It’s been a while since I last visited the Vanguard Real Estate Index Fund ETF Shares (NYSEARCA:VNQ) back in February with a ‘Buy’ rating, and it hasn’t been one of my best performers, to say the least. Considering the regional banking crisis and interest rate hikes since then, it’s no wonder that investors have shied away from income vehicles like REITs.

All this negativity has resulted in VNQ now trading a near its lowest point over the past 5 years excluding the early 2020 timeframe, reflecting the below average valuations for most of its holdings. In this article, I discuss why income investors who like diversification may want to consider layering into VNQ at its currently discounted price, so let’s get started!

VNQ ETF (Seeking Alpha)

Why VNQ?

VNQ isn’t a stock that’s going to make anyone rich overnight, but investors would rather hold it for its quality diversification and income from hard, tangible assets. Unlike technology stocks, real estate is boring and presumably provides for slow by steady growth. This makes them out of favor with investors in an environment where 10-year Treasury bonds yield well over 4%.

Institutional investors make up the largest owners (over retail investors) in most companies with market cap over $1 billion, and are clearly favoring tech stocks. This is according to a recent Bank of America (BAC) survey of 247 fund managers who are piling out of REITs with “capitulation” not seen since the collapse of Lehman Brothers during the Great Financial Crisis of 2008.

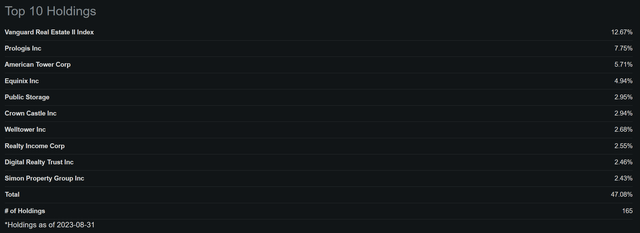

Nonetheless, not all REITs are created equal, and VNQ counts a number of high quality players among its top holdings. This includes REITs that are leaders in their respective industries that command pricing power. As shown below, industrial giant Prologis (PLD), cell tower leader American Tower (AMT), data center giant Equinix (EQIX), and self-storage leader Public Storage (PSA) are among VNQ’s top holdings, encompassing just over one-fifth of the portfolio total.

VNQ Top Holdings (Seeking Alpha)

As one can imagine, these giants command pricing power due to their established asset base in prime locations and carry significant operating leverage due to their significant economies of scale. That’s because they are able to spread operating costs over a wider asset base.

For example, Public Storage, one of the largest self-storage REITs on the market today, sitting just behind Extra Space Storage (EXR) after the latter acquired Life Storage this year. PSA achieved a 73% operating margin (with depreciation addback) over the trailing 12 months, surpassing the 66% for smaller peer CubeSmart (CUBE) over the same timeframe.

Additionally, VNQ’s top holdings such as Prologis and American Tower belong to growth industries, achieving inflation beating growth metrics. For example, PLD has seen a 3-year AFFO CAGR of 12.9% and a 5-year dividend CAGR of 12.6% while AMT has a 3-year AFFO CAGR of 8.6% and a 5-year dividend CAGR of 16.4%.

Risks to VNQ include, of course, the fact that REITs carry leverage in order to boost growth. While that may be a fine model in a ZIRP (zero interest rate policy) environment, higher interest rates can put pressure on both external growth due to higher cost of funding as well as bottom line growth due to higher interest expenses. As such, I wouldn’t expect names such as PLD and AMT to grow their top and bottom-lines by as much this year and next compared to the prior 3 years.

Nonetheless, VNQ’s top holdings all carry strong balance sheets with investment grade credit ratings, which should provide some buffer against refinancing risk. Additionally, as I noted in a recent piece about another one of VNQ’s top holdings, Welltower (WELL), higher interest rates may actually work to its long-term advantage, as this prevents higher leveraged private market players from taking on loans to do speculative build and create new supply competition.

With construction starts in WELL’s seniors housing industry being down 80% from its peak several years ago, WELL is in a far better position to succeed due to less competition for both labor and senior living. As such, while REITs in VNQ currently see headwinds from higher rates, they are well-positioned to succeed over the longer term due to less competition. At the same time, these REITs can also offset inflation with price increases, as in the case with WELL and others due to their inherent pricing power.

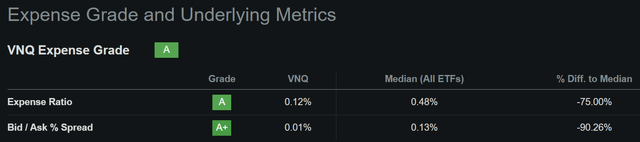

Meanwhile, VNQ is also investor friendly with an ‘A’ grade for expenses, charging just a 0.12% expense ratio, which sits well under the 0.48% median across the ETF universe. Having a low expense ratio means a lot over time, especially considering that higher expenses can be significant when compounded over time.

Seeking Alpha

Lastly, I see value in VNQ’s current price of $75.44 with 4.8% dividend yield makes up for the near-term risks to REITs. At this rate, VNQ would only need a 5.2% long-term dividend CAGR to produce the same 10% long-term RoR as that of the S&P 500 (SPY), all while providing a far higher yield. For reference, VNQ produced a 6.7% dividend CAGR over the past 3 years. As such, VNQ may be well-suited for investors looking for value and yield.

Investor Takeaway

In summary, VNQ offers income investors high-quality and diversified exposure to REITs with solid top holdings that should help provide for above market average dividend yields over time. While REITs face near-term headwinds due to higher rates, their institutional grade balance sheets and pricing power should allow them to succeed over the longer term. With its low expenses and current discount, VNQ is a strong choice for investors looking for both value, diversification and income.

Read the full article here