Southwestern Energy (NYSE:SWN) is a primarily natural gas exploration and production company headquartered in Houston, Texas. The company currently trades with a market cap of $7 Billion.

The company was started all the way back in July 1929, just as the Great Depression was about to get underway. Over the years, the company plodded along eventually becoming a public company in 1981. Southwestern Energy is perhaps most famous for its discovery of the Fayetteville Shale in July 2004. This catapulted the company’s growth at the same time that natural gas prices also saw a substantial rise.

Unfortunately for Southwestern Energy, horizontal drilling in gas-shale unleashed an overabundance of gas and as the natural gas prices slowly decreased over the next decade heading into 2020 and 2021, the company sold its Fayetteville Shale position in 2018.

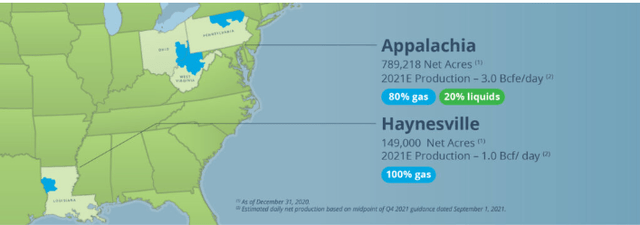

Today, the company holds positions in the regions shown below in the Appalachia regions as well as the Haynesville Shale in western Louisiana. Despite only being a natural gas focused company, their strategic advantage is that their natural gas positions are in close proximity to end markets.

Southwestern Areas of Operation (Southwestern Energy Website)

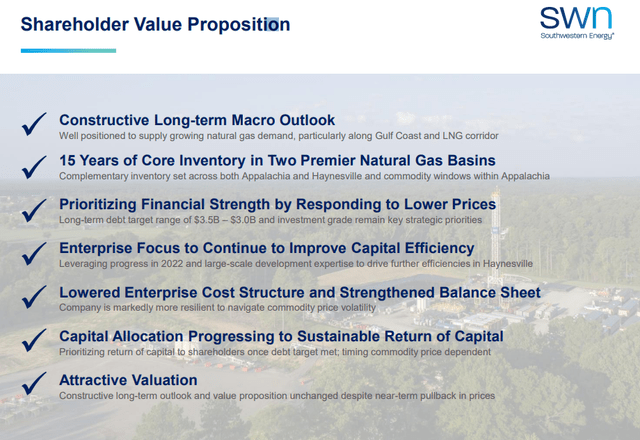

Southwestern Energy created this slide to share what they believe are the reasons they are on the right path as a company. We will evaluate some of these points below.

Southwestern Energy Shareholder Value Proposition (Southwestern Energy Q2 Presentation)

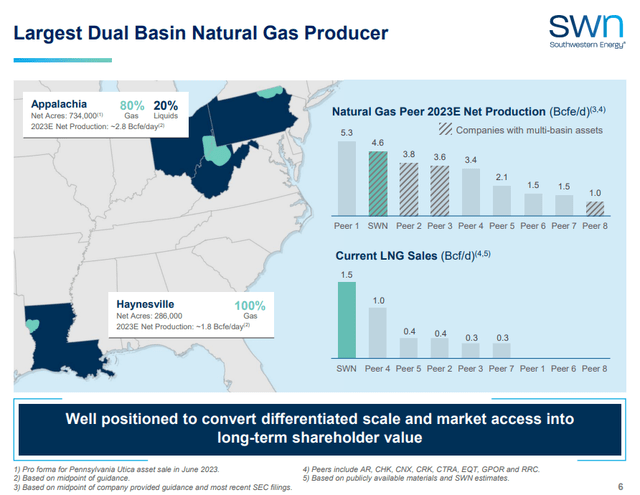

Southwestern Energy has positioned itself as one of the premier natural gas producers, making that their sole focus. Their acreage is in the heart of the Haynesville Shale and the Appalachia Shales such as the Marcellus Shale. I’ve written about natural gas before and I believe demand for natural gas is poised to continue to grow.

Natural Gas Producer Comparisons (Southwestern Energy Q2)

Cash Flow

The company’s cash flow was on a difficult trajectory headed into 2020. After rearranging their balance sheet and receiving a decent increase in realized natural gas prices, their cash flows appear to be more sustainable.

| $ millions | 2019 | 2020 | 2021 | 2022 | TTM 2022 |

| Operating Cash Flow | 964 | 528 | 1,363 | 3,154 | 3,317 |

| CapEx | (1,099) | (896) | (1,032) | (2,115) | (2,351) |

| Free Cash Flow | (135) | (368) | 331 | 1,039 | 966 |

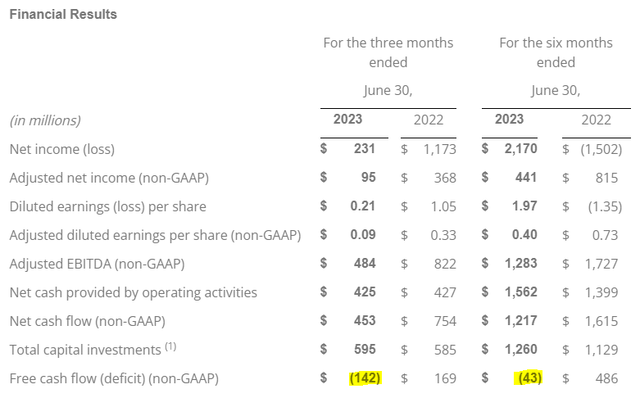

The above table is from the Seeking Alpha financial data and the TTM data doesn’t accurately represent the current situation. Currently, the company is once again outspending their operating cash flow and for both the previous three months as well as six months, the company has had negative free cash flow. I expect this will only be temporary, but still, old habits die hard.

Financial Results Q2 2023 (Southwestern Energy)

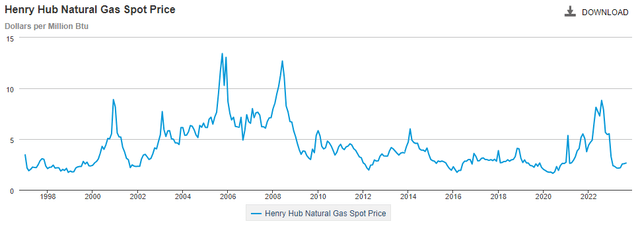

Natural Gas Prices

The bump in operating cash flows in 2022 came as natural gas prices skyrocketed. However, in the immediate next section, you will see that thanks to their hedging program, Southwestern Energy did not get to fully realize those prices.

Henry Hub Natural Gas Prices (EIA)

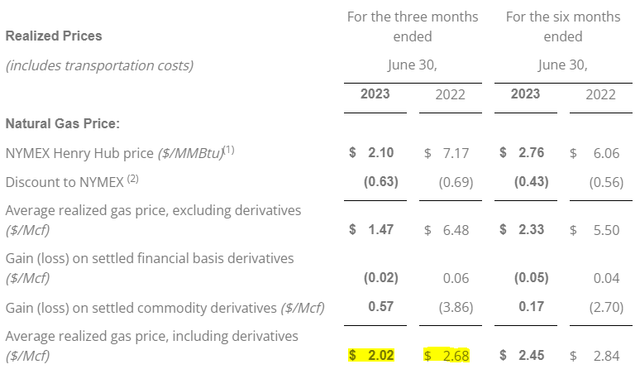

Realized Natural Gas Prices

It is important to understand that even though natural gas prices increase dramatically, unless they stay there for a sustained period of time, a company like Southwestern Energy will not get to realize those prices. That is because the company has a hedging program which protects them on the downside but also limits their upside. The company realized prices in June 2022 of $2.68 and had to forfeit $3.86 per Mcf thanks to their “commodity derivatives” contracts.

In the most recent quarter, they were able to reap the benefits of hedging by gaining just over 50 cents per Mcf. However, this still only brought the realized price per Mcf up to $2.02.

Considering that Southwestern Energy is once again outspending their cash flow it demonstrates that natural gas prices in this range are not attractively sustainable for Southwestern Energy. Today, Henry Hub natural gas prices have risen over the last month and are trading at $3.40 cents and so this should present a sustainable price for Southwestern Energy to make money.

Realized Natural Gas Prices Q2 2023 (Southwestern Energy)

Derivatives Hedging

According to the most recent 10Q, The company currently has most of its production hedged through 2024. After 2024, the company will be able to realize substantially higher natural gas prices…assuming natural gas prices remain elevated. I expect that they will.

Balance Sheet

In 2020, the company’s balance sheet was dangerously close to upside down when they took actions to reverse course. Ultimately, the company was forced to dilute shares to stay solvent during the pandemic. See the next section where I show the increase in shares outstanding.

| $ millions | 2019 | 2020 | 2021 | 2022 | Q2 2022 |

| Assets | 6,717 | 5,160 | 11,848 | 12,926 | 13,001 |

| Debt | 3,471 | 4,663 | 9,301 | 8,602 | 6,512 |

| Debt-to-Assets | .52 | .90 | .79 | .67 | .50 |

The company’s balance sheet is on a better path today. Natural gas prices have rebounded from the pandemic and seem to be on a path where companies like Southwestern can make money. Nevertheless, hopefully the company has learned its lesson and proceeds to manage its balance sheet more responsibly going forward.

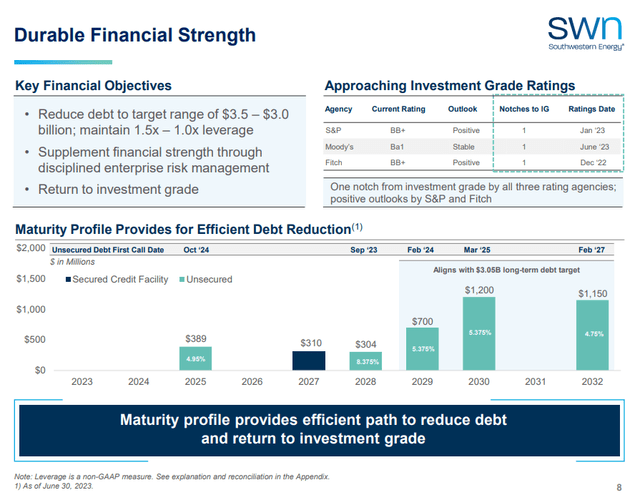

This slide below shows their debt maturity profile. The company has a very manageable debt load until 2029 and 2030. If the company manages its finances well, then the debt coming in 2029 and 2030 and beyond shouldn’t be a problem in my humble estimation.

Each of the senior note issuances have a fixed interest rate that can be seen inside each bar in white font.

Long-Term Debt Structure (Southwestern Energy)

Shares Outstanding

This demonstrates the risk of dilution if the company isn’t able to make enough money to manage its balance sheet well. The company had roughly 350 million shares outstanding in 2013 and so the company has a history of using share dilution to dig itself out of a hole.

| Millions | 2019 | 2020 | 2021 | 2022 | Q2 2022 |

| Shares Outstanding | 540 | 674 | 1,114 | 1,100 | 1,101 |

Comparison to Permian Resources

Here I want to do a comparison. I often mention that investing is a matter of choosing between various options. And when we place our bets, we should want to pick the “fastest horse in the race.” In my last article, I wrote an article about Permian Resources (PR) and as one would expect from its name, Permian Resources is only focused in the Permian Basin. The wells that are drilled in the Permian Basin are made up of a mix of oil and natural gas with most of them containing around 50 percent oil according to Permian Resources.

Many investors may not understand the difference between oil and natural gas and why it matters where you invest. If you don’t understand the difference, then you will be prone to make a mistake. Although these two are both hydrocarbons, they are not the same.

Both can be measured by the amount of energy that is contained within their molecular structure. Oil is a denser molecule than natural gas, therefore, as a general rule of thumb 6 mcf of natural gas equals the energy contained in one barrel of oil. Six mcf is a much larger volume of hydrocarbons, however it contains the same amount of energy contained within a barrel of oil. Now, monetarily speaking one Mcf of natural gas currently sells for roughly $3.40 cents while a barrel of oil sells for $86 per barrel. One can easily see the differential between these two hydrocarbons. Six mcf equals ($3.40 x 6) $20.40 and so this presents the extreme price differential between 6 mcf of natural gas and 1 barrel of oil. This makes companies that are leveraged to oil more attractive investments.

Now that I’ve explained that, let’s look at some hard numbers from Permian Resources to see how they compare to Southwestern Energy. I think the implications of the price differential between oil and natural gas will become more evident by comparing each company’s financial performance.

Permian Resources Cash Flows

Notice how Permian Resources is ramping up its capital expenditure due to the fact that they continue to receive strong returns from their previous capex. Therefore, free cash flow isn’t hurt by the increased CapEx.

| $ millions | 2018 | 2019 | 2020 | 2021 | 2022 | TTM 2023 |

| Operating Cash Flow | 670 | 564 | 171 | 526 | 1,372 | 1,803 |

| CapEx | (1,217) | (968) | (328) | (327) | (784) | (1,378) |

| Free Cash Flow | (547) | (404) | (157) | 199 | 588 | 425 |

Permian Resources Balance Sheet

A strong balance sheet goes hand-in-hand with profitable capital expenditures and the operating cash flow that result.

| $ millions | 2018 | 2019 | 2020 | 2021 | 2022 | Q2 2023 |

| Assets | 4,260 | 4,688 | 3,827 | 3,805 | 8,493 | 8,926 |

| Debt | 1,016 | 1,418 | 1,223 | 1,054 | 2,836 | 3,000 |

| Debt-to-Asset Ratio | .24 | .30 | .32 | .27 | .33 | .34 |

Permian Resources Shares Outstanding

Permian Resources has also diluted shares, but much more mildly than Southwestern Energy. And in fact, they are about to dilute share much further with an all-stock transaction to purchase Earthstone Energy (ESTE). The difference, in my opinion, is that these shares dilutions are accretive to shareholders, whereas Southwestern Energy is diluting shares to remain solvent.

| millions | 2018 | 2019 | 2020 | 2021 | 2022 | Q2 2023 |

| Shares Outstanding | 267 | 277 | 277 | 310 | 323 | 335 |

Conclusion

I am rating Southwestern Energy a sell. I’m actually bullish on natural gas over the long term. Over a long enough time horizon, natural gas prices are going to rise as there is simply too large of a price differential between natural gas and oil. The market has a way of slowly fixing these things. That differential will be squeezed over time as natural gas markets continue to become more mature. And although there are some who might find this prediction strange, I believe Bitcoin will be a big driver of closing the gap between oil and natural gas. I wrote about this possibility in an analysis of Microstrategy (MSTR). Despite this fact, I still cannot recommend buying Southwestern Energy. Why is that?

First, the company doesn’t have a proven track record of managing itself well. Granted, they faced an uphill battle with depressed natural gas prices through 2020, but when a company dilutes shareholders to the extent that they did, just to remain solvent, I cannot recommend that investors consider allocating capital there.

Second, the management team is basically the same as it was then. The CEO has been the CEO since 2016 when he graduated to the position from COO.

Third, even if you believe natural gas prices will increase, I do not believe it is prudent for investors to bet on natural gas prices increasing by investing in a purely natural gas company. Most companies that are focused on oil-shale, are also receiving a substantial amount of natural gas from each well. So if oil is providing the strongest returns at the moment, why not invest there, and when natural gas prices rise, you’ll also reap the benefits of higher natural gas prices.

Now, I will say that the upside for natural gas is higher than oil. For example, it’s not out of the realm of possibilities for natural gas to 3x over the next 5 years. If that does happen, Southwestern Energy will likely outperform companies that are focused solely on oil-shale. This is the nature of being more leveraged to a more volatile asset such as natural gas. But again, as a financial minded investor who tries to consider the risks between companies and their strategies, oil-shale companies represent a better risk-adjusted opportunity. For that reason, relative to oil-focused shale companies, Southwestern Energy is a sell.

Read the full article here