First Quantum Minerals Ltd. (OTCPK:FQVLF) finalized a deal last month that gives them a 55% stake in Peru’s La Granja – one of the world’s largest undeveloped copper deposits. In addition to other ongoing and planned projects, First Quantum could see annual output more than double to 1.6 million tons in the next five to six years. However, the company may face major challenges to meet these volume levels including labor strife and contract disputes with the government in Panama. Not to mention, high interest expenses and rising operating costs have hurt cash flows and weigh on the valuation. That said, I think the stock is worth holding given the long-term upside of the company’s strategic copper assets and the stock’s momentum.

La Granja: Boosting Long-Term Copper Arsenal

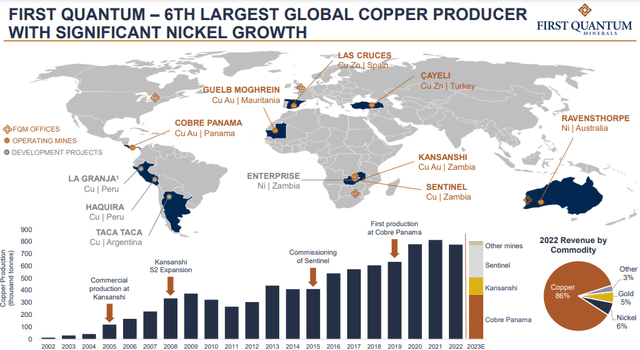

First Quantum, headquartered in Vancouver, is among the ten largest copper producers in the world, deriving 86% of its $6.76 billion in sales in the past twelve months from the red metal, the remainder coming primarily from nickel and gold.

The company’s mining operations are spread across seven countries, including Panama, Zambia, Australia, Finland, Spain, Turkey, and Mauritania. The Cobre Panama operations drove 40% of revenue in the trailing twelve months, followed by two mines in Zambia, which collectively accounted for 46% of sales.

First Quantum Copper Production Profile (First Quantum May Investor Deck)

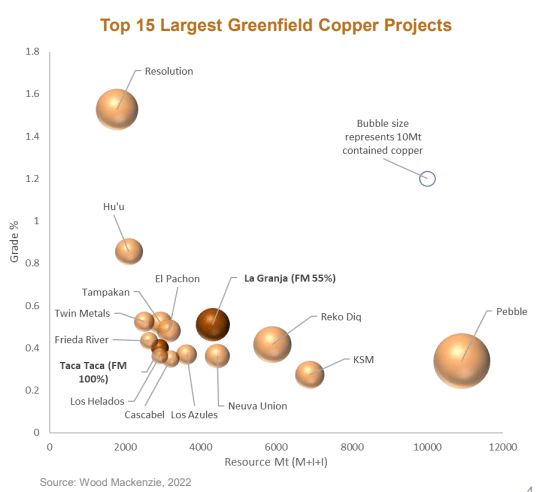

First Quantum also has three greenfield projects underway: two in Peru and one in Argentina. These projects represent major upside in light of massive copper shortages many expect in the long-term along with a dearth of global capital investments and lack of new discoveries.

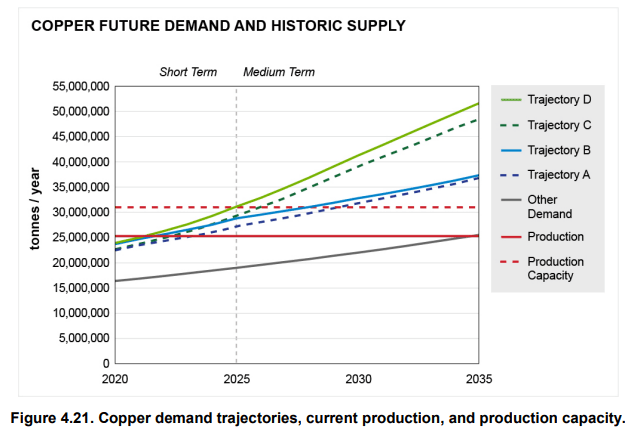

The U.S. Energy Department in an assessment released in July indicated that the annual copper supply gap could actually reach as high as 20mln tons by 2035 in a net zero emissions by 2050 scenario – if current production levels remain flat (trajectory D in the table below).

US DOE Copper Supply Gap Projection (US Energy Department Report June 2023)

S&P Global in a forecast earlier this year projected that development capital expenditure for copper projects could drop by over 18% in 2023 compared to the prior year.

This only underscores the significance of First Quantum finalizing its deal with Rio Tinto to secure controlling interest in La Granja, one of the largest undeveloped copper deposits in the world. La Granja has inferred resources of 4.32bln tonnes at 0.51% copper (more than 20Mlbs of contained copper). The operation is expected to produce 500kt of copper annually, implying about $2.2bln in revenue, and has a mine life of 40 years (MetalMiner reported, citing analysts).

Top Greenfield Copper Projects (First Quantum Investor Presentation)

Key details of the La Granja deal, which was announced on August 27, include:

- First Quantum will pay $105mln for its 55% stake

- Another $546mln will be invested in the feasibility study and construction

- The feasibility study is expected to take 2-3 years

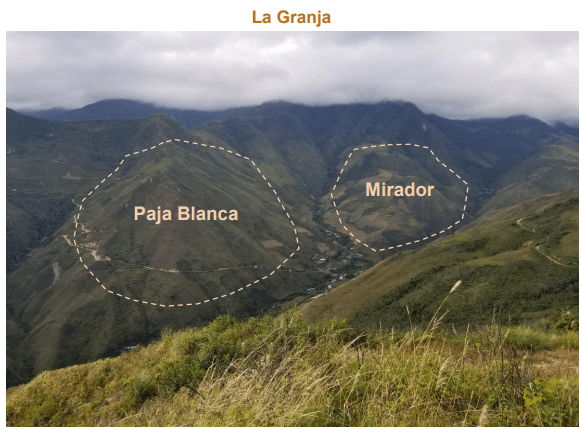

La Granja, located in northern Peru at an altitude of between 2,000 and 2,800 meters, has been under Rio Tinto’s control since buying it from the Peruvian government in 2006. Rio Tinto has already carried out over 300,000 meters of drilling that significantly expanded the resource and indicated high potential exploration targets. Two distinct porphyry copper centers have been identified by Rio Tinto: Paja Blanca and Mirado.

La Granja asset in Peru (First Quantum Investor Presentation)

First Quantum’s next step will be to undertake a feasibility study to update the geological resource and reserve model. The work program over the initial years will focus on:

- Additional infill drilling to upgrade inferred Resources to Measured and Indicated categories and target high potential exploration targets

- Metallurgical studies to establish optimal processing configurations

- Extending community support for project development over a wider area

- Layout of infrastructure, including tailings management, logistics, and product export options

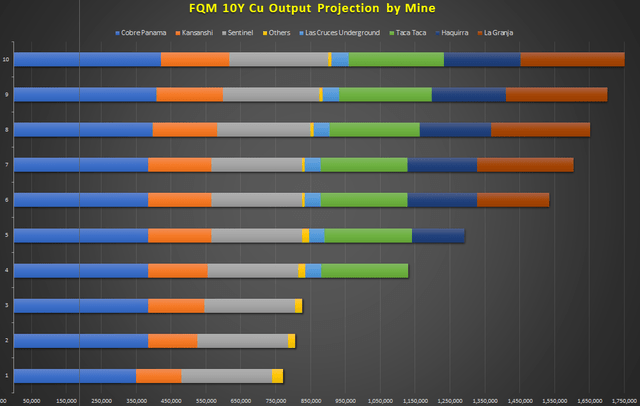

By adding La Granja to the mix, First Quantum could expand its copper profile to over 1.6Mln tons per year by 2029. In addition to the completion of brownfield initiatives, this requires the following major assumptions around the timing of the development projects (all estimates are the author’s):

- La Granja (Peru) – Assume 2.5 years for the feasibility study and two years for construction prior to production. Author’s projected production ramp up date: Q2 2028.

- Haquirra (Peru) – In the Environmental Impact Assessment phase. Projected startup: Q2 2027.

- Taca Taca (Argentina) – Awaiting green-light for construction – decision may come in 2024. Projected startup: 2026

Author Estimates of First Quantum Production (MH Analytics)

First Quantum Stock Relative Valuation

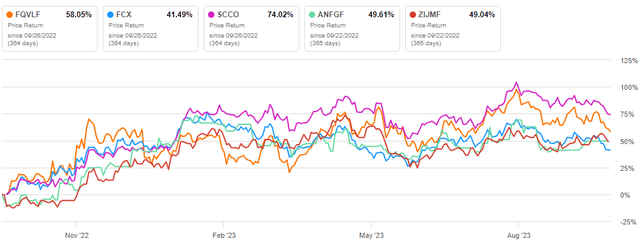

The stock has risen by almost 60% in the past 12 months, second to Southern Copper Corporation (SCCO) among the top five publicly-traded pure play copper peers.

First Quantum Stock Performance (Seeking Alpha)

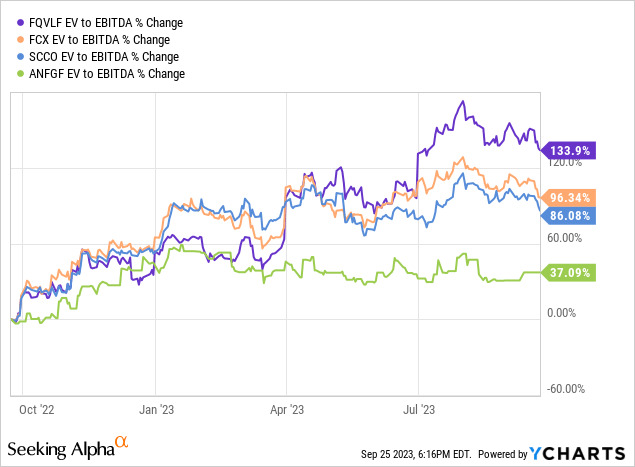

Notice that these five high performers also saw valuation multiples soar along with the stock price, with First Quantum leading the way when it comes to EV/EBITDA, up 133% in the past year.

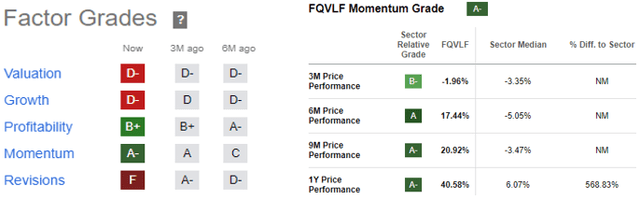

Hence it isn’t too surprising that First Quantum secured high quant grades on momentum and an “F” in valuation.

First Quantum Factor Grades and Momentum (Seeking Alpha)

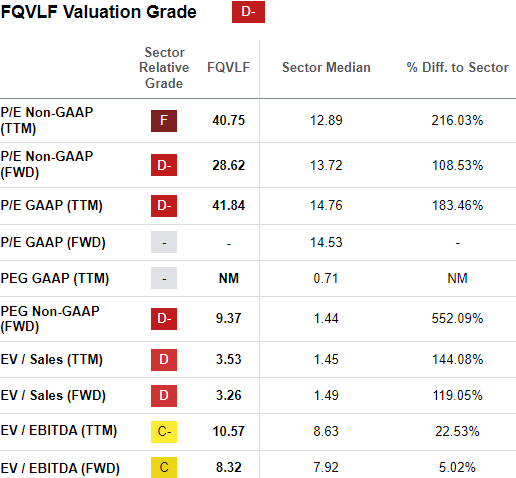

First Quantum is trading at a mind-boggling 40x earnings – albeit this is a bit misleading when you take into account future long-term growth.

First Quantum Valuation Grade (Seeking Alpha)

Notice that per consensus EPS estimates the implied forward P/E for fiscal year 2023 is 26.7 and drops to about 8.2 by 2026 (this view by the way is in Canadian dollars but the ratios should hold).

First Quantum Consensus Earnings Estimates – Canadian Dollars (Seeking Alpha)

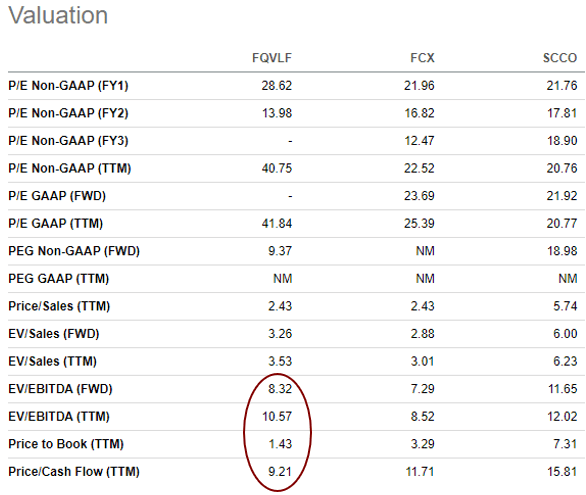

Not to mention forward EV/EBITDA of 8.32 is only 5% above the material sector median. Moreover, putting aside the price-to-earnings ratio over the past 12 months, First Quantum compares favorably versus top peers in EV/EBITDA, price/cash flow, and price to book.

First Quantum Valuation Metrics vs. Peers (Seeking Alpha)

First Quantum Stock Intrinsic Valuation

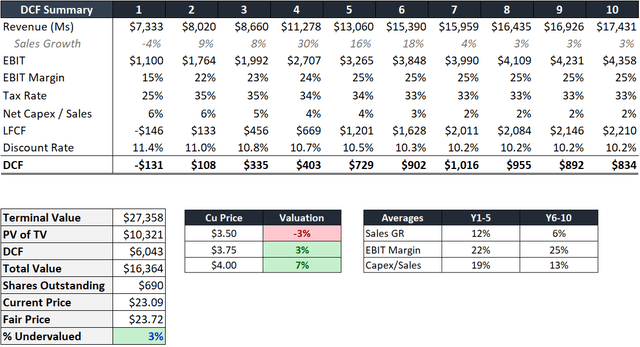

Below outlines the assumptions behind key inputs of the discounted cash flow analysis I conducted to arrive at an intrinsic value for First Quantum.

Sales Growth – I relied on consensus estimates for the top line in the first three years of the DCF model which seemed in line with the company’s three-year guidance. For years 4-10 I then relied on mine plans in technical reports for each operation, assuming mine expansion of 3% in the final three years (as opposed to leaving flat).

Price Assumptions – Copper – $3.75/lb, Gold – $1,900/oz, Nickel – $9.40/lb

EBIT Margin – I started with the most recent twelve months margin of 15% as a starting point and gradually moved up to the major copper peer average of about 25%. I moved very gradually in light of cost issues I address in the risk section.

Interest Expenses – I begin with an interest expense to sales ratio of 10% in line with the trailing twelve months. I lower gradually based on the company’s plans to tackle debt.

Capex – I leveraged company guidance for capex spending figures for years 1-3 then lowered to industry averages in line with moderate growth.

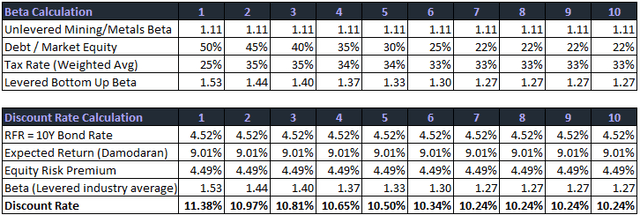

Discount Rate – I employed the Capital Asset Pricing Model (CAPM) based on the following inputs and method to calculate beta and the discount rate:

- I levered the metals & mining industry average beta (sourced from Professor Aswath Damodaran’s data updates) according to First Quantum’s tax structure and debt to market equity ratio.

- Beta changes each year because tax rate fluctuates based on geographic sales shift, and I lower debt to market equity ratio toward the industry average over time.

- I then use the 10-year bond for the risk free rate and expected market return is based on Damodaran’s analysis derived from analyst estimates. The discount rate shifts from 11.38% in year 1 to 10.24% by year ten.

First Quantum Discount Rate Calculation (MH Analytics)

In the end, based on this DCF, the stock looks to be trading at about 3% below its intrinsic value, according to the base case. The DCF summary below includes a copper price sensitivity table and displays averages of key metrics.

First Quantum DCF Model Summary (MH Analytics)

Risks

I see key risks in three company-specific areas: potential project delays, cost management, and debt.

Project Delays

There are a number of potential challenges that could delay the ramp up of key projects, including more labor strife, environmental protests, and government delays. Earlier this month, First Quantum struck a deal that headed off a strike at its copper mine in Panama. The union said it achieved a salary increase – but did not specify the amount – along with bonuses and improvements in social benefits.

In March, the company finalized a draft of a 20-year deal with Panama’s government after a period of tensions that put to end a contract dispute over royalties and back payments. As a result of the deal, the adjusted effective tax rate for 2023 is expected to be between 35% and 40%. Next steps include endorsement by the comptroller and approval by the National Assembly.

Costs

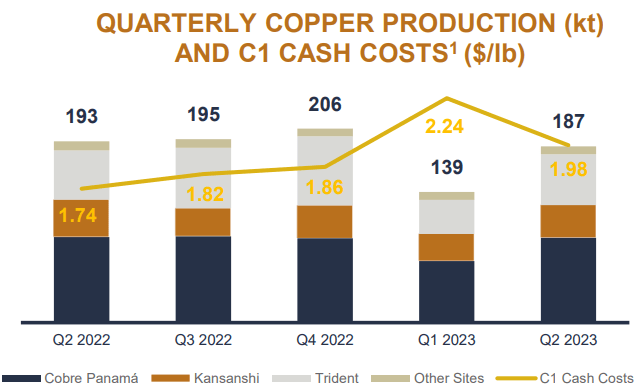

I was reluctant to aggressively escalate the EBIT margins in the DCF model given there is little reason to expect operating costs to come down dramatically any time soon. Notice the trend shown in the Q223 report – cash costs year-over-year rose from $1.74/lb to $1.98/lb. In the three-year guidance the c1 projections remain steady between $1.65/lb to $1.85/lb for 2023 and 2024 and $1.60-$1.85/lb in 2025.

First Quantum Quarterly Production vs. Cash Costs (Q223 Results Presentation)

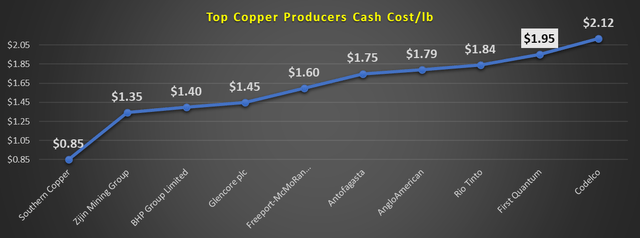

Based on aggregate costs vs. copper produced in the first half of 2023, First Quantum c1 costs amounted to $1.95/lb – one of the highest among the major copper producers.

First Quantum C1 Costs vs. Peers (Data: Company Filings)

Managing costs becomes even more crucial in light of falling copper prices. The red metal is up 11% in the past 12 months but down almost 12% in the past six largely due to concerns over China demand.

Copper Price Performance – Past 6 Months (Seeking Alpha)

Debt

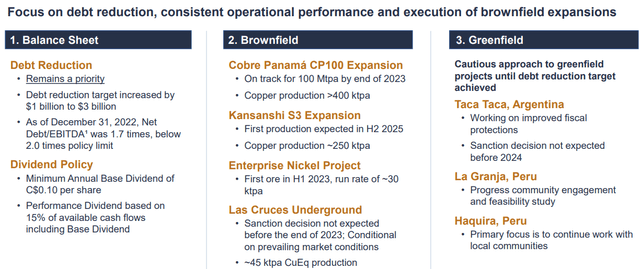

It is important to point out that First Quantum said it will remain cautious on allocating capital to greenfield projects until the company reduces debt from its current level of $7.98 billion to a target of $3 billion. As the DCF model highlighted, the high interest expenses have a major negative impact on free cash flows.

First Quantum Capital Allocation Plan (First Quantum Investor Presentation)

Conclusion

Finalizing control of the La Granja asset in Peru in a deal with Rio Tinto solidified First Quantum’s long-term copper portfolio and opens the opportunity for the company to grow production of the red metal from 770kt/year to 1.6 million tons/year by about 2029. However, the company’s stock appears to be trading at close to fair value based on a DCF analysis. Moreover, First Quantum needs to reduce debt and operating costs significantly in order to generate cash flows that justify the valuation. Hence, now is not a good time for a new investor to dive in. However, given the stock’s undeniable momentum and the company’s long-term strategic profile, I rate First Quantum a hold.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here