Co-authored with “Hidden Opportunities”

Have you ever reflected on those handful of expenditures that stand out as the absolute best investments you’ve made in your lifetime? It could be a book that gave you a whole new outlook, a trip that left an indelible mark on your soul, or a course or conference that ignited new passions.

These tangible, intellectual, experiential, or even digital purchases enrich our present and often map the course for our future. They can even be stepping stones that lead us to the next great chapter of our lives.

Such investments also come as tradable securities on the stock exchange. In every annual shareholder letter, Warren Buffett talks about the crown jewels of Berkshire Hathaway’s portfolio, his prized long-term investments in companies like Coca-Cola (KO), American Express (AXP), GEICO, etc. that keep generating billions in dividend payments every year.

“The cash dividend we received from Coke in 1994 was $75 million. By 2022, the dividend had increased to $704 million. Growth occurred every year, just as certain as birthdays. All Charlie and I were required to do was cash Coke’s quarterly dividend checks.” – Warren Buffett

Ideally, we would like to hold our investments forever, and it would help if they paid us handsomely to do that. Today, we will discuss two cash-producing picks that make excellent additions to your long-term portfolio due to the predictability and safety of their yields.

Let’s dive in.

Pick #1: AFG Baby Bonds – Up To 6.5% Yields

The history of American Finance Group, Inc. (AFG) goes back to its humble beginnings in 1872 as the Great American Insurance Company. Today, AFG operates over 120 locations worldwide, employs 7,500 employees, and is a leader in specialty property and casualty insurance (P&C). Source

Investor Presentation

AFG’s underwriting standards and diligence are clearly seen from the fact that their overall “combined ratio” was under 94% for ten consecutive years. The combined ratio is the sum of incurred losses and expenses from policyholder claims divided by the earned premiums from the policies. Hence, a metric over 100% means an insurance firm is paying out more in claims than collecting through premiums. For FY 2023, AFG has guided the specialty P&C overall combined ratio between 89-91%, indicative of solid underwriting profitability. AFG maintains an excellent balance sheet, rated A+/A1 by leading credit agencies.

AFG’s board recently approved another increase in the regular annual dividend to $2.84 from $2.52/share, a 12.7% YoY increase. AFG has no debt maturities until 2030, and the company has no borrowings under its $450 million credit line. The company ended Q2 with $551 million in cash and short-term fixed maturities, providing significant liquidity to AFG to take advantage of market disruption events.

Dividends are not the only form of capital return pursued by AFG. The company has been actively repurchasing shares, with ~67 million in share purchases in 1H 2023. In addition, the company also purchased $4 million of its Senior Notes during Q2. AFG can purchase another 7 million shares remaining in its current repurchase plan. The family of Carl Lindner, Jr., company executives, and the institutional retirement plan for staff owns 24% of the shares indicating strong insider alignment towards shareholder interests.

AFG has four publicly traded subordinated notes – baby bonds, trading at attractive discounts amidst the Fed’s hawkish monetary policy. Given AFG’s financial strength, operational excellence, and shareholder-oriented capital allocation priorities, the baby bonds present CD-beating “Sleep Well At Night” securities. All four subordinated notes carry investment grade “Baa2” ratings and come right below the company’s senior notes in the capital stack.

-

5.875% Subordinated Debentures due March 30, 2059 (AFGB)

-

5.125% Subordinated Debentures due December 15, 2059 (AFGC)

-

5.625% Subordinated Debentures due June 1, 2060 (AFGD)

-

4.50% Subordinated Debentures due September 15, 2060 (AFGE)

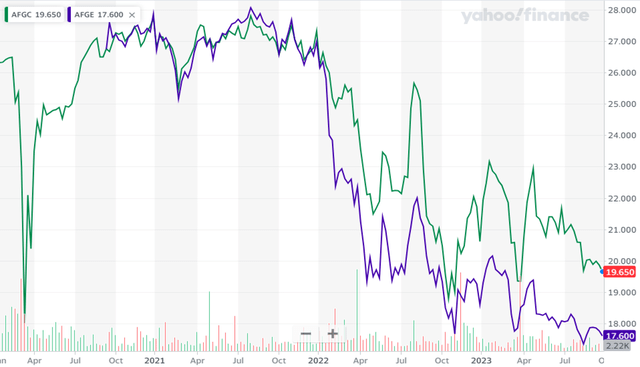

Both AFGE and AFGC present attractive yields with significant capital upside to par value. AFGE yields 6.4% and offers a 42% upside to par, whereas AFGC pays 6.5% and offers a 27% upside. Source

Yahoo Finance

AFG is a well-managed machine to keep chugging along those interest payments for the foreseeable future. Buying either AFGC or AFGE at these low prices will enable a healthy stream of reliable income and eventual capital upside as rates move lower. In the alternative, investors could also choose to hold this through maturity, which would be “forever” in a sense due to the maturity date being ~30 years away.

Pick #2: RLJ Preferred – Yield 8.2%

During the Labor Day weekend, domestic bookings for flights, hotels, rental cars, and cruises were up 4% YoY, while international bookings were substantially higher by 44%. With over 14 million passengers screened around the long weekend, travel numbers have surpassed the pre-pandemic period, indicating the importance of travel and leisure among the American public.

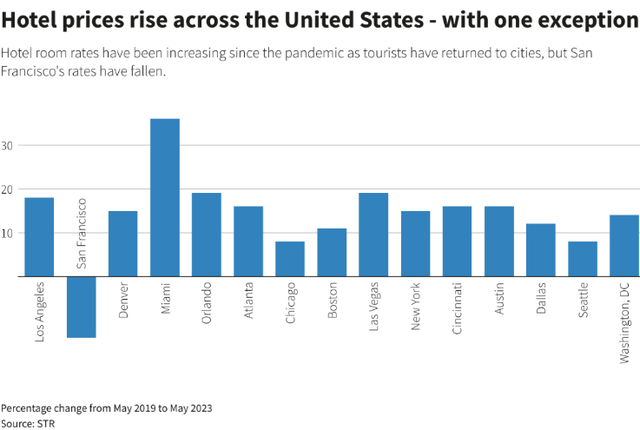

Sunbelt states in the U.S. are leading the post-pandemic recovery in the hotel industry. Travel volume and demand remain strong even though several cities have seen substantial hotel price increases in 2022.

Reuters

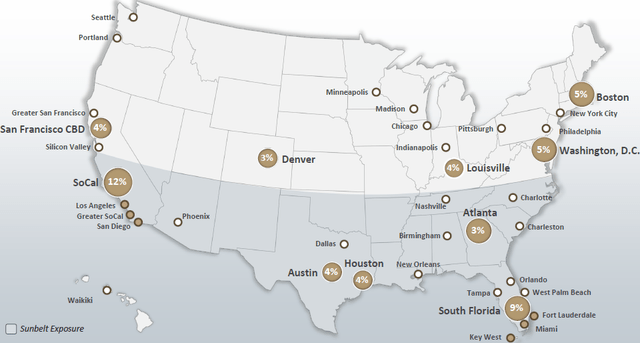

RLJ Lodging Trust (RLJ) is a hotel REIT with ~51% EBITDA exposure to sunbelt states and 2/3rd of its property portfolio in urban centers. The persistence of leisure travel and the strong rebound of business travel has this company recovering strongly and delivering value to shareholders along the way. Source

July 2023 Investor Presentation

RLJ reported business travel reaching 71% of 2019 levels while achieving a sequential improvement. Also, the REIT’s urban market concentration has resulted in overall RevPAR growth (Revenue per Available Room) exceeding the industry metrics for the second straight quarter. Q2 2023 RevPAR increased 4.5% YoY, reaching 96% of the pre-pandemic levels, marking a new high. These were achieved despite poor weather in Florida and the Hollywood strikes in California.

RLJ’s board approved a $250 million share repurchase program (for one year), which lets the company take advantage of depressed prices amidst the market volatility. During Q2, the company repurchased 2.5 million shares for $25.5 million. YTD 2023, RLJ repurchased 5.3 million shares for $54.2 million at an average price of $10.22 per share (this includes $1.3 million repurchased in Q3 as of the conference call).

And, there is more. RLJ’s strong FCF profile made management confident to announce a second quarterly dividend raise for the year. The company’s Q3 dividend of $0.10/share reflects a 25% increase sequentially.

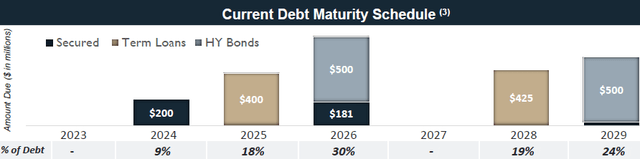

The company’s growing FCF and strong balance sheet adequately support the new dividend policy. 81 out of 96 hotels in RLJ’s portfolio are unencumbered by debt. The REIT has 93% of its debt at fixed rates or hedged. The company’s weighted average interest rate at the end of Q2 was an enviable 3.98%. RLJ maintains a staggered debt schedule with ample liquidity to meet its upcoming maturities in 2024. The REIT ended Q2 with $477 million of unrestricted cash and $600 million of availability on its corporate revolver to pursue buybacks, issue dividends, and execute portfolio enhancement projects. Source

August 2023 Investor Presentation

With that, we will turn to RLJ’s convertible preferred security, which offers attractive long-term income prospects. A growing common dividend provides an additional layer of safety to the investors of the cumulative preferred.

-

RLJ Lodging Trust, $1.95 Series A, Cumulative Convertible Perpetual Preferred Shares (RLJ.PR.A)

RLJ cannot redeem the RLJ-A preferred, but can force conversion to common stock only if RLJ trades at or above $89.09 for 20 out of 30 trading days. As such, for the preferred to become convertible, the common stock has to experience a staggering 780% upside, making it quite an improbable situation, or what is known as a “busted convertible”.

During 1H 2023, RLJ’s $196 million adj. EBITDA provided adequate coverage for the $39.9 million interest expense, $12.5 million preferred dividend payments, and $25 million common dividends.

Being convertible, RLJ-A cannot be called and has no par value. The price of this preferred fluctuates based on the interest rate environment and on the amount Mr. Market is willing to pay for the $1.95 annual yield. At current prices, this security presents an attractive 8.2% annual yield. Interest rates won’t remain high forever. We are closer to the peak than ever, and these yield levels in this quality firm won’t last.

Capital projects, share buybacks, dividend raises – RLJ has it all going for its shareholders. The 8.2% yielding cumulative preferred presents safer perpetual income prospects for long-term investors from an industry that is increasingly appealing to the priorities and values of younger generations.

Conclusion

In the investing world, some securities can be bought and held forever, and these can quietly deliver profound value for a very long time. I am not talking about swinging for the fences with some speculative investment that may or may not be the next ten-bagger. This report discusses two picks that will produce stable fixed income for the foreseeable future. With such investments, I will know how much I’ll be paid next year and the year after, and I am happy to hold them through broader market volatility.

Whether material, educational, or monetary, our purchase decisions can offer sustained benefits, contributing to a higher quality of life and often creating savings or growth that extend well into the future. Over the years, you would have made several purchases that fulfill their immediate purpose and provide enduring value over the long term. It could be durable kitchen appliances, a comfortable mattress, quality tools, vehicles, exercise equipment, art and collectibles, or even real estate. Please share some of your standout purchases that have exceeded their initial purpose in the comments section.

Read the full article here