Investment Thesis

Rigetti Computing (NASDAQ:RGTI) has a mighty compelling mission statement that Rigetti puts forth in large capital letters on their SEC filings,

OUR MISSION IS TO BUILD THE WORLD’S MOST POWERFUL COMPUTERS TO HELP SOLVE HUMANITY’S MOST IMPORTANT AND PRESSING PROBLEMS.

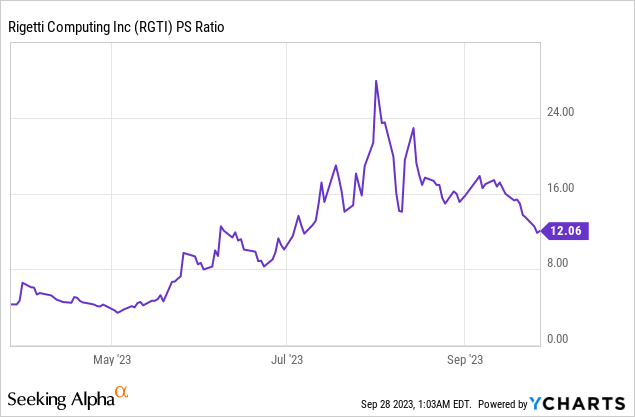

But beyond its strong use of words, the business is far from viable, at least for now. Moreover, I find that paying 12x forward sales for Rigetti to be simply too high a multiple.

Consequently, I’m staying firmly on the sidelines here.

Rigetti Computing’s Near-Term Prospects

Rigetti Computing has tremendous aspiration, its mission is to create one of the world’s most powerful computers to tackle humanity’s most critical challenges. They specialize in building and operating quantum computers, which leverage the principles of quantum mechanics to process information in a new and powerful way compared to classical computing. These quantum computers have the potential to solve complex problems at unparalleled speeds, making them a transformative technology.

Rigetti’s approach includes developing multi-chip quantum processors that are the building blocks for scalable quantum computing systems. They have their own wafer fabrication facility, Fab-1, dedicated to prototyping and producing these quantum processors. By owning the entire production process and employing a full-stack development approach, Rigetti aims to create commercially valuable quantum computers efficiently and with a lower risk.

Furthermore, Rigetti offers quantum computing services to end-users through their Rigetti QCS platform and cloud service providers. They have formed strategic partnerships and customer relationships with prominent organizations, including Amazon Web Services (AMZN), Microsoft (MSFT), and government agencies like DARPA and DOE. Rigetti’s goal is to advance quantum computing through various phases, from Emerging Quantum Advantage to Large-Scale Fault Tolerant Quantum Computing, which holds vast potential for applications in fields like drug discovery, materials science, and beyond.

Rigetti Computing’s near-term prospects appear attractive as they remain on track to achieve significant milestones with their fourth-generation quantum system. The successful launch of the Ankaa-1 system internally and their collaboration with Riverlane to improve error correction techniques demonstrate their commitment to advancing quantum computing capabilities. Notably, Rigetti plans to make this innovative quantum system accessible to the general public in the upcoming fourth quarter, indicating their confidence in its readiness and market potential.

Moreover, their recent achievement of completing the first QPU sale to a national lab signifies a growing interest in their quantum processors. While the majority of their revenue still stems from research contracts, the introduction of QPU sales could diversify their revenue streams. With a focus on enhancing the performance of its quantum systems and a roadmap that includes scaling up its qubit count from 84 qubits to 168, Rigetti is eager to make further strides in the quantum computing industry, positioning itself for potential growth and technological advancements in the near term.

Undoubtedly, Rigetti has a compelling narrative. But now let’s dig into its financials.

Revenue Growth Rates Too Unpredictable

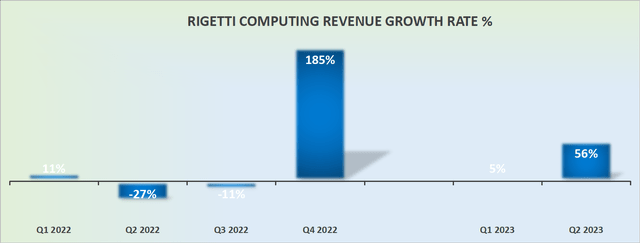

RGTI revenue growth rates

Personally, I find Rigetti’s revenues too unpredictable. They may occasionally land a large deal, but counting on those large deals to forecast its growth rates is simply too challenging a task, to be frank.

For instance, back in Q4 2022, Rigetti’s revenues stood at $6.1 million, and as of Q2 2023, it’s roughly half of that at $3.3 million. Furthermore, putting aside the blockbuster Q4 2022 result, Rigetti’s revenues have ranged between $2 and $3 million for practically 2 years. This is not a rapidly growing business.

What’s more, there’s so little visibility into its revenue growth rates that Rigetti itself fails to provide its shareholders with guidance for the upcoming quarter, not to mention the whole year.

And those considerations surface even before we consider its financial position.

Balance Sheet Will Require More Cash

Followers of my work will know that I recommend always spending 5 minutes on a company’s balance sheet. 5 minutes is not a long time, but those 5 minutes can be worth their weight in gold if it keeps an investor from putting themselves in an uncomfortable position.

Because as an investor, the last thing you want is to have to live by the market’s whims. By this, I mean that if the business needs to raise capital, you want the business not to need capital when financial conditions are not restrictive or interest rates are high, for example.

Looking out to the end of 2023, Rigetti believes it will end with around $70 million of cash. And on top of that, once we factor in its debt profile, Rigetti’s net cash position drops to around $45 million of net cash.

And then, we have to keep in mind that Rigetti burns through about $15 million of free cash flow per quarter. This is a rough estimate, likely to change substantially from quarter to quarter, but it puts us in the right ballpark.

Meaning that to get around $3 million in revenues, the business has to burn through nearly 5 times as much free cash flow. Put another way, for every $1 of revenues the business makes it uses around $4 to $5 of cash. That’s simply not sustainable.

Given this cash burn rate, Rigetti stated on the earnings call,

based on our current operating plan, we anticipate that Rigetti will need to raise additional funding by late 2024 or early 2025 to continue its research and development efforts and achieve its business objectives.

Accordingly, the company is openly asserting that the business even in late 2024 isn’t likely to be profitable, but instead will need to raise more cash to stay afloat.

Now, given everything we’ve discussed, does it make sense to pay 12x forward sales for this business? I’m up for paying for growth stories, but it must make reasonable sense. And from my perspective, I find it challenging to believe that investors will be rewarded for investing in this stock.

The Bottom Line

As I assess Rigetti Computing’s near-term prospects, a sense of uncertainty looms. While their mission to create powerful quantum computers for critical challenges is inspiring, their current viability remains unclear. The 12x forward sales multiple raises valuation concerns amid these uncertainties.

The unpredictability of revenue growth rates, fluctuations from large deals, and a lack of revenue guidance add to the uncertainty. Rigetti’s balance sheet reveals cash flow sustainability issues, with heavy cash burn and a likely need for additional funding by late 2024 or early 2025. Given these challenges, paying a 12x forward sales multiple seems unjustified, prompting a cautious stance and my decision to stay on the sidelines regarding this stock.

Read the full article here