When somebody mentions “yield curve inversion” almost everybody responds in a Pavlovian way with “recession”! And given the bad performance of equities in (some of the) previous recessions, the conclusion is often: “sell your equities”. But despite the fact we have a yield curve inversion for a long time, we still have no recession and equities are performing well. Some equities are performing better than others. Is this a coincidence they are performing so well despite the yield curve inversion, or not?

Rising interest costs

Banks make money by “borrowing short and lending long”. Banks borrow from depositors at lower short-term borrowing rates while lending at higher longer-term rates. Normally, when the yield curve is upward sloping, this allows banks to pocket nice profits. And the steeper the yield curve, the juicier the bank profits. The biggest risk for these bank profits is of course a yield curve inversion: short term rates are higher than long term rates.

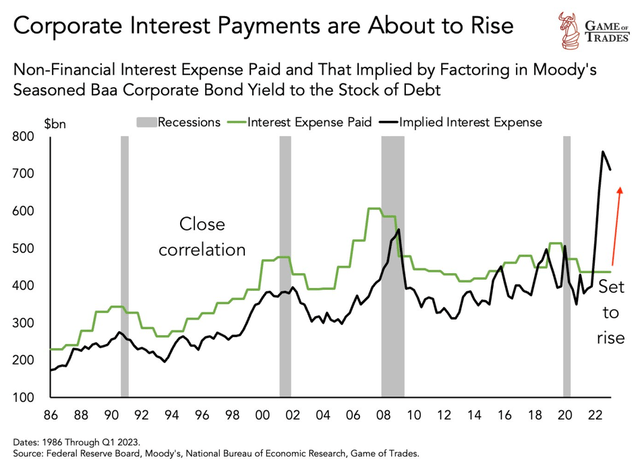

The past two years interest rates have risen and due to the fact that short term interest rates have risen more than long term rates, we have a yield curve inversion. Some companies are more exposed to short term rates, while others have more exposure to long term rates. But because both short and long term rates have increased, we can expect that interest payments have increased for all companies.

Figure 1: Corporate Interest Payments (Game of Trades)

But this is not what we see in the data. To the contrary, interest payments decreased!

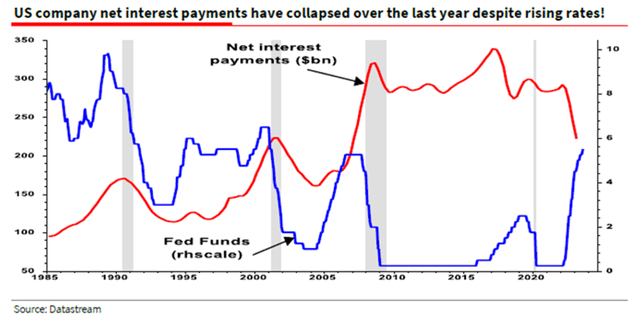

Figure 2: Interest Payments (SG)

How is this possible?

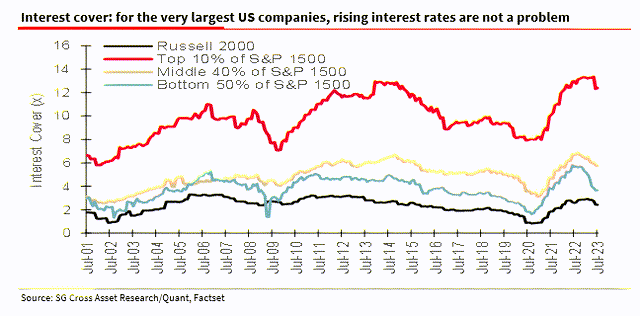

Rising rates have a bigger impact on smaller companies who use more floating rate debt. Bigger companies use more fixed rate long term debt and have locked in lower rates before rates started rising.

Figure 3: Interest Cover (SG)

Those bigger companies often generate lots of free cash flow which they can invest now at higher short term rates. They actually do the opposite of the banks: “borrowing long and lending short”. This is a winning strategy when there is a yield curve inversion.

Cash rich companies

So, when there is a yield curve inversion, we should look for cash rich companies.

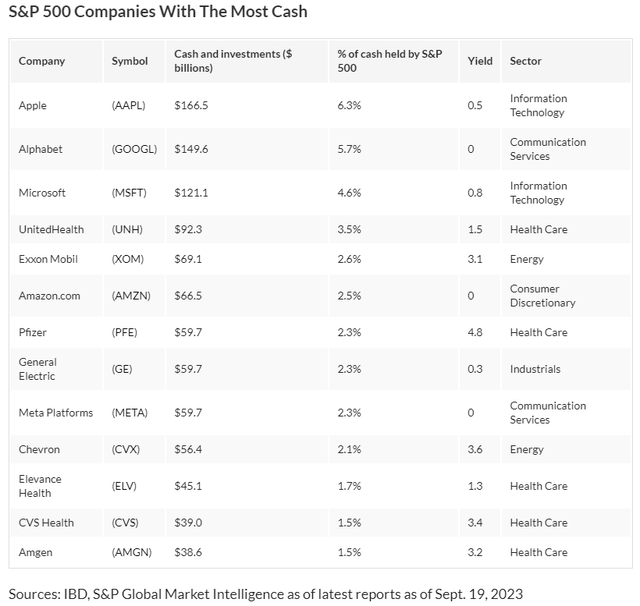

Investor’s Business Daily recently published a list with the most cash rich companies.

Figure 4: Cash rich companies (Investor’s Business Daily)

The list includes the usual suspects from the Technology and Communication Services sectors like Amazon (AMZN), Alphabet (GOOGL), Meta (META), Apple (AAPL) and, Microsoft (MSFT). But maybe a bit surprising also stocks from the Healthcare and Energy sectors are part of the most cash rich companies list.

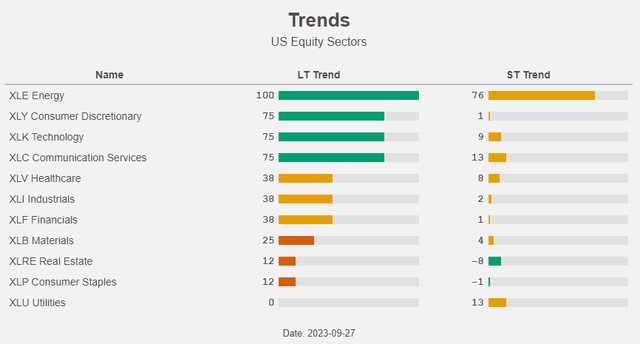

With the exception of the Healthcare sector, all the mentioned sectors are in a long term uptrend.

Figure 5: Trends (Radar Insights)

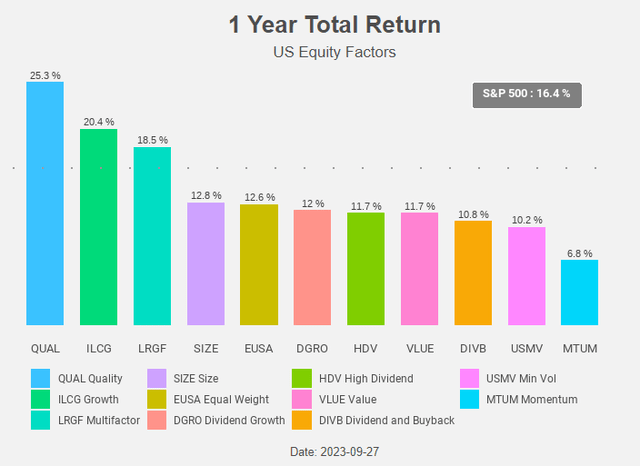

Which ETF invests a lot in those quite diverse sectors? Companies with a lot of cash and hence a strong balance sheet point to quality ETFs like the iShares MSCI USA Quality Factor ETF (QUAL). Quality is the best performing equity factor.

Figure 6: Total return chart (Radar Insights)

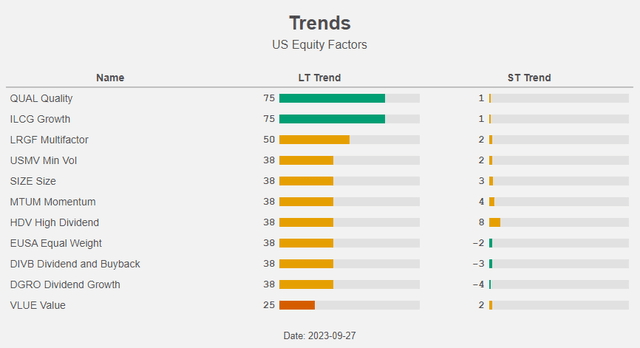

Quality and Growth are the only equity factors that are still in a long term uptrend (and are at the same time oversold after the recent share price weakness).

Figure 7: Trends (Radar Insights)

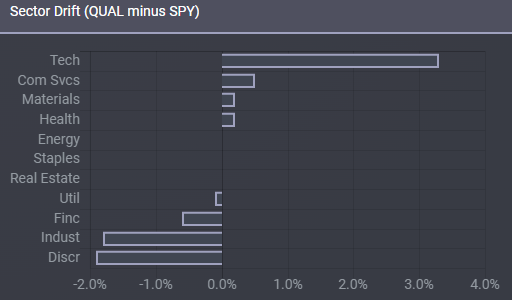

Compared to the S&P 500 QUAL is a bit overweight Technology, but that’s about it.

Figure 8: Sector drift (ETF Research Center)

Can we do better?

Wahed FTSE USA Shariah ETF

Another quality ETF we’ve written about is the Wahed FTSE USA Shariah ETF (NASDAQ:HLAL). HLAL invests only in so-called Shariah-compliant stocks which have characteristics which are consistent with Islamic principles as interpreted by subject-matter experts.

On top of that, only those companies that pass the following financial ratios are considered Shariah-compliant:

- Debt is less than one-third of total assets;

- Cash and interest-bearing items are less than one-third of total assets;

- Accounts receivable and cash are less than 50% of total assets; and

- Total interest and non-compliant activities income should not exceed 5% of total revenue.

It goes without saying that the HLAL-portfolio has a strong quality-bias.

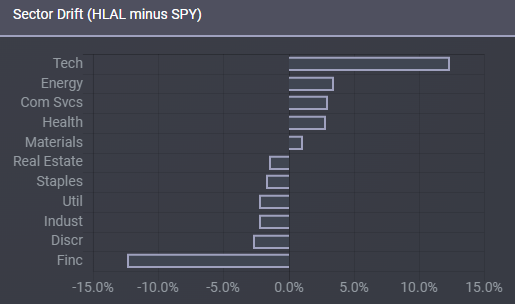

And indeed, HLAL is overweight the right sectors and this overweighting is also more outspoken compared to QUAL.

Figure 9: Sector drift (ETF Research Center)

Finance stocks are not shariah-compliant and hence there’s absolutely no Finance-exposure. As a result there is no exposure to stocks that suffer when there is a yield curve inversion.

The exclusion of financials helped the performance of HLAL during the regional bank weakness in March. The fund managers view “speculative activities by banks to be cyclically recurring events” and believe the exclusion of financials (and highly leveraged companies) will also be a long-term driver of outperformance in the future.

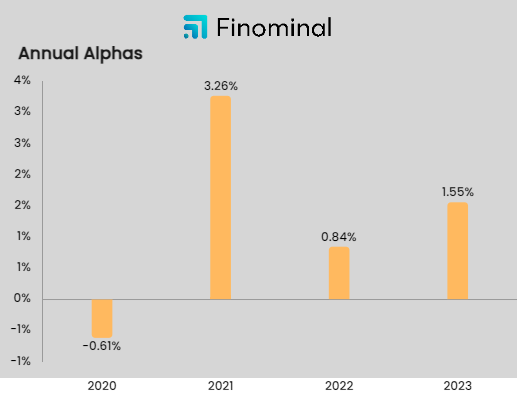

The past years HLAL consistently delivered alpha.

Figure 10: HLAL Alpha creation (Finominal)

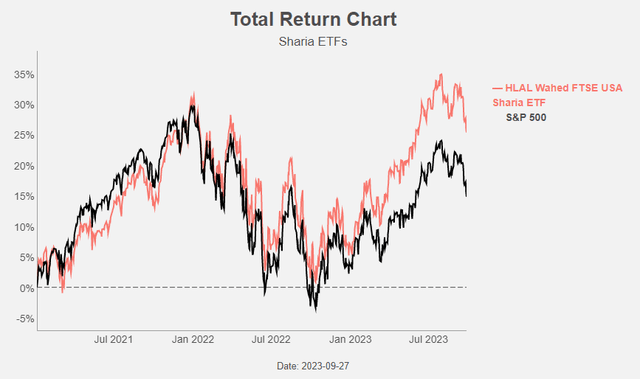

It comes as no surprise that HLAL is outperforming the (well performing) S&P 500.

Figure 11: Total return chart (Radar Insights)

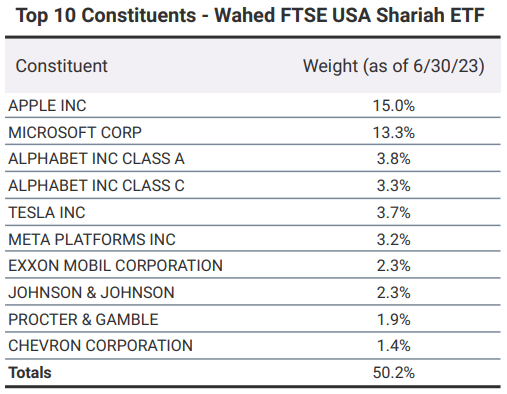

HLAL’s portfolio is market cap weighted. This results in high weights for Apple and Microsoft .

Figure 12: Top 10 holdings (Wahed)

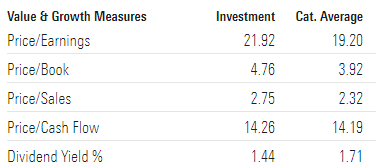

Wahed itself doesn’t offer much valuation info about HLAL. The valuation of HLAL is in line with those of the “Large Blend” Morningstar category.

Figure 13: Valuation (Morningstar)

An investment is often overbought while it is in an uptrend and vice versa, often oversold in a downtrend. Both QUAL and HLAL are in a long term uptrend and at the same time oversold. This doesn’t happen often, and we advise to profit from this rare occasion: buy the dip!

Figure 14: Trends (Radar Insights)

Conclusion

The past two years interest rates have risen and due to the fact that short term interest rates have risen more than long term rates, we have a yield curve inversion. This is good news for the big caps who generate a lot of free cash flow and have locked in lower fixed rates before interest rates started rising. Those cash rich companies are able to “borrow long and lend short” and to profit from the yield curve inversion.

The Wahed FTSE USA Shariah ETF is overweight the sectors with the most cash rich companies. The recent share price weakness offers an excellent buying opportunity for this quality ETF.

Read the full article here