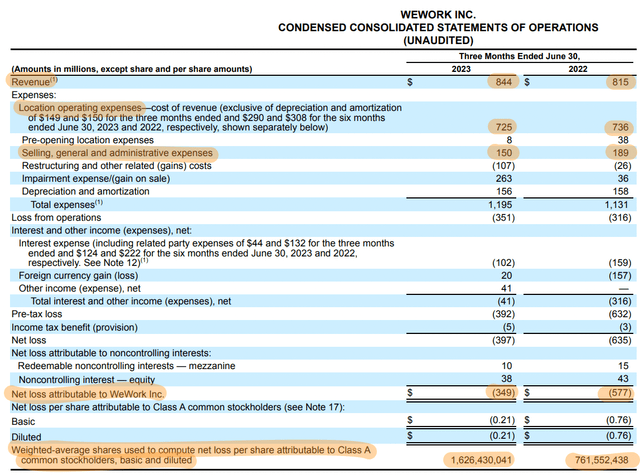

Let’s start with the good. WeWork Inc.’s (NYSE:WE) most recent fiscal 2023 second quarter earnings somewhat validated the argument by bulls of the shift to hybrid working in the remote working post-pandemic zeitgeist forming a tailwind for the company. WeWork recorded consolidated revenue of $844 million, up 3.6% year-over-year and a beat by $3.93 million on consensus estimates. This was driven by physical occupancy that expanded 200 basis points to 72% from its year-ago comp.

The role and relevance of offices have been subject to a plethora of competing takes since the pandemic struck, but the overwhelming consensus has been that hybrid working arrangements will remain sticky. This is when workers are able to mix and match working from home and in-office work.

WeWork Inc. Fiscal 2023 Second Quarter Form 10-Q

Rising office vacancies across the U.S. could translate into enterprise demand for shared workspaces that still allow for the benefits of in-person work to be actualized, together with the cost and efficiency gains from not being tied to a long-term lease. Hence, WeWork’s core business is growing. If you’re short on office real estate investment trusts, or REITs, WeWork in a way represents a mild play on the other side of this trade.

Think about it. Company A’s lease comes up for renewal, but it’s facing higher interest payments, broader pressure to cut costs, and only half of its employees are in the office. WeWork is a flexible hybrid option. However, the company represents a poor investment due to its highly indebted balance sheet and lease payments, which have rendered its future bleak and materially heightened the specter of a Chapter 11 bankruptcy filing.

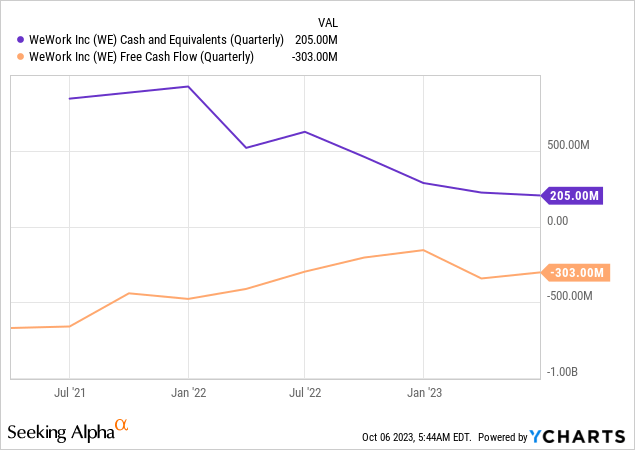

WeWork’s Cash Dwindles As Free Cash Outflow Remains Elevated

WeWork is not in great shape. Location operating expenses at the end of its second quarter at $725 million means it only has around $119 million in net location revenue before other expenses. Selling, general, and administrative expenses came in at $150 million to place its income statement in negative territory before other operating expense line items. WeWork recorded a net loss of $349 million for its second quarter, down from $588 million in the year-ago comp, but still at a level that’s unsustainable. Even more unsustainable is free cash outflow that came in at $303 million, a dip sequential from $343 million from the prior first quarter.

You can calculate a very rough estimate of a company’s cash runway by simply taking free cash outflow away from cash and equivalents. WeWork does have access to an expanded liquidity backdrop of $680 million, as it has only drawn down $175 million from $475 million of capacity available under its first lien notes delayed draw. Hence, there are actually enough funds for a few more quarters, assuming cash burn continues to match the second quarter. That free cash outflow remains high against intense efforts to exit leases since 2019 is concerning. WeWork has exited or amended 590 leases since 2019, reducing around $12.7 billion in fixed lease payments. More needs to be done and the company skipping $95 million in interest payments is a tactic to help renegotiate long-term debt of $2.91 billion as well as $14.16 billion in upcoming capital leases.

Huge Concessions Needed

The trend line is clear, WeWork needs huge concessions from its lenders and landlords, or it won’t see the summer of calendar 2024 without having gone through the Chapter 11 process. The company has been able to taper over some of this burn through the expansion of its share count which more than doubled year-over-year, contributing to a share collapse that forced a 1-for-40 reverse stock split to regain compliance with NYSE minimum listing rules. A going concern warning was issued in light of all the chaos seen in its second-quarter earnings. WeWork skipping interest payments could strong-arm its lenders into making needed concessions.

Chapter 11 would be messy and WeWork broadly does not own its physical property footprint, so lenders would find it hard to recoup their principal balance. Its landlords would also have to re-lease their building into an office market where vacancy rates continue to rise, whilst facing higher interest payments on their own respective debts. There likely isn’t going to be another WeWork anytime soon, and these properties might be sitting empty for years. The company has a 30-day grace period, from 2 October 2023, to make the interest payments on the debt, or it’s recorded as a default.

Conclusion

What’s the play here? To do nothing. WeWork Inc. is not a serious investment, it never has been since going public via SPAC, and the current chaos is a culmination of what’s been an incredibly unsustainable business model. The fate of the company now depends on just how many concessions it can get out from its lenders and landlords. I’ll remain on the sideline.

Read the full article here