By Francesco Pesole, FX Strategist

We estimate that further US bond weakness and 10-year Treasury yields hitting 5.0% would bring EUR/USD to the 1.02 area. While near-term upside risks to back-end yields are non-negligible, short-term USD swap rates should be more capped given a smaller pricing/dot plot gap compared to last June. Our medium-term baseline remains bullish for EUR/USD.

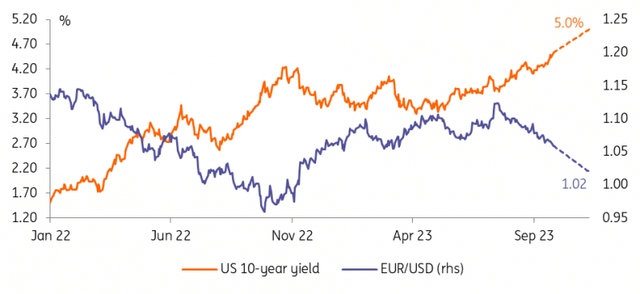

10Y Treasuries at 5% can bring EUR/USD to 1.02

Our colleagues in rates strategy argued in this piece that 5.0% 10-year US yields are no longer a remote possibility. The higher-for-longer Federal Reserve narrative that has been supporting the dollar recently has been mirrored in higher treasury yields, and the implications for the FX market are tangible.

We simulated a scenario where the 10-year Treasuries hit 5.0%, based on the past year of EUR/USD coefficients. We estimate the pair would be trading around 1.02 with 5.0% 10Y yields.

That would be an approximate 3.5% drop from current levels, the same kind of depreciation observed in the period when UST 10Y yields rose from 4.0% to the current 4.50% levels (EUR/USD sliding from 1.10 to 1.06).

EUR/USD and Treasury yields

Dashed lines are ING estimations in a 5.0% UST 10Y scenario

Refinitiv, ING

Smaller hawkish repricing potential for short-term swap rates

The rewidening of the USD:EUR short-term rate differential in the past few months has been another driver of EUR/USD depreciation. It must be noted that such re-widening has been entirely driven by rising US swap rates, and not by a decline in EUR rates.

With US swap rates facing wider volatility on the back of the Fed’s higher starting point to cut rates, we can expect the EUR:USD short-term swap rate differential to continue to be driven predominantly by the dollar leg.

Incidentally, the chances of the European Central Bank making a rapid transition to monetary easing appear inconsistent with the lingering hawkish pressure from numerous members of the Governing Council.

Once it’s been determined that USD short-term swap rates will remain the key driver, it’s worth investigating whether they have the same potential that our rates team attached to the 10-year Treasury yields.

The price action since June can help us in this case. Back then, like now, there was a question of markets not fully trusting the hawkish dot plot in the aftermath of the Fed meeting.

Expectations of Fed easing – rather than the level of the terminal rate – have been driving most dollar moves of late, and markets are now attaching a greater weight to the 2024 dot plot projections.

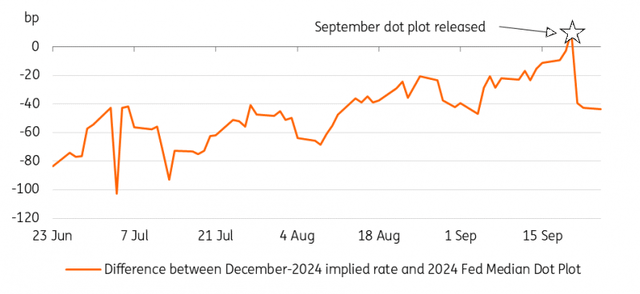

We can see in the chart below that the gap between the current end-2024 implied rate (4.68%) and the September median dot plot for 2024 (5.13%) is around 40bp, much less than the 80bp+ after the June meeting.

Market pricing closer to dot plot compared to June

ING, Refinitiv

US activity data in the summer months pushed market pricing closer to the median dot plot for 2024, and the same could happen in the fourth quarter. However, the room for a hawkish repricing is now substantially smaller than it was in June.

The room for a hawkish repricing is now substantially smaller than it was in June

Incidentally, the Fed only has two more meetings to deliver on its “promise” (as per its 2023 dot plot) to hike one last time this year. Should it pause until December, one 25bp hike could theoretically be trimmed off the 2024 projections as well, more than halving the gap with market pricing.

EUR/USD implications

While we do see risks of US back-end yields staying high, and cannot exclude a 5.0% scenario for the 10-year tenor, additional bearish pressure at the shorter end of the USD curve may be curbed.

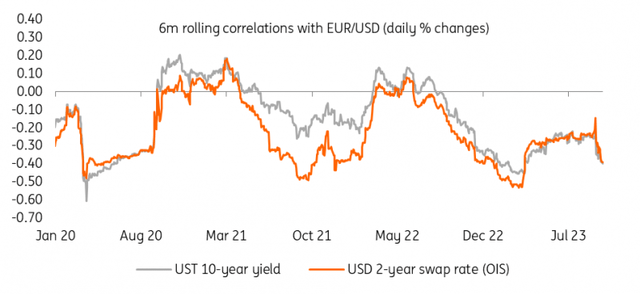

A look at recent EUR/USD correlations suggests that the pair has responded to back-end US yields just as much as short-term swaps. All in all, we estimate 1.02 as the most likely bottom for EUR/USD in a scenario where the US bond sell-off continues.

Correlation between EUR/USD and US 10-year yields/2-year swap rate

ING, Refinitiv

Our baseline scenario in the medium term, however, signals the opposite. ING’s economics team is expecting a sizeable re-rating in the US activity outlook by the first quarter of next year as excess savings are drawn down and the consumer spending support to the US economy dwindles.

We sit on the more dovish end of the spectrum when it comes to Fed expectations and therefore expect a dovish repricing to drive a dollar decline in 2024.

In the short run – i.e. until US data turns negative – the growth differential between the eurozone and the US, a lingering high real USD rate and an unstable risk environment point to a downward-tilted balance of risks for EUR/USD. We think 1.05 may be the bottom for the pair in current conditions, but as discussed, a drop all the way to 1.02 cannot be excluded.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here