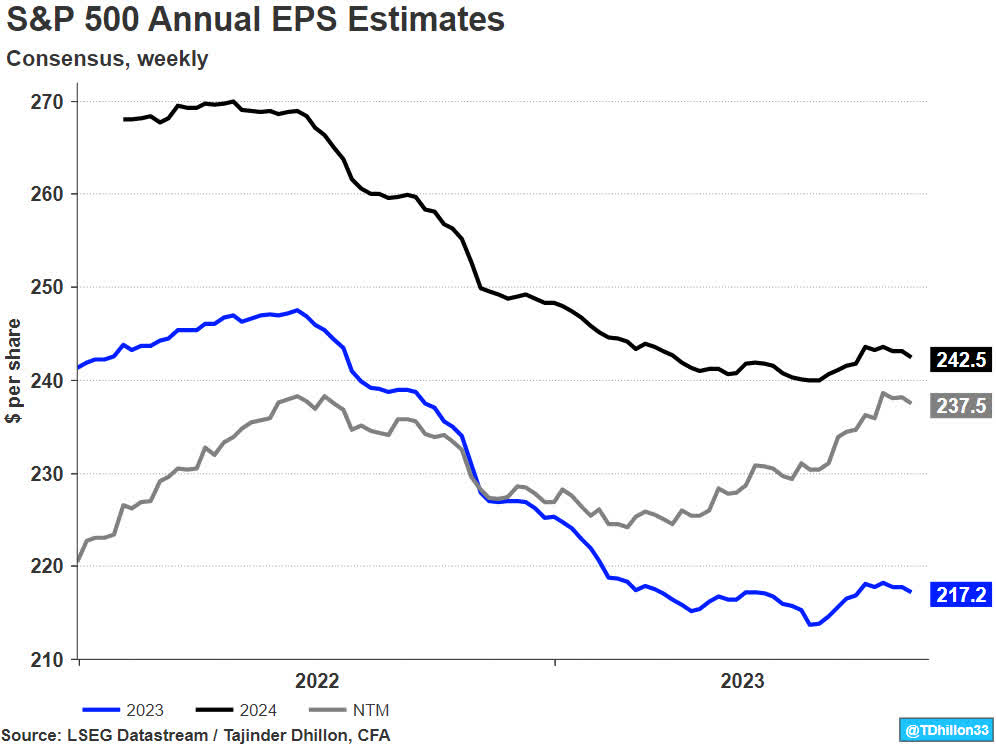

Using LSEG Datastream, the forward 12-month (F12) EPS recently peaked to $238.57 per share last month and currently sits at $237.46 per share (Exhibit 7). However, this can be misleading as it is important to note that the F12 EPS estimate continues to have a larger weighting towards the 2024 estimate as each day passes this year.

For a more accurate picture, the 2023 and 2024 estimates have declined by 11.7% and 9.2% respectively since June 2022. In comparison, the S&P 500 has risen by approximately 14% over the same period.

The S&P 500 forward 12-month P/E ratio has fallen over the last three months to a current reading of 18.1x, which ranks in the 79th percentile (since 1985) and a 2.3% premium to its 10-year average (17.7x). For reference, the trough forward P/E during the last four recessions were as followed: 10.1x (Oct 1990), 17.3x (Sept 2001), 8.9x (Nov 2008), and 13.0x (March 2020).

Furthermore, the S&P 500 ‘PEG’ ratio is currently 1.33x, which ranks in the 67th percentile (since 1985) and a 5.7% discount to its 10-year average (1.41x). The PEG ratio has fallen significantly compared to the previous quarter when it was in the 98th percentile.

Exhibit 7: S&P 500 EPS Estimates

Conclusion

Q3 estimates have improved ever so slightly heading into earnings season, which may set a lower bar for corporations to beat analyst expectations and surprise to the upside, as seen in Q1 and Q2.

If Q3 delivers a weaker-than-expected earnings season, we would expect a material downgrade in Q4 estimates as it is the high watermark quarter for 2023.

We continue to monitor top-line strength and see if Q3 can show any improvement in the revenue surprise rate, which reached a multi-year low last quarter.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here