It’s been a rough past two months for the restaurant sector, with the AdvisorShares Restaurant ETF (EATZ) plunging ~19% in barely 50 trading days, erasing nearly all the index’s year-to-date gains. However, while the index has stayed afloat in positive territory year-to-date (albeit barely), Denny’s (NASDAQ:DENN) hasn’t fared nearly as well. This is evidenced by the stock being down 8% year-to-date and 65% from its highs, massively underperforming large-cap quick-service names like Yum Brands (YUM) and McDonald’s (MCD) which made new all-time highs earlier this year. And while Denny’s likely isn’t getting cheaper following this pronounced period of underperformance, it’s tough to argue for an investment just yet, especially with industry-wide traffic continuing to be choppy. Let’s take a closer look below:

Denny’s Restaurant – Company Website

Recent Results & Q3 Outlook

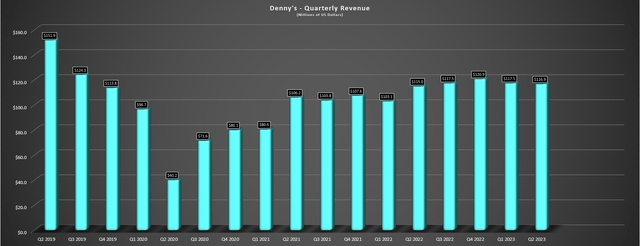

Denny’s released its Q2 results in August, reporting revenue of $116.9 million, a marginal increase from the year-ago period. This was driven by domestic same-store sales of 3.0% which was well below effective pricing implying a moderate dip in traffic, and the company’s two-year stack same-store sales was of 6.8% was well below peers like First Watch Group (FWRG) with delivered ~21.0% two-year stacked same-store sales in the period. Meanwhile, from a development standpoint, the brand saw 10 franchise openings including four international and 1 Keke’s, but it has still shed over 42 net new stores on a year-over-year basis excluding the Keke’s acquisition, resulting in just 1% growth including its Keke’s acquisition for ~$82 million.

Denny’s – Quarterly Revenue – Company Filings, Author’s Chart

Overall, these results were a little disappointing, and the margin performance wasn’t all that inspiring either. This is because while margins bounced back because of easy year-over-year comps, they remained well below pre-COVID-19 levels at just 15.1%, down 150 basis points on a four-year basis vs. Q2 2019. This is over 500 basis points below the newest entrant into the breakfast segment, First Watch, and development also trailed by miles. On the call, management noted that lower franchise revenue was mostly related to kitchen equipment sales in the year-ago period, and that it took advantage of the share price weakness to repurchase ~$10.4 million worth of shares, with ~$133 million still available. At current levels, reducing the float makes sense, but the market may not love this strategy with the company sitting on over $250 million in debt.

Finally, from a financial standpoint, Denny’s reported $12.7 million in adjusted free cash flow, benefiting from lower capital expenditures in the period. Meanwhile, adjusted EBITDA improved to $22.3 million, up from $17.2 million in Q2 2022. That said, labor related costs remained relatively high as a percentage of sales at over 37%, and while the company reported an improved outlook for commodity inflation for the year of 1-3% vs. 4.6% previously, same-store sales guidance remained at an uninspiring 3-6%, suggesting that it’s seeing the same soft traffic trends that are being reported sector-wide. On a positive note, though, the company’s new Rewards program appears to be gaining some traction, with 200,000 new Rewards members since its June 22nd launch, and improving net sentiment scores which are outpacing its peer group according to Black Box Intelligence.

Industry-Wide Trends

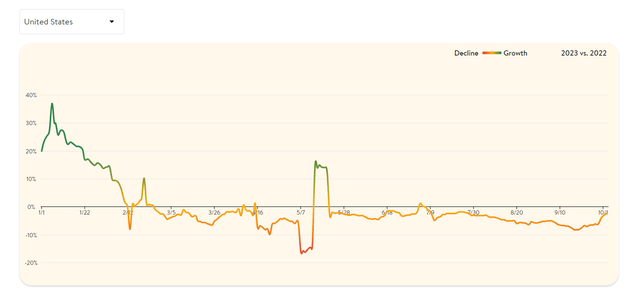

2023 has been a tough year from a traffic standpoint for most segments of the restaurant industry, but while the first half of the year wasn’t great, things have not improved, at least according to OpenTable data which measures seated diners in the United States. In fact, as shown below, January saw strong traffic growth year-over-year after lapping Omicron, and there were brief spikes into double-digit positive territory in February and May. However, since May, seated diner growth has struggled to even return to positive territory and while it improved to start Q2, which led to somewhat positive commentary when discussing quarter-to-date traffic in the Q2 results industry-wide, we can see that it decelerated sharply throughout the quarter. This decelerating lined up with a return to higher gas prices, which can further dampen consumer confidence, and gas prices have remained elevated sequentially (Q3 vs. Q2) since then.

Seated Diners 2023 vs. 2022 – OpenTable

As for Black Box Intelligence data, the results aren’t much better here, with August comparable traffic negative yet again at 2.9%, with exceptions being Italian (cuisine) and quick-service (segment) which performed the best. Unfortunately, Denny’s belongs to neither category and fits into the casual dining space where the trends are clearly worse than Black Box Intelligence data, which covers a larger portion of the sector and includes quick-service and fast-casual. Plus, competition has heated up in the breakfast space with First Watch Group growing units like a weed since going public and continuing to report much stronger traffic than many of its peers, suggesting it could be taking some market share given its differentiated offerings with fresh ingredients and regular menu refreshes, and a more similar concept to Keke’s which Denny’s acquired last year.

Black Box Intelligence – August Sales & Traffic Stats – Black Box Intelligence

The silver lining is that at least turnover appears to be improving sector-wide, which Denny’s also called out, and the industry is getting some relief from a commodity inflation standpoint with many companies calling for low single-digit to flat inflation after lapping peak inflation for many commodities in Q3/Q4 2022. That said, the labor situation isn’t getting any easier with rising minimum wages and other retail brands raising wage rates to help with retention and ensure they’re positioned for growth, suggesting that even if Denny’s is benefiting on the commodity side, any gains could be offset by sticky labor inflation. And while the relief is nice to see, it doesn’t help if the top line struggles to grow with choppy traffic trends, still ~25% of Denny’s in the system not taking advantage of late-night (a key daypart), and a difficult decision when considering raising menu prices to ensure it doesn’t price its lower-end consumers out of regular visits.

Given this setup, I am less confident in Denny’s ability to enjoy positive traffic in Q4 and next year, and it’s tough to forecast much growth for the business when it’s still shedding net units on a consolidated basis. Plus, from a margin standpoint, the pre-COVID-19 margins look like a distant memory for brands like Denny’s, especially given its need to offer value vs. other brands that have been more aggressive with pricing and leaned into different concepts like Chipotle (CMG) to boost average unit volumes and claw back any margin losses. So, while 2025 might be better as we see more openings for Keke’s which can offset the net closures for its primary Denny’s brand, this is not a growth stock currently and I don’t see the valuation reflecting this yet, even if the stock has come down substantially from its highs. Let’s dig into the valuation below:

Valuation

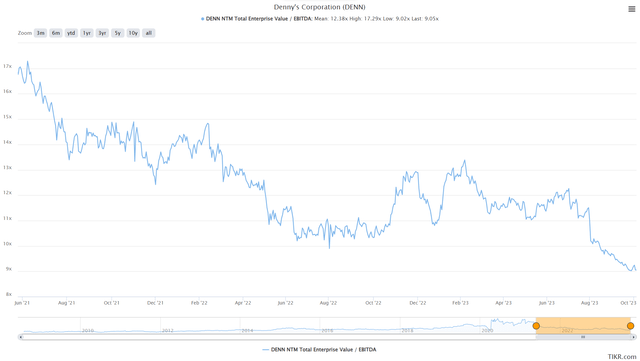

Based on ~56 million shares and a share price of $8.50, Denny’s trades at a market cap of $480 million and an enterprise value of ~$850 million. This is a very reasonable valuation for a company with a system of its size if it were a growth story, with Denny’s finishing the quarter over 1,640 restaurants, with an industry-leading ~96% of these restaurants being franchised. In fact, this valuation has left Denny’s trading at just ~13x EV/FCF using FY2024 estimates and less than 10x forward EV/EBITDA, giving it one of the highest free cash flow yields in its peer group. However, it is hardly a growth story, with 42 net closures year-to-date (ex-Keke’s) or just 1% unit growth following the acquisition of Keke’s last year. And while a 7% free cash flow yield might be a steal for a mid-cap company with double-digit sales growth, I think it’s more difficult to argue that this is enough of a margin of safety for a small-cap name with low single-digit sales growth, and non-existing unit growth on a consolidated basis for the time being.

Denny’s – EV/EBITDA Multiple – TIKR.com

So, what is a fair value?

Using what I believe to be a more conservative multiple of 12.5x free cash flow for a small-cap, low-growth restaurant brand, I see a fair value for Denny’s of $9.60 based on an estimated 52 million shares outstanding at year-end 2024. This points to a 13% upside from current levels, which might entice some investors in betting on a turnaround. However, for small-cap names, I am looking for a minimum 30% discount to fair value to justify starting new positions. And if we apply this discount to Denny’s, the ideal buy zone for the stock comes in at $6.70 or lower. Obviously, there’s no guarantee that the stock gets to this level, but with an unfilled gap in this area and several more attractively valued small-cap names elsewhere in the market, I think it’s hard to justify rushing into the stock at $8.50.

Summary

Denny’s continues to see progress on turning things around and the restaurant’s value proposition, revamped Rewards program, and acquisition of a new concept in Keke’s could help Denny’s to report better same-restaurant sales and return to net unit growth by 2025. That said, we are seeing softer than hoped trends for industry-wide traffic (especially in casual dining), we could see more companies become promotional to drive sales which would increase competition in Denny’s value category, and this means it’s more difficult to be optimistic about the stock beating estimates going forward. Assuming this was more than priced into the stock with it trading at a 12% plus free cash flow yield, this wouldn’t be an issue, but with the stock trading at 13x EV/FCF, I continue to see better bets elsewhere. Hence, although Denny’s is reasonably valued here, I would need to see a pullback below $7.00 to get more interested.

Read the full article here