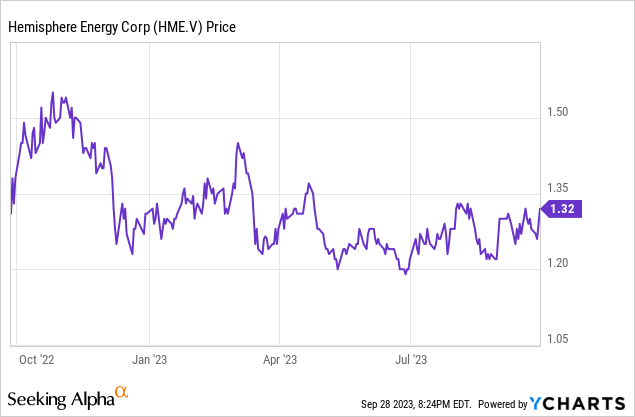

Introduction

Back in July, I argued Hemisphere Energy (TSXV:HME:CA) (OTCQX:HMENF) was an interesting dividend candidate thanks to its strong dividend policy. The company is paying a quarterly dividend of C$0.025 per share which represented an 8% dividend yield, but Hemisphere’s dividend policy bases the dividends on the operating cash flow. As the oil price was going up (and subsequently continued to increase throughout the third quarter) I argued the dividend would likely be increased. This has now happened. And although the Q3 results obviously still have to be reported, Hemisphere has just announced a C$0.03 special dividend, bringing the anticipated dividend for the year is C$0.13 for a yield of in excess of 10%. I wanted to have another look at the stock to figure out how strong the third quarter will be.

The Q2 results allow us to run the numbers on Q3

Before diving into my expectations for the third quarter, it’s important to have a closer look at the Q2 results as that will be the starting point for my Q3 projections.

As Hemisphere Energy mainly produces heavy oil (representing in excess of 99% of the total oil-equivalent production), the WCS price and the differential between light oil and heavy oil is very important for the company (and its shareholders).

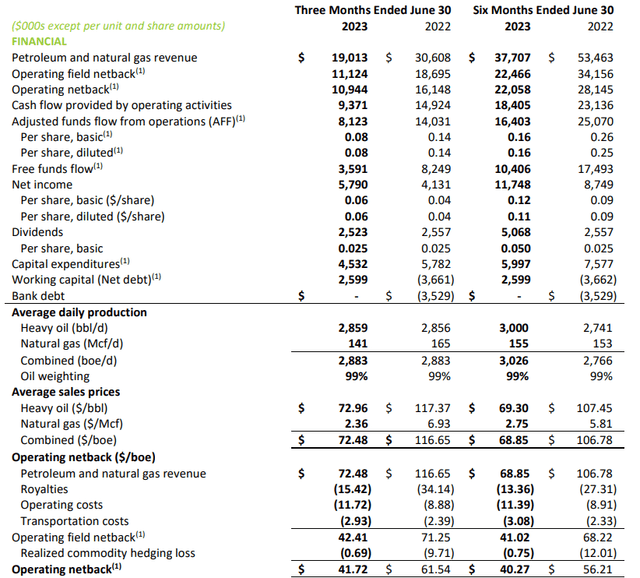

During the second quarter of the current financial year, Hemisphere reported an average realized price of C$73 for its heavy oil and about C$2.36 for the very small amount of natural gas that was produced during the quarter. This resulted in an average received price of C$72.48 per barrel of oil-equivalent and this meant the total netback was C$42.41 per barrel of oil-equivalent, excluding hedge losses. The highest operating cost wasn’t the pure production cost or the transportation expense, but the royalties. As you can see below, the royalties made up about 50% of all production costs.

Hemisphere Investor Relations

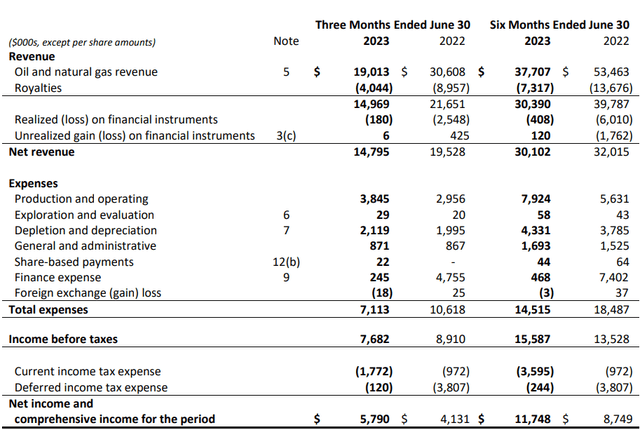

The total revenue reported by Hemisphere in the second quarter was approximately C$19M and about C$15M after taking the royalty payments into consideration. The total net revenue of C$14.8M also included about C$0.2M in hedging losses.

Hemisphere Investor Relations

And the income statement obviously also provides evidence of the low cost nature of the production. The total production costs were less than C$4M and depletion and depreciation expenses made up about 30% of all operating expenses. That’s great as this meant the pre-tax income came in at C$7.7M representing a net profit of C$5.8M after covering a C$1.9M tax bill. This means the EPS in the second quarter was roughly C$0.06 and this obviously also means the quarterly dividend of C$0.025 per share is very well covered as the payout ratio is less than 50%. And that was based on an average realized price of just C$73 per barrel for the heavy oil.

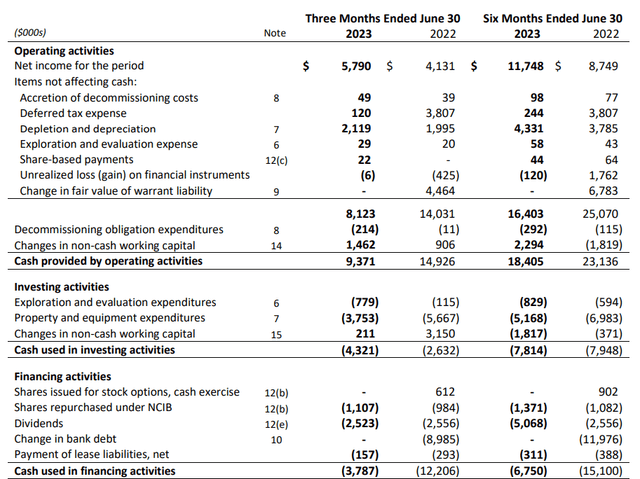

This wasn’t just an accounting profit as the company’s cash flow statement appears to back up the strong net profit.

The image below shows the company generated about C$9.4M in operating cash flow, but after deducting the C$1.5M contribution from working capital changes and the C$0.2M in lease payments, the adjusted operating cash flow was C$7.7M. The total capex and capitalized exploration cash outflow was C$4.5M, resulting in a net free cash flow of C$3.2M or C$0.032 per share.

Hemisphere Investor Relations

While this still fully covered the quarterly dividend, the free cash flow result was substantially lower than the net income. This was predominantly caused by the high capex and capitalized exploration which came in at more than twice the depreciation expenses. This also was higher than the normalized capex as Hemisphere is still guiding for a full-year capex of C$14M, representing C$3.5M per quarter. And even if you would use C$4M per quarter, the free cash flow result would obviously still be strong.

Now we have established how strong the results were in the second quarter, let’s have a look at what we may expect from the third quarter.

Oil prices continued to increase and it’s important to note the heavy oil price is increasing as well. The WCS price was C$83 in July, C$87 in August and will likely exceed C$95 for September. This means we can expect the average realized price for the quarter to exceed C$85 per barrel and it may even come in closer to C$90/barrel.

Assuming C$88/barrel as average realized price for the quarter, Hemisphere’s revenue per barrel will increased by approximately C$14 compared to the second quarter. And after deducting the royalties and tax payments, the net operating cash flow should increase by roughly C$7/barrel. At a production rate of 3,000 boe/day, this represents an additional net free cash flow of C$21,000/day or C$1.8M for the quarter.

A special dividend is underway

Which means the Q3 free cash flow result may very well come in at C$5.5M in the third quarter (using a normalized capex of C$4M) and that would represent about C$0.055 per share.

The company’s dividend policy calls for a payout ratio of 30% of the adjusted funds flow. At an average heavy oil price of C$88/barrel, the annualized adjusted funds flow would be approximately C$38M which means the annual dividend should be roughly C$0.12 per share. This is subject to quality adjustment factor per barrel of oil.

That also was what I was expecting in the previous article. But earlier this week, Hemisphere Energy announced it will pay a special dividend of C$0.03 per share in November. Combined with the normal quarterly dividends of C$0.025 per quarter, the full-year dividend will come in at C$0.13.

Investment thesis

And this reconfirms Hemisphere’s status as a small-cap oil company with dividend potential. As of the end of June, the company had no gross debt and a net cash position of approximately C$4M, so it makes sense the company continues to focus on keeping its shareholders happy. I’m looking forward to seeing the Q3 results and I wouldn’t be surprised to see an adjusted operating cash flow of C$10M and a normalized free cash flow result of C$6M. For the time being, I’m slightly more conservative and I will use an anticipated free cash flow of C$5.5M based on an average WCS price of around C$88/barrel. But keep in mind the current WCS oil price is now more than 10% higher at roughly C$100/barrel.

I have a long position in Hemisphere, and although I’m mainly focusing on capital gains, I’m very happy with the generous dividend payments.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here