What a powerful finish as the S&P 500 (SPX) (SPY) and the Nasdaq (NDX) (NASDAQ:QQQ) shook off early pre-market declines on Friday (October 6) as investors reacted to the robust jobs market report. I last held a Neutral view of the Nasdaq in my previous update, as I wanted to ascertain the robustness of the market action before revising my rating.

Notably, the report demonstrated that the bearish prognosticators hammering home their recessionary thesis have been off the mark significantly over the past year. Yet, they continue to bang the table and have not been able to prove their point since the market bottomed out in October 2022.

Bearish investors continue pointing to the surge in bond yields, as the 10Y Treasury yield (US10Y) surged well above their highs in October 2022, reaching 4.89% this week.

Given the recent surge, I previously held a more bearish view of the US10Y, but that thesis has been invalidated. Still, a possible bull trap could form in its long-term chart, suggesting that bondholders should avoid selling further at a possible long-term bottom, allowing the market to consolidate.

These bearish prognosticators could point to the surge in bond yields as hugely damaging to the tech-heavy Nasdaq. However, they shouldn’t “conveniently” ignore the observation that QQQ is nearly 45% above its October 2022 lows. As such, it is clear that the market has continued to shrug off the so-called bond yield headwinds on the Nasdaq despite its more expensive valuation than the S&P 500. Investors are likely anticipating that the Fed is very close to its peak rate hikes, which corroborates the price action seen in the Nasdaq.

As such, it makes sense for investors to focus more on forward earnings prospects and less on the surge in bond yields, which hasn’t led to a significant valuation downgrade in the Nasdaq.

QQQ last traded at a P/E of about 22.5x, markedly higher than the 18x on the SPY. Yet, it didn’t stop the buyers from lifting the optimism on the QQQ, as it formed an astute bear trap (false downside breakdown) to finish robustly in its first trading week for October. As I explained in a recent SPY article, Q4 is a seasonally bullish quarter for the market. As such, the robust price action validates buyers are seemingly ready to continue QQQ’s bullish bias, notwithstanding the recent surge in bond yields to levels not seen since 2007.

Investors could ask why the market formed the bullish reversal despite the increasing possibility that the Fed could delay its rate hikes further into the final quarter of 2024. Why did buyers return with such aggression on Friday, helping to validate a bear trap that likely ensnared early sellers who bought into the bearish thesis emanating from the robust jobs report?

To be clear, I have the intellectual honesty to tell you that I don’t have all the answers to your questions (I don’t have a crystal ball). But, really, does it matter? When you focus on price action, valuations, and investor psychology, what matters is whether they are aligned and have the relevant information for me to decide based on an actionable thesis.

I have highlighted to members in my service that investor psychology is highly favorable for the market to bottom out. Fear gauges are at pessimistic levels last seen in March 2023, some even lower (more pessimistic). As such, those who wanted to sell have likely sold, as the strong hands returned to pick up the pieces from the weak ones at the lows.

How about valuations? I highlighted in my article yesterday that the US market is undervalued by quite a fair distance compared to July. Tech sector valuation has also dropped markedly, with some stocks like AMD (AMD) already fallen into a bear market. As such, tech (XLK) is also no longer overvalued.

While I assessed that tech could underperform relatively to the market over the next six months, the Nasdaq has an ex-tech exposure of about 51%. As such, the relative undervaluation in high-weightage sectors such as communications (XLC) and consumer discretionary (XLY) would help mitigate possible near- to medium-term weakness in tech. Accordingly, communications and consumer discretionary accounted for about 16% and 14% of QQQ’s exposure, respectively.

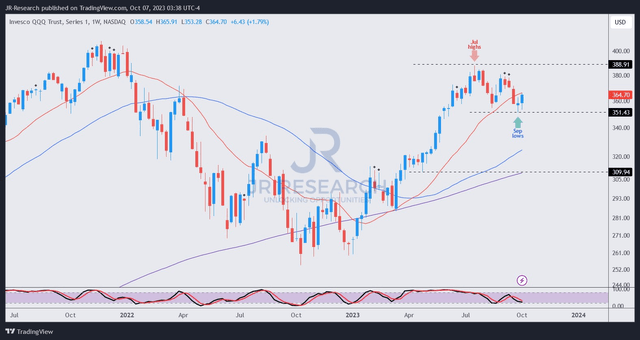

QQQ price chart (weekly) (TradingView)

Yesterday’s powerful bullish reversal in the regular session helped negate all the pre-market losses and more, as QQQ finished strongly. As such, it validated the bear trap pivot formed in late September, which took out the dip-buying lows in August.

As such, I assessed that QQQ is well-primed to restart the next leg in its uptrend continuation (valid since March 2023), as it took a well-deserved break over the last three months.

Don’t miss this one if you missed the early entry points in late 2022 or early 2023.

Rating: Upgraded to Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Read the full article here