Written by Nick Ackerman, co-produced by Stanford Chemist.

Equities have been under pressure, and so have closed-end fund (“CEF”) discounts. The last time we covered Voya Global Advantage and Premium Opportunity Fund (NYSE:IGA), it was trading at a deep discount, and that’s where it remains today, which still makes it a tempting offering in this uncertain market.

The fund is tilted towards a value-oriented approach utilizing a call-writing strategy against indexes and exchange-traded funds (“ETFs”) while also including some global exposure. By writing calls, the fund adds some slight defense to its already defensive-tilted portfolio. That’s what helped the fund hold up significantly better in 2022.

However, through 2023, these defensive sectors haven’t been receiving quite the same love as the Magnificent Seven. Those stocks, on their own, have been driving all the gains this year, with most other stocks flat or down for the year. Even those names have been slipping lately as volatility slowly creeps back into the market, with interest rates rising significantly.

The Basics

1-Year Z-score: -1.51

Discount: -15.84%

Distribution Yield: 9.89%

Expense Ratio: 0.99%

Leverage: N/A

Managed Assets: $150.9 million

Structure: Perpetual.

IGA’s investment objective is “a high level of income; capital appreciation is secondary.” They intend to write “call options on indexes or ETFs, on an amount equal to approximately 50-100% of the value of the Fund’s common stock holdings.”

Performance – Discount Remains Attractive

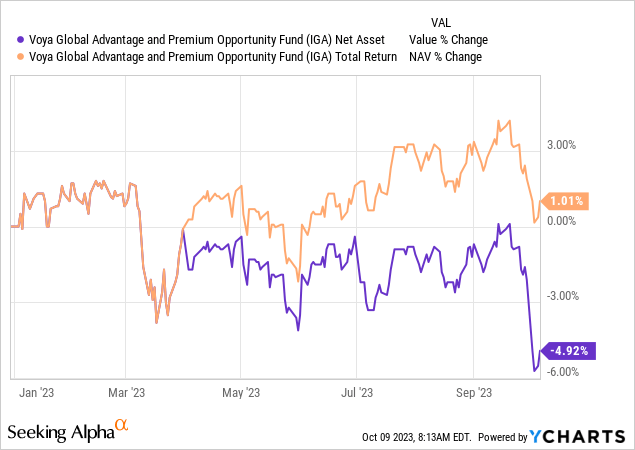

Since our last update, IGA has ever-so-slightly outperformed the broader S&P 500 Index (SP500) on a total return basis.

IGA Performance Since Prior Update (Seeking Alpha)

The fund last reported being overwritten by around 70.4%. That’s a fairly meaningful increase from being overwritten at around just under 50% previously. This suggests that the fund managers were or are getting more defensive, as it suggests the managers don’t expect the equity market to rise too substantially.

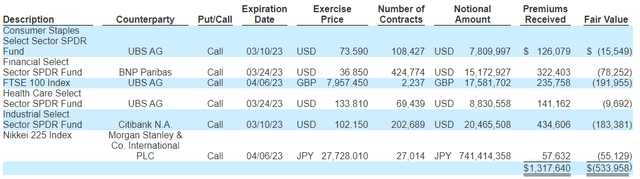

The fund writes calls against indexes and ETFs primarily, which means they aren’t making individual bets really but brushing with broad strokes. For example, here are what outstanding options they had at the end of their last fiscal year.

IGA Short Options Contracts (Voya)

Writing index calls means these transactions are cash-settled, or essentially, they are writing naked calls. The fund also doesn’t directly hold these ETFs usually that they’ve written against. That means, in theory, there is a chance for unlimited losses. That being said, in practice, their underlying portfolio also holds many of the same components and indirectly is “covering” these contracts.

The fund has a relatively low expense ratio for CEFs, and that’s fairly common for funds that don’t operate with leverage in the form of borrowings. Having no borrowings in this environment of rising interest rates, I would say, is another bonus for this fund as it is one less headwind they are having to deal with. It comes with its own downsides as well; if equity markets really take off, their leveraged peers stand to perform better – especially considering the call-writing strategy can put a ceiling on the amount of gains that could be realized. That’s why a flat to even slightly down market can work quite well for a call-writing fund such as IGA.

While global equities have underperformed their U.S. counterparts through most of the last decade, that also led to a drag on the performance of IGA. However, there are some signs that have reversed as international equities start performing better. Additionally, international markets remain relatively cheaper than the U.S. markets, which is another potential catalyst for better performance going forward. Of course, no one can predict the future, and IGA is even split between a heavy weighting to U.S. exposure and everything else.

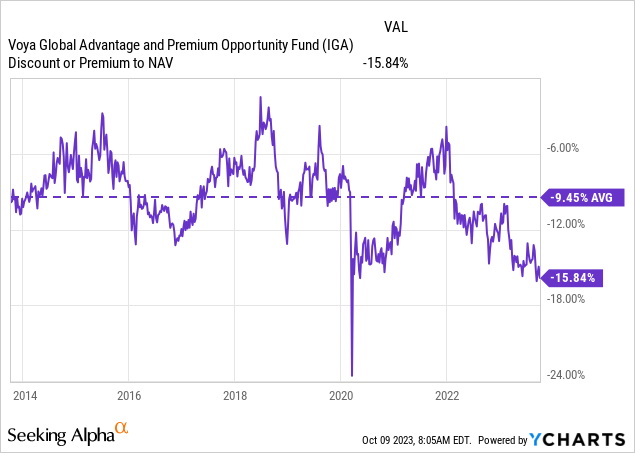

The fund’s discount has remained about the same since we last covered this fund, which makes it still an attractive discount to consider for initiating a position.

YCharts

Distribution Yield Near ~10%

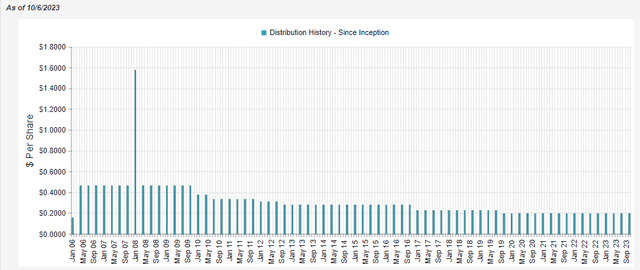

The fund pays quarterly, and that is less appealing to some investors.

IGA Distribution History (CEFConnect)

Distribution reductions are also less appealing to investors but have been fairly consistent with the relatively weaker performance of the fund with its global tilt. At this time, the fund’s deep discount has pushed up the distribution yield to nearly 10%, but the fund’s NAV distribution rate is at a more sustainable level of around 8.3%.

As a call-writing equity fund, it will heavily rely on capital gains to fund its distribution, as we discussed in our prior update.

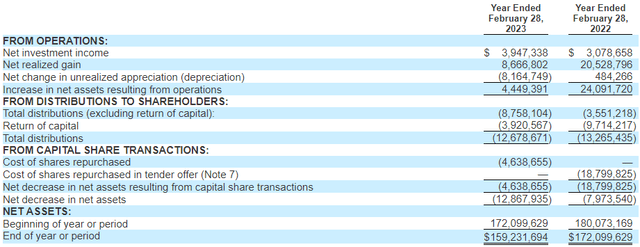

As with most equity funds, we can see that net investment income isn’t enough to cover their payout to shareholders. However, NII did increase in the last year.

IGA Annual Report (Voya)

Any increase in NII is welcomed as it means less pressure on what the fund will need for capital gains. On a per-share basis, this went from $0.18 in fiscal 2022 to $0.25 in fiscal 2023.

Putting together the NII and realized capital gains that put the fund just shy of covering its payout for 2023. Of course, they also still experienced sizeable unrealized losses that also mostly offset the realized gains.

In another month or so, we should get an updated semi-annual report with more recent numbers. However, doing a rough look at the NAV, we can see that it is running negative this year. That was mostly all happening in just the last couple of weeks as interest rates surged. When factoring in the distributions paid, returns would have held about flat so far.

YCharts

All this suggests that the fund isn’t covering its distribution as the NAV encompasses all the income and capital gains from all sources (investments realized/unrealized, options, and other various derivative strategies they employ.) Should this continue, then we should expect further distribution cuts, but for now, the NAV rate seems justifiable to keep it where it is.

IGA’s Portfolio

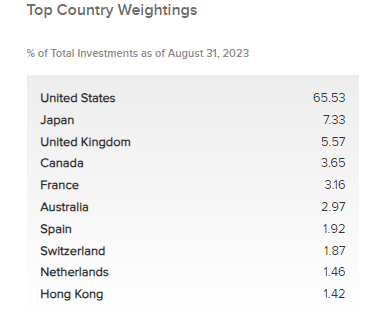

As mentioned, the fund takes a more hybrid approach rather than investing exclusively in global positions; they also incorporate a sizeable position in U.S. equities. This has increased a touch since our last update in terms of an even larger U.S. exposure, but it hasn’t been too meaningful. The country exposure for this fund is generally further away from the current conflict zones of Eastern Europe and the Middle East.

IGA Geographic Allocation (Voya)

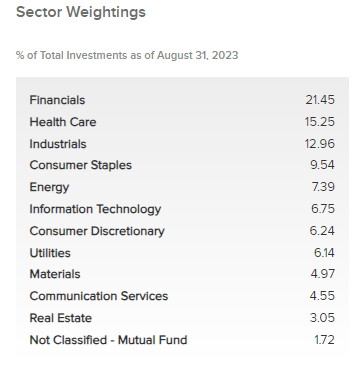

They’ve also taken a value-oriented portfolio positioning approach by overweighting financials, healthcare, industrial, consumer staples and energy before we see the weighting to tech. These weightings remain fairly consistent with where the fund was positioned in our prior update.

IGA Sector Allocation (Voya)

This sort of weighting with the implementation of their call-writing strategy is what seemed to have helped the fund hold mostly flat through 2022.

However, it’s also why the fund hasn’t produced anything too meaningful this year either and has mostly held flat on a total NAV return basis.

Utilities aren’t a major weighting in this fund, but with consumer stables healthcare, financial services and energy all being negative on a YTD basis in terms of sector performance, it’s clear to see why IGA would be struggling this year as well. In particular, consumer staples are having a tough time despite the uncertainty going forward, which would often warrant a shift to a more defensive tilt.

U.S. Sector Performance (Seeking Alpha)

That said, this area of the market does face the headwinds of rising interest rates. This is in more than one way as well. First, the more income-oriented investors can take positions in risk-free Treasuries and get competitive or even better yields in most cases than they can in defensive equities without the risks.

A second headwind for these sectors is the costs of their debt going forward, as it rolls over, will start to impact profitability. Some of these companies have really taken a lot of debt when it was free, but that environment is quickly changing, with Treasury rates rallying more recently. Of course, this isn’t all companies and some are better positioned in terms of hedges, fixed vs. floating and debt maturity schedules than others.

Naturally, with the limited changes we’ve seen in positioning geographically and sector-wise, the top positions of the fund have seen relatively immaterial changes since our last update as well. Which, this consistency has been quite consistent as it was mostly the same conclusion as our prior update – that is, even when the fund’s historically high turnover rate has averaged around 84% over the last five years.

IGA Top Ten Holdings (Voya)

The new names in the top ten are iShares Russell 1000 Value ETF (IWD) and Texas Instruments (TXN) making an appearance. Those have seen McDonald’s (MCD) and Bristol Myers Squibb (BMY) removed. Though they don’t provide a whole holdings list as of the end of August, we can see these were still positions at the end of May 2023, according to the N-PORT filing.

Conclusion

With some discount narrowing potential, Voya Global Advantage and Premium Opportunity Fund can be in a position where it could continue to outperform other equity benchmarks in the short and medium term. Global equities starting to perform better could be an additional catalyst to help the fund out.

However, the added diversification the fund presents, along with the call-writing strategy, could mean that in the longer term, it would still continue to underperform and instead is built more for a flat market overall. One where it can collect the premium and its underlying positions can continue to pay steady dividends.