Smiths Group (OTCPK:SMGZY) is a technology firm serving the security and defense, energy, and aerospace markets worldwide. SMGZY reported solid FY23 results. Their financial performance is quite solid, and the valuation also looks cheap, but I don’t think investing in it right now will be a good decision. I will analyze its annual results and discuss why one shouldn’t invest in it right now in this report. I assign a hold rating on SMGZY.

Financial Analysis

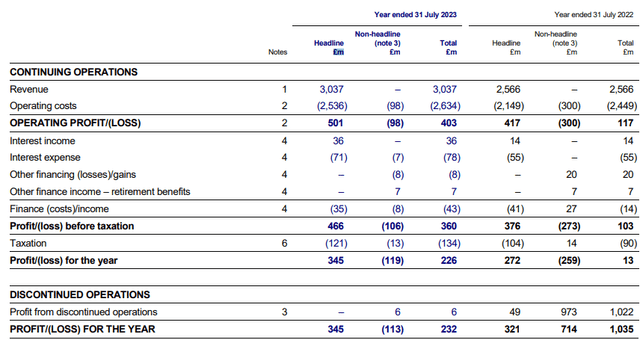

SMGZY recently posted its FY23 results. All the figures are in Pound sterling. The revenue for FY23 was £3 billion, a rise of 18.3% compared to FY22. Strong performance in its John Crane, flex-Tek, and Smiths Detection divisions was the reason behind the revenue growth. The revenue in the John Crane division grew by 19.8% in FY23 compared to FY22. This division benefitted from the strong demand for emissions reduction solutions and chemical processing, which were the major reasons behind the revenue increase in this division. The revenue in the flex-Tek division grew by 18.6% in FY23 compared to FY22. Higher new aircraft builds, and strong demand for the HVAC applications in the first half of FY23 benefitted this division. The revenue in the Smiths Detection division grew by 22.6% in FY23 compared to FY22. A strong demand for its 3D CT machines was the major reason behind the revenue growth.

SMGZY’s Investor Relations

The headline operating profit margin for FY23 was 16.5%, which was 16.2% in FY22. The margins benefitted from better pricing and improved supply chain. Its ROCE also improved to 15.7% in FY23, which was 14.2% in FY22. I believe FY23 was an excellent year for the company. They saw improvement in every aspect. The profitability and margins improved, and the revenue saw significant growth. However, I expect the revenue growth in the first half of FY24 might not be as significant as it was in FY23. The housing market in the U.S. is experiencing a slowdown, the mortgage rates are at a 20-year high, and the semiconductor market is also experiencing weakness. So, their U.S. construction and Interconnect business might be adversely affected, which can affect the company’s revenue growth in FY24. But, their business is quite diverse and spread across many markets, which is their strength. Their energy and aerospace market has been experiencing solid growth and is expected to boost the company’s revenue growth in FY24. There are some headwinds in their construction and industrial business, but still, I expect them to report positive revenue growth in FY24, although the growth might not be as significant as it was in FY23.

Technical Analysis

Trading View

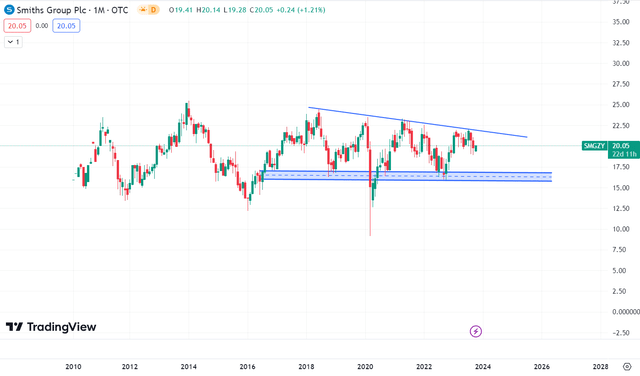

SMGZY is trading at the $20 level. Since its debut in 2010, the stock has been trading in a range. In the last 13 years, the stock has neither been in an uptrend nor a downtrend. It is simply consolidating between the range of $12-$25. So, if you buy it at the current level, there is a high chance that your money might get stuck for a long time. Hence, buying this stock at the right level becomes very important. So, in my opinion, there are two buying scenarios. First, if the stock breaks the trendline from which it has been facing resistance for the last five years. The trendline is at $22.5; if the stock breaks the level, we might see an upward rally. The second buying opportunity will arise if the stock reaches its support zone of $16.5. The $16.5 level has been a strong support zone for the stock since 2017, so if the stock reaches this level, I believe one can initiate buying as it will provide a better risk-to-reward trade as the downside is limited. But until then, it will be best to avoid the stock. Hence, I assign a hold rating on SMGZY.

Should One Invest In SMGZY?

First, look at SMGZY’s valuation. SMGZY has a P/E [FWD] ratio of 14.45x, which is lower than the sector median of 17.2x. It has a PEG [FWD] ratio of 1.27x compared to the sector median of 1.61x. The growth they experienced in FY23 was impressive. So, according to the valuation ratios and the results, I think SMGZY is undervalued. But the undervaluation doesn’t mean that one should buy it. The timing also matters a lot, and buying the stock right now might not be a beneficial decision because doing so could keep you in the stock for a very long period without producing any returns. In my opinion, one should wait for the price breakout or price to reach the support to buy the stock. The stock has been stuck in a range for over a decade and might continue to trade in the range. Hence, considering all the factors, I assign a hold rating on SMGZY.

Risk

The world is currently facing catastrophic global energy market inflation and general worldwide inflation. Rates are rising at central banks all around the world to combat inflation. Smiths have the danger of having to pass on growing labor, material, and transportation costs through price. Additionally, there is a chance of a regional or worldwide recession as central banks attempt to reduce inflation, which would put pressure on their revenue growth and profitability. Geopolitical tensions and the emergence of trading blocs may have further effects on the free flow of capital, goods, and people, as well as increase supply chain volatility and limit market opportunities.

Bottom Line

SMGZY reported strong annual results, and the valuation also looks cheap. But the stock has been stuck in a range for over a decade and might continue trading in a range. Hence, I believe investing right now might not be a wise decision. Hence, I would suggest to wait for the right opportunity to arise and utilize it when it happens. But until then, I would suggest avoiding it. Hence, considering all the factors, I assign a hold rating on SMGZY.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here