By Padhraic Garvey, CFA, Regional Head of Research, Americas and Benjamin Schroeder, Senior Rates Strategist

US yields are off their highs, and we doubt the mood is there to move higher immediately. Inflation data to decide

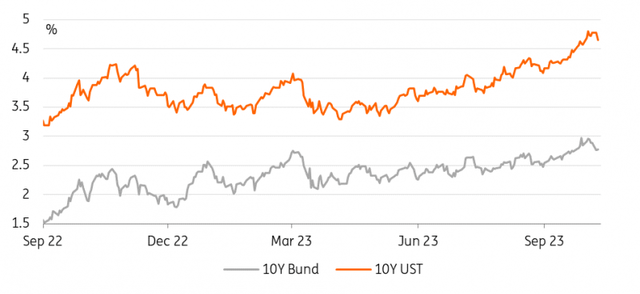

The US 2-year is now back to levels first seen in June this year when the funds rate was 25bp lower. The 10-year is off its recent highs, but still practically 80bp above where it was in June. The curve has clearly steepened over this period.

Things have changed since the weekend though. The bear market bubble has burst in the 10-year, and the market has downsized the rate hike risk ahead. Inflation readings in the next couple of days will have a say, with month-on-month readings still coming in a tad hot on the CPI. That’s the most likely impulse for resumed upside to yields.

Interesting that the 3-year auction tailed yesterday. There was a strong market at the time, which can help to tame negatives from this. But at the same time, the indirect bid (which includes central banks) was remarkably subdued, which is indicative of relatively weak end-investor demand.

All eyes clearly remain on the tragic scenes out of Israel, and there is deep concern over what’s to come. Likely this story goes quiet for a while, but it’s clearly far from over. More likely the beginning, in fact, given the voices out of Israel.

Even if it remains localised, there will be concern that it becomes much bigger and more dangerous. That will remain a rationale for core bond yields not straying too much higher from here. They are currently well off recent highs (more so in the US), and the mood for attaching 5% has waned.

There is a 4.5% risk ahead for the 10-year, unless the inflation data is high enough to cause a reversal higher in yields.

The Bond Bear Market Bubble Has Burst (Refinitiv, ING)

Today’s events and market view

Even though the flight-to-quality move has abated, the US CPI data ahead might still be reason enough for some to stay on the sidelines. We will already get the US PPI data today and, in the evening, the minutes of the last Federal Reserve meeting, where rates were kept on hold but projections were significantly raised. We can also expect a number of comments from central bankers coming out of the IMF/Worldbank meetings in Marrakech. The main focus in the eurozone with an otherwise empty calendar will be the European Central Bank consumer expectations survey on inflation.

In government bond primary markets, Germany is active with 30-year taps, and later, the US Treasury will tap its 10-year note.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more.

Original Post

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here