We reiterate our buy rating on Taiwan Semiconductor Manufacturing Company Limited (NYSE:TSM) aka TSMC. While the slower-than-expected Chinese recovery and macro headwinds pressuring end demand momentum continue, we think the TSMC stock has now priced in the negatives; the stock has underperformed the S&P 500 (SP500) slightly since our cautious near-term outlook on the chip sector. TSMC stock is flat over the past six months since our April note, underperforming the S&P 500 by 6%. Since June highs, the stock has erased roughly $77B of its market cap due to investor concern regarding macro headwinds and consumer demand. We think the weakness is priced in and see end demand recovery in +44% of TSMC’s end market exposure happening in 2024, and longer-term growth tailwinds from A.I.

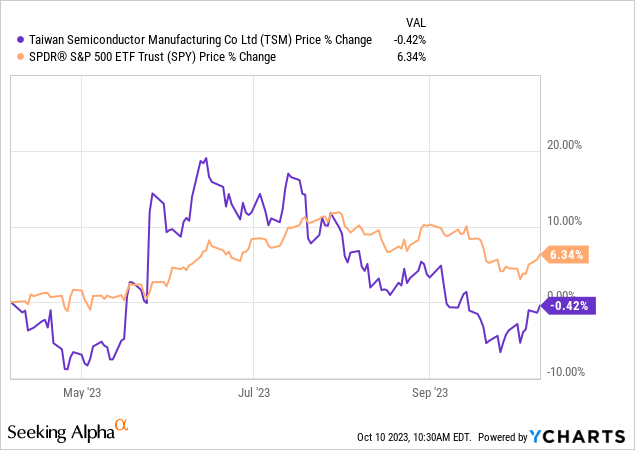

The following outlines TSMC stock performance over the past six months.

YCharts

We believe end market weakness weighing on TSMC’s top-line growth over the past four quarters has corrected, referring to PC, server, and smartphone markets. We expect the PC and server markets to recover in 2024, estimating that the PC and the Server total addressable market (“TAM”) will grow by 5% and 8% Y/Y, respectively, next year. We expect TSMC to meet or outperform the consensus expectation of 23% growth Y/Y. We’re already seeing signs of PC recovery after IDC published its Q3 2023 global PC shipment report yesterday, highlighting slower Y/Y declines in shipment by the top-five global PC vendors.

We’re less optimistic about smartphone end demand, although we believe the correction there is complete. Our data points for the smartphone end demand rebound are mixed for the near term; we think there is a lack of momentum to drive an uptick in demand. We think Apple (AAPL) iPhone sales in Q4 2023 will help improve demand a bit, but still see little to no sign of true recovery matching that of the PC market into 1H24. We think the smartphone TAM will remain flat Y/Y in 2024, potentially growing 2% Y/Y in a better-case scenario.

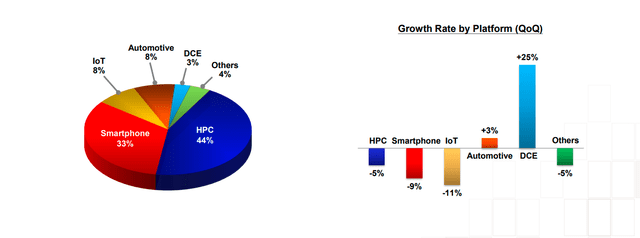

The following charts outline TSMC’s revenue exposure by platform for Q2 2023.

TSMC 2Q23 earnings presentation

Longer term tailwinds at play: A.I. & export ban

We don’t expect TSMC to outperform substantially in the near term due to a high capex-to-sales ratio and challenges to gross margin expansion, but we see longer-term growth drivers at play. We believe the potential expansion of the Biden administration export ban on China will work in TSMC’s favor. While we expect the likely ban expansion to pressure the semi-cap, specifically ASML Holding (ASML), Lam Research (LRCX), and Applied Materials (AMAT), we see a different scenario playing out for TSMC. We think the likelihood of an expansion to the ban is very real after Huawei launched its 5G smartphone in spite of U.S. attempts to tighten the grip on China’s access to advanced tech.

Additionally, we expect the strong A.I. demand to drive material revenue growth for TSMC. The main benefactor of the A.I. boom this year is Nvidia (NVDA), and we think NVDA’s growth rate will reflect positively on TSMC’s earnings into 2024 as demand continues to outpace supply for A.I. servers. We think it’s still too early to be concerned about double-ordering and a potential correction; we think the correction should be on the radar late next year.

Valuation

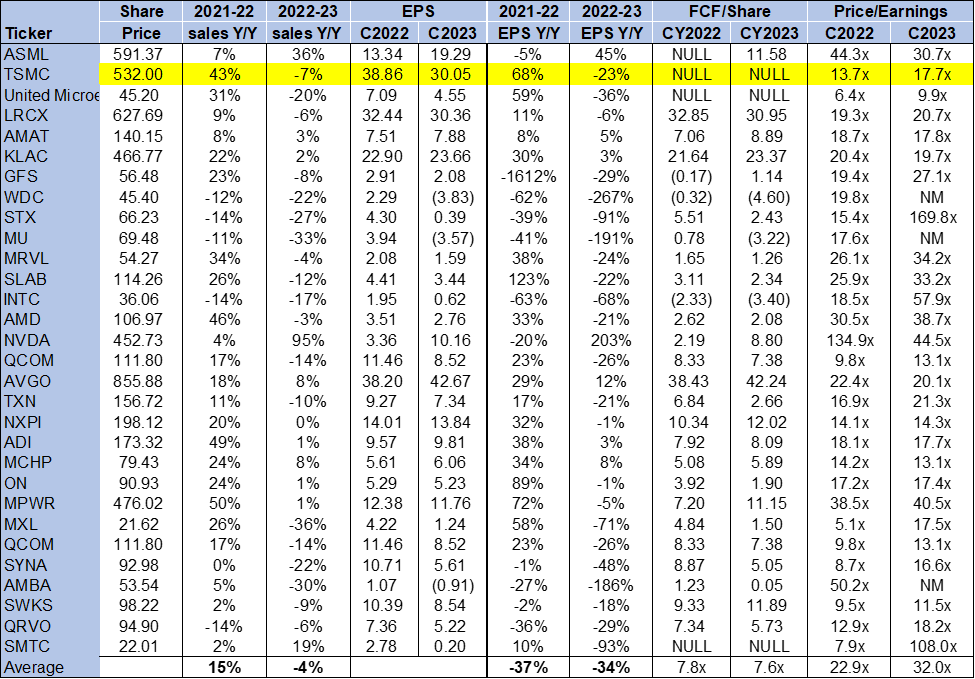

TSMC stock is trading well below the peer group average for its position in the foundry market. On a P/E basis, the stock is trading at 17.7x C2023 EPS $30.03 compared to the peer group average of 32.1x. The stock is trading at 5.85x TTM EV/Sales versus the peer group average of 5.5x. We see attractive entry points into the stock at current levels.

The following chart outlines TSMC’s valuation against the peer group.

TSP

Word on Wall Street

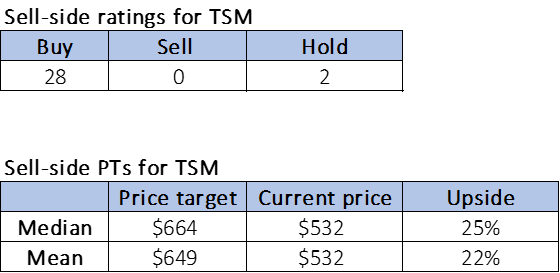

Wall Street shares our buy-rating on TSMC stock. Of the 30 analysts covering the stock, 28 are buy-rated, and the remaining are hold-rated. We think the overwhelmingly bullish sentiment on the stock results from TSMC’s dominant position in the foundry market and anticipation of end demand recovery in 2024.

The following charts outline TSMC’s sell-side ratings and price-targets.

TSP

What to do with the stock

We remain buy-rated on TSMC. We now see a clear growth runway for the stock as PC and server end demand recovers in 2024. While data points for smartphone demand remain less clear, we expect to see a solid recovery toward 2HCY24. We think the macro weakness has been priced into the stock since July highs and into the outlook for 2HFY23. We see longer-term growth drivers due to potential ban expansion and A.I. tailwinds. We recommend investors explore entry points into TSMC at current levels to ride the upward trend in 2024.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here