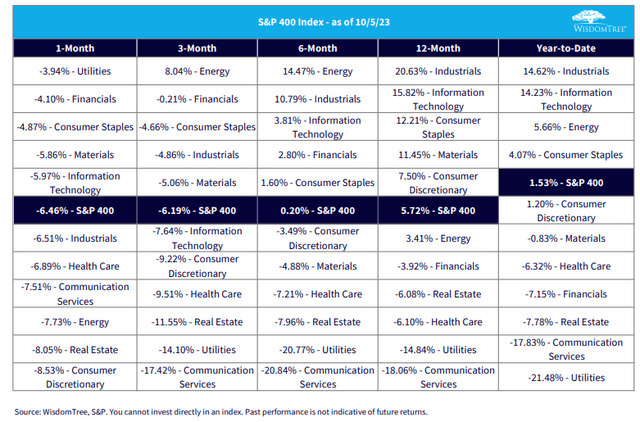

What’s the best-performing sector in 2023? You might say something tech-related. While that is true among large-cap US equities, small and mid-sized companies within the Industrials sector shine brightest among the 11 market groups. It’s not all rosy, though. Higher interest rates and overall corporate pessimism are key risks for business services companies.

I reiterate my hold rating on Cintas (NASDAQ:CTAS). It is an earnings powerhouse, though its dividend is small and free cash flow is somewhat light. With a lofty valuation and technical uptrend, there continue to be mixed signals.

Industrials Beating Tech Under the Market’s Surface

WisdomTree

According to Bank of America Global Research, Cintas is the leading North American provider of corporate uniform rental programs. The company also provides mats, restroom cleaning and supplies, first aid and safety products, and fire protection services, all delivered through its recurring route-based service model.

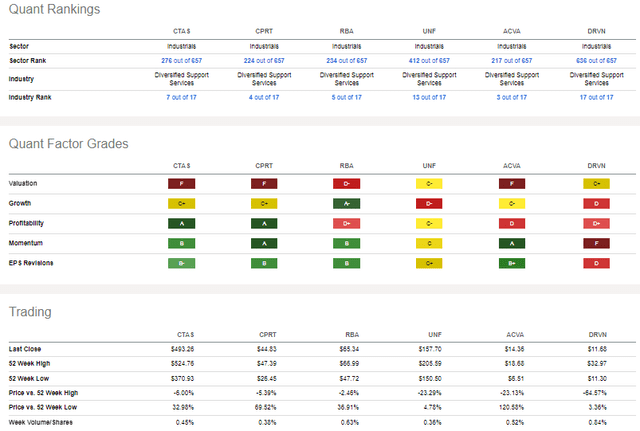

The Ohio-based $50.2 billion market cap Diversified Support Services industry company within the Industrials sector trades at a high 37.1 trailing 12-month GAAP price-to-earnings ratio, pays a small 1.1% dividend yield, and, ahead of a shareholder meeting later this month, shares trade with a low 19% implied volatility percentage and a modest short interest of 1.3%.

Last month, CTAS reported a strong start to its FY 2024. Earnings per share topped Wall Street’s expectations modestly ($3.70 vs $3.68) while revenue rose more than 8% year-on-year to $2.34 billion – in line with estimates. Shares fell on September 26 immediately after the numbers crossed the wires, though, even considering an optimistic guidance increase.

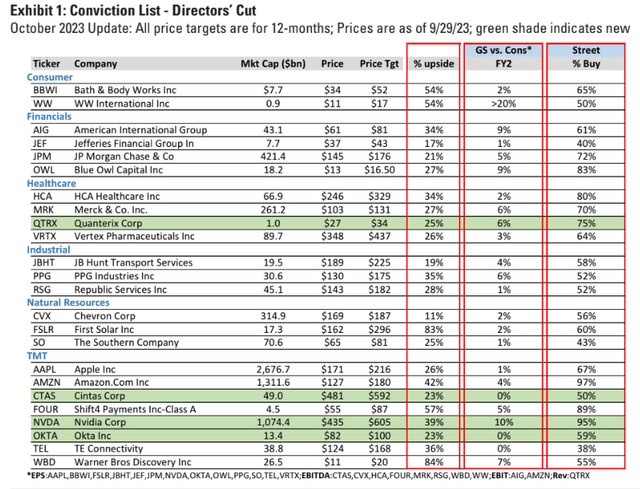

The management team now expects better performance figures due to solid volume growth, effective cost control measures, and energy costs that are easing from year-ago levels. Importantly, the firm reported a better-than-expected EBIT margin – that metric notched new highs in its Q1, and it forecasts continued margin expansion later this fiscal year. Just recently, following the Q1 EPS report, CTAS was added to Goldman Sachs’ conviction buy list.

Cintas Added to Goldman’s Conviction Buy List

Goldman Sachs

Key risks for the firm include intense competition from peers such as Aramark and Unifirst and broader economic sensitivity, though a hot September jobs report suggests that risk is less of a concern.

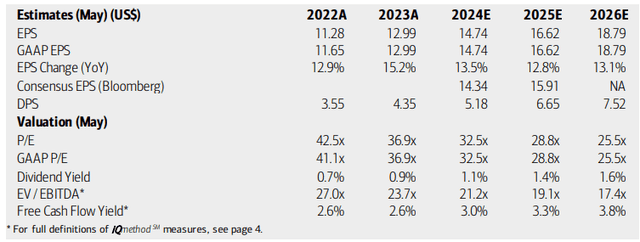

On valuation, analysts at BofA see earnings rising materially this year to nearly $15 (the firm is already operating in its FY 2024), and continued double-digit EPS growth is seen through 2026. The Bloomberg consensus forecast is slightly less sanguine compared to BofA’s outlook. Dividends, meanwhile, are seen growing at a fast clip, though the overall yield is expected to remain under 2% over the coming quarters. You have to pay up for the fast grower, however, as both the operating and GAAP P/E ratios are above 30 right now. Moreover, CTAS sells at a high EV/EBITDA multiple and it is expensive on a free cash flow basis.

Cintas: Earnings, Valuation, Dividend, Free Cash Flow Forecasts

BofA Global Research

Back in March, I was too pessimistic about CTAS. My hold rating asserted that shares were about 10% overvalued. Value investors were left out on this one as a nearly 20% rally ensued to the September peak just shy of $525. With the stock back under $500, the current non-GAAP forward P/E remains expensive.

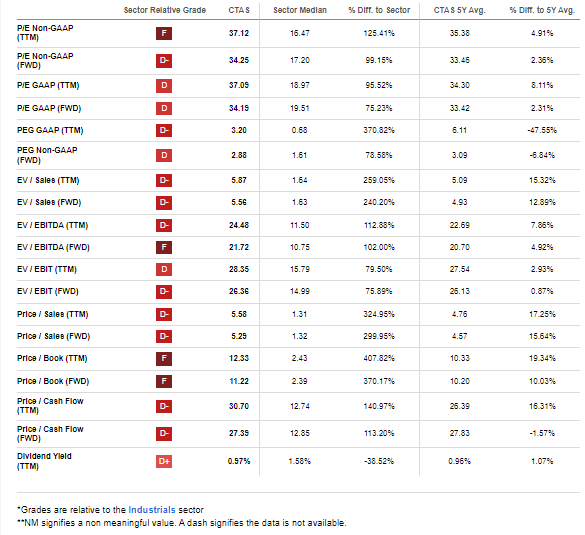

The PEG ratio, assuming about 14% earnings growth, is thus near 2.5 by my calculations (2.88x according to Seeking Alpha). That is near the 5-year average on the stock while most other metrics are to the pricey side on both an absolute basis and, particularly, relative to the Industrials sector. If we assume 2026 EPS of $18 and apply a 25 multiple, then shares should be near $450, so I still see the company as expensive.

CTAS: Expensive On Valuation

Seeking Alpha

Compared to its peers, Cintas features a comparable valuation, though I contend that the growth rating is selling the firm short considering the sustainable low-double-digit EPS growth rate. Profitability is robust, though, while share-price momentum has been solid in 2023. With generally positive EPS revisions and improved margins, the earnings story appears intact.

Competitor Analysis

Seeking Alpha

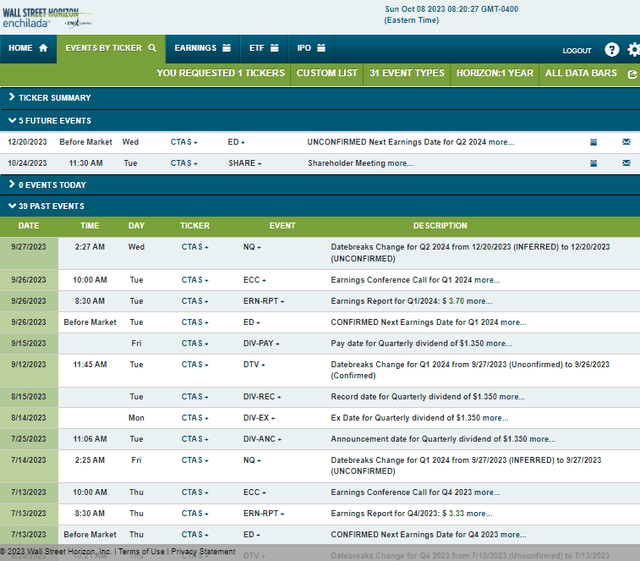

Looking ahead, corporate event data provided by Wall Street Horizon shows an unconfirmed Q2 2024 earnings date of Wednesday, December 20 BMO. Before that, the firm hosts a shareholder meeting on Tuesday, October 24, which could bring about some share price volatility.

Corporate Event Risk Calendar

Wall Street Horizon

The Technical Take

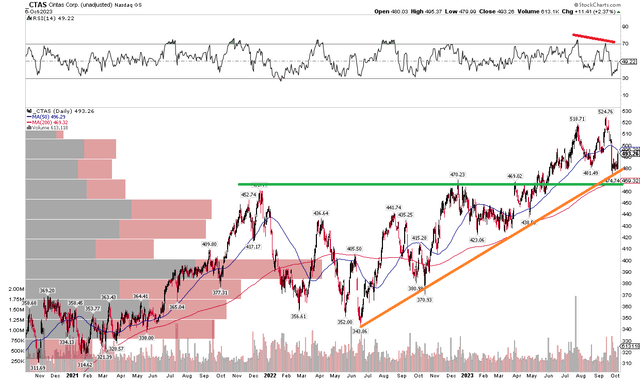

CTAS broke out from a “messy chart” as I had described it back in Q1. Notice in the graph below that the $460 to $470 range was key resistance from late 2021 through this past May. I alerted investors to pay attention to that level in the previous article, and a bullish breakout indeed took place late in the second quarter. After spiking to an all-time high above $520 in September, shares retreated to previous resistance (now support) just above $470.

Also take a look at the rising 200-day moving average – CTAS has been above that trend indicator line since November last year, and the bulls defended it last month during the correction after the RSI momentum indicator (at the top of the chart) printed a bearish divergence. Longer-term, an upside breakout from a cup and handle pattern earlier this year triggered a bullish measured move price objective to near $580 based on the height of the previous pullback and resistance line.

Overall, the uptrend is also intact and $460 to $470 is important support.

CTAS: Bullish Uptrend, Cup & Handle Target to $580

Stockcharts.com

The Bottom Line

I reiterate my hold rating on Cintas. It remains a richly priced stock with strong earnings potential while the technical trend is up after an impressive 16-month advance.

Read the full article here