Vulcan Materials Company (NYSE:VMC) is a company operating in the building materials industry. It is actually one of the largest companies operating in that industry at least by market capitalization. They have a simple and predictable business but they do it at scale. The company has great cash flow generation with $1.6B in adjusted EBITDA in 2022. They have the main aggregates segment and have recently been achieving margin expansion and increased profits from their asphalt and concrete businesses. The company does seem overvalued compared to its peers but maybe its size and strength of operations make it worth paying for.

Introduction

Vulcan Materials Company, together with its subsidiaries, produces and supplies construction aggregates primarily in the United States. It operates through four segments: Aggregates, Asphalt, Concrete, and Calcium. The Aggregates segment provides crushed stones, sand and gravel, sand, and other aggregates; and related products and services that are applied in construction and maintenance of highways, streets, and other public works, as well as in the construction of housing and commercial, industrial, and other nonresidential facilities. The Asphalt Mix segment offers asphalt mix in Alabama, Arizona, California, New Mexico, Tennessee, and Texas, as well as engaging in the asphalt construction paving activity in Alabama, Tennessee, and Texas. The Concrete segment provides ready-mixed concrete in California, Maryland, New Jersey, New York, Oklahoma, Pennsylvania, Texas and Virginia, and Washington D.C. The Calcium segment mines, produces, and sells calcium products for the animal feed, plastics, and water treatment industries. The company was formerly known as Virginia Holdco, Inc. and changed its name to Vulcan Materials Company. Vulcan Materials Company was founded in 1909 and is headquartered in Birmingham, Alabama.

Numbers/Outlook

In 2022 Vulcan Materials Company had full year results of $7.3B in revenues and net income of $575.6M which comes out to $5.04 in EPS diluted. The company has also reported the first 2 quarters of 2023 in which they had $3.76B in revenues, with $429M in net income which equates to $3.25 in EPS diluted. The company also currently pays a dividend of $1.72 per share, which is a 0.81% yield at the current share price.

The outlook for the company’s growth continues to look good. The company had some updates for their full year outlook in their 2nd quarter earnings results. The company is forecasting increased 2023 full year net income between $855M and $935M and adjusted EBITDA between $1.9B and $2B. The company sees a good market for their products related to infrastructure as well as residential and non-residential construction. They have seen a sharp increase in infrastructure projects with funding made available in the 2023 Omnibus Appropriations Act as well as the Infrastructure Investment and Jobs Act. In regards to residential and non-residential construction they estimate that 75% of the population growth and 74% of household formations over the next decade will occur in Vulcan-served states. These all show good signs of future demand and need for the products Vulcan provides.

The reported numbers for the company look great for the first half of 2023. Especially the net income which is only $150M off from the full year net income from all of 2022. If they continue to execute well and have a 2nd half of the year that was as good as the 1st half they would meet their forecast which would be an incredible achievement for the company.

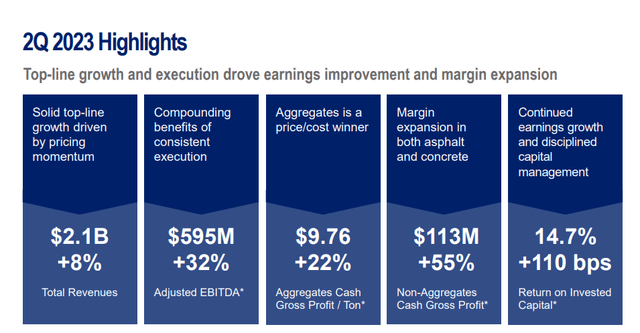

Vulcan Materials Company Investor Presentation 2023 (Vulcan Materials Company)

Potential Risks

There are also potential risk factors to consider. One risk factor is that the business is dependent on the timing and amount of federal, state and local funding for their infrastructure projects. This can cause the company to go through periods of time when the money available for these projects dries up and they have to wait for funding to be approved if at all. Currently there are many infrastructure Acts passed with federal and state funding but in the future this might not be the case.

Another potential risk factor for the company is that they are in certain markets experiencing the expanded use of aggregate substitutes. Recycled concrete and asphalt are increasingly being used in some of their markets and expanded use of these could result in reduction in demand for aggregates.

All of these risks are possible and there are many other risks out there as well. They just need to be monitored to see if they will have an effect on the company and by extension your investment.

Valuation

Vulcan Materials Company has a current market capitalization of $28B and a price to earnings (P/E) ratio of 38.23. This P/E ratio is at the higher end of competitors that I have seen. As such they are trading at a premium to their peers but that may be warranted if they have superior operations and scale. Of the other building materials companies that I looked at this company does have the largest market capitalization but all these companies don’t exactly have the same businesses just some of the same segments. They are usually operating in some different parts of the same industry.

Some of the companies that operate in the same industry as Vulcan Materials are Martin Marietta Materials Inc (MLM) with a P/E of 27.69, Summit Materials Inc (SUM) with a P/E of 22.88, and Eagle Materials Inc (EXP) with a P/E of 12.81. All of these companies compete in one or more of Vulcan Materials segments but they all trade at a lower price to earnings multiple than the company. It seems like from a valuation standpoint, it would be a better investment if it had a P/E multiple that was closer to its peers. The company can reach this result 2 different ways, either the stock price could drop and bring it more in line with the other companies or the earnings could increase like the company is indicating could happen throughout the rest of 2023 and it could make the stock more attractive.

The company currently has a total debt load of $4.5B with maturities ranging from 2023 to 2048. The company has a long-term target range of EBITDA to debt of 2.0x to 2.5x and the company currently sits at 2.1x. So they have in the range that they want to be in and do not show any issues with keeping up with the debt payments and maturities with their robust cash flow generation.

Investor Takeaway/Conclusion

Vulcan Materials Company looks like a great business. The company has robust operations and many segments that continue to grow as the business expands its geographic footprint into key markets in the U.S. This is a steady money making machine of a company and they are consistently growing and the share price has followed. It seems like right now the share price of the company may have gotten ahead of itself. I think that the best time to invest in this may be when it has experienced some pullbacks in the stock price, or an increase in their earnings per share and when the multiples are more in line with the rest of the industry. If the company produces results that are the high end of their forecast the rest of the year, they could get to a P/E of around 29.8 if their stock price stayed at $211. When the company gets to a valuation metric that is on par with the rest of the industry, it would be a buy.