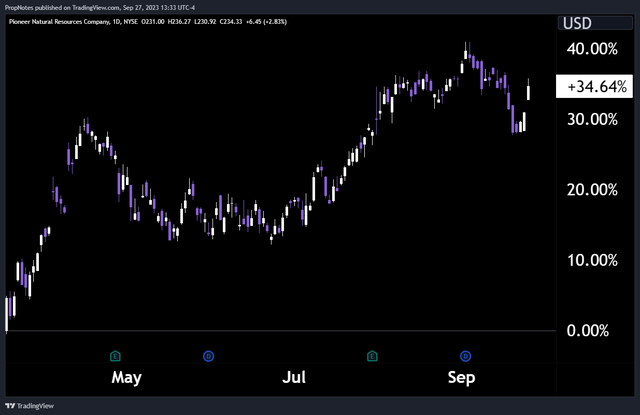

Pioneer Natural Resources (NYSE:PXD) has been on a tear lately.

Up more than 34% since mid-March, the mid-sized Oil & Gas production company has surged in price on the back of two impressive earnings reports, in addition to a resurgent underlying oil market:

TradingView

While we like the company and believe that management has done a good job steering the ship, the stock has gotten more expensive relative to itself historically, as well as against market peers.

That’s why, at the present moment, we think that selling put options on PXD stock is the most optimal way to trade this company.

Selling puts allows investors to generate immediate income and have lower-volatility exposure to the stock, while retaining the opportunity to scoop up shares if they dip in price too precipitously.

Today, we’ll take a deeper look into PXD’s financials, prospects, and valuation, in order to explain why we ultimately think selling put options is the best win-win opportunity for investors looking to get their feet wet in this great company.

Let’s dive in.

Past Results

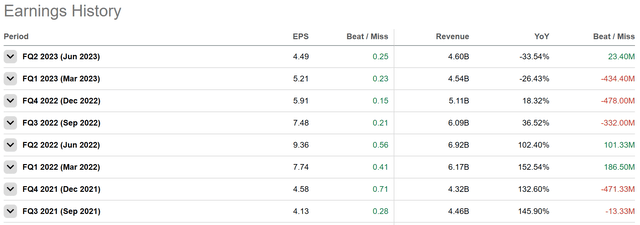

As always, let’s begin with the company’s Financial Results.

As we just mentioned, PXD recently reported a few solid quarters of earnings.

Revenue fell earlier this year as 2022’s hot oil market has cooled, but the company has continued to crank out estimate-beating EPS for the last several quarters:

Seeking Alpha

In Q1, PXD produced $5.21 in EPS vs. an estimate of $4.98.

In Q2, they beat again, with reporting EPS of 4.49; 25 cents above estimates.

Interestingly, this performance came at a time of broader market uncertainty.

In short, PXD outperformed in what was ostensibly a poor market for oil and its derivatives; here’s what PXD management themselves had to say about their end market opportunity for the first half of 2023:

Recent data from China points to a fragile economy as key indicators, such as consumer spending, have weakened, and youth-unemployment recently hit record highs.

China remains the world’s second largest economy and represents a key component of oil demand. These uncertainties led OPEC to reduce its oil demand outlook, which led to multiple cuts to its production quotas.

As a result of the current global supply and demand uncertainties, average NYMEX oil and NYMEX gas prices for the three months ended June 30, 2023 were $73.78 per Bbl and $2.09 per Mcf, respectively, as compared to $108.41 per Bbl and $6.76 per Mcf, respectively, for the same period in 2022.

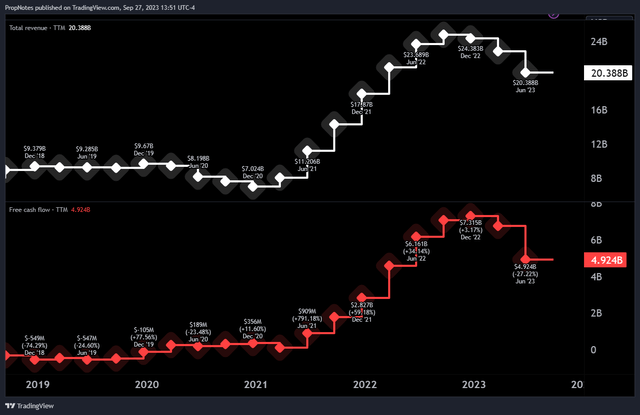

While the company has outperformed expectations, which is a sign of solid management, cash conversion, and drilling efficiency, the company hasn’t been immune to the slowdown.

Zooming out, nominally, PXD’s TTM revenue has fallen, and Q2 YoY revenue was down more than 33%. This dip has impacted cash flow, causing a noticeable dip in TTM FCF profitability:

TradingView

While the outperformance is nice, there’s only so many levers an oil company can pull when the market is fighting you.

The Outlook

Time for some good news.

Since PXD’s last report, oil has picked back up in price, on the back of increased demand and continued supply snarls from the Ukraine/Russia situation.

Since the end of June, the liquid commodity has rallied more than 37%:

TradingView

Record demand and supply issues have led to falling oil inventories, which bodes well for producers.

Wednesday, the Energy Information Administration had the following to say:

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 2.2 million barrels from the previous week. At 416.3 million barrels, U.S. crude oil inventories are about 4% below the five year average for this time of year.

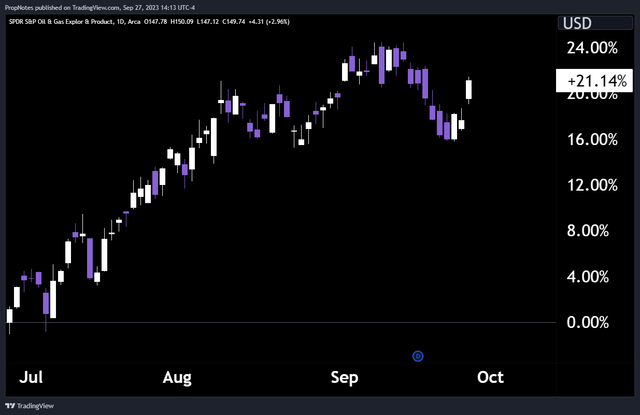

This ongoing supply, demand, and inventory situation has led to a surge in oil stocks across the board, PXD included, as the outlook of “higher for longer” should lead to continued opportunities, especially for larger, competent drillers:

XOP (TradingView)

However, this has caused us some concern around the valuation.

The Valuation

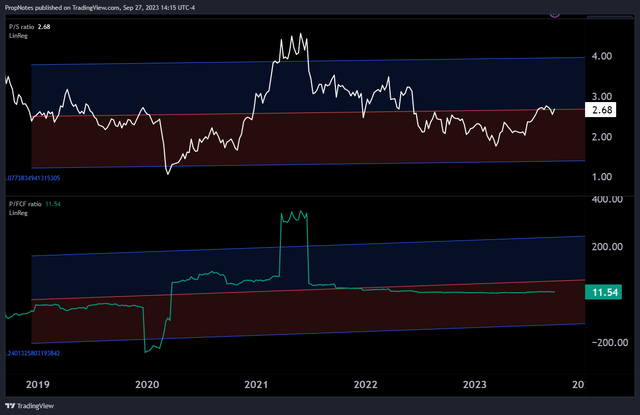

Nominally, many would call PXD ‘cheap’. The company trades at 2.6x Revenue, 11x free cash flow, and sports net margins in the mid 20%’s:

TradingView

However, as you can see from the graph above, PXD has gotten more expensive as of late. The company’s sales multiple has expanded above the midpoint of the linear regression, and FCF is beginning to look uncompetitive with other oil peers, especially on the crucial FCF multiple:

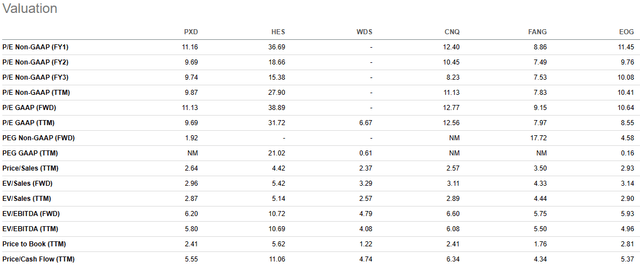

Seeking Alpha

Trading at 5.5x CF, the company is no longer a value gem; it’s in the middle of the pack.

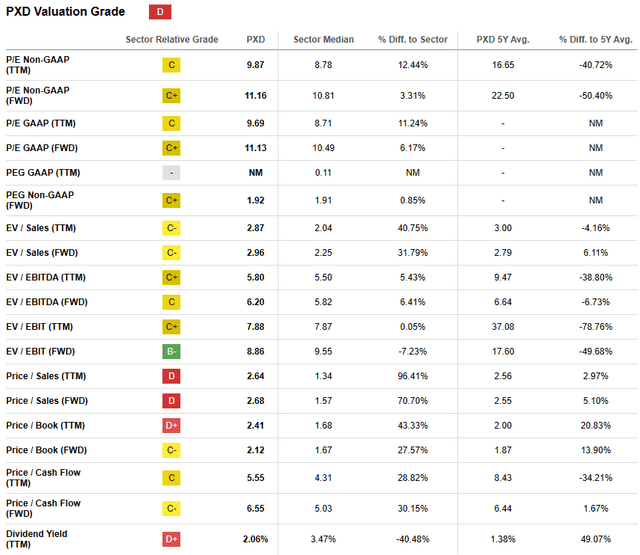

This is something that Seeking Alpha’s Quant Rating system agrees with, as PXD is currently rated a ‘D’:

TradingView

Thus, when taken together, it’s clear that PXD is a well-run company with significant opportunities ahead of it, as oil continues to rally and business conditions improve. However, the stock isn’t a compelling value, and the dividend, at 2.06%, is quite low.

What’s the best way to trade it?

The Trade

In our view, the best way to take advantage of PXD is by using the stock as a solid underlying platform for selling put options.

In case you’re unaware, when you sell a put option, you’re agreeing to buy the stock at a given price (the strike price), if the stock price finishes under the strike price.

In return for the obligation of doing so, you earn a cash premium.

Think of it like selling insurance on a stock – the stock goes up, you keep the cash. The stock goes sideways, you keep the cash. The stock goes down precipitously, you get to buy up shares at a significantly lower breakeven point vs. today’s market.

This solves our income dilemma, and our valuation dilemma, as a lower entry point would likely lead to a more attractive margin of safety.

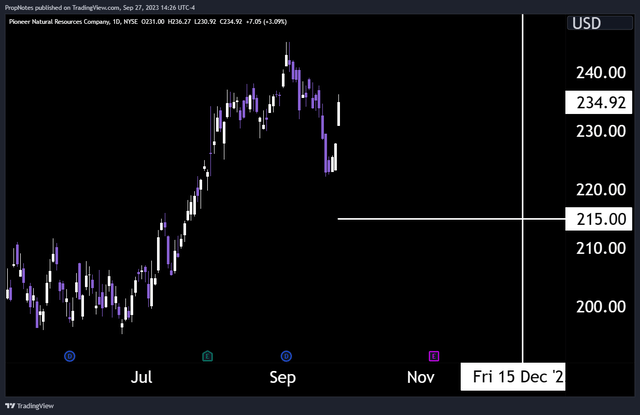

As a result, we like the December 15th, $215 strike put options:

TradingView

They’re currently trading at $4.40, which represents a cash-on-cash return of 2.09%, or 9.6% annualized.

With a 78% probability of worthlessness by option expiry, they seem like a great win-win way to play the stock.

Risks

As always, there are some risks associated with a trade like this – chief among them the fact that the company is expected to report earnings on November 7th.

This is before our option expires, and even if the stock does end up beating expectations, you never know how the market will react to those numbers.

This risk profile is no different than simply owning the shares outright, but it’s important to mention that put sellers, in some cases, may be forced to buy PXD stock above market depending on how the next 74 days go.

Summary

All in all, we like the outlook for PXD, but we’re not in love with the company’s capital return policies or the mixed/expensive valuation.

Thus, we think selling put options is the best win-win to play the stock – either a solid cash premium earned, or a much better entry point into this medium term winner.

If you enjoyed this article, be sure to share it with a friend who may also appreciate it.

Cheers!

Read the full article here