Thesis

Kinross Gold Corporation (NYSE:KGC) is a major gold miner with assets in the United States, Canada, Brazil, Chile, and Mauritania. KGC produces 2 million oz of gold annually from its flagship mines, Tasiast, Paracatu, and La Coipa. Kinross’s project pipeline has a Manh Choh project expected to come into production in 1H24 and Great Bear, which is at the PFS stage.

The company has a robust balance sheet with sufficient liquidity to cover its debt obligations. In 2025, a large portion of its debt is due, and I do not expect any issues given KGC’s improved profitability and adequate liquidity. I believe Mr. Market misprices KGS, thus providing a margin of safety of 17% even in a conservative scenario with the gold spot price at $1500/oz. One red flag is the high acquisition price of the Great Bear project. Kinross paid $360/oz for reserves. I hope the Pre-Feasibility Study will validate the project’s potential, thus justifying the high price. Given all the facts, I give Kinross a buy rating.

Company Overview

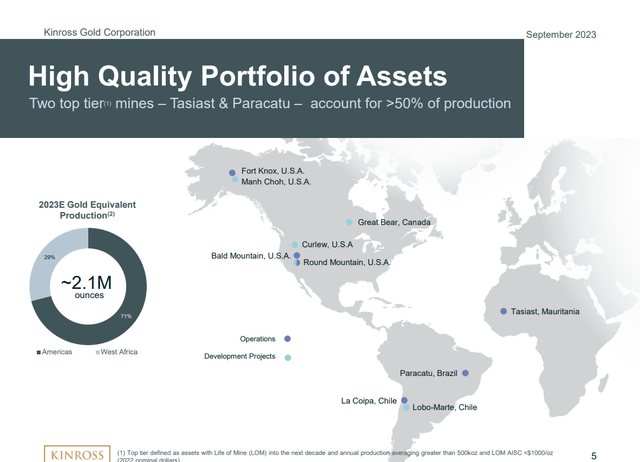

Kinross owns a portfolio of quality assets in Brazil, Mauritania, Chile, USA, and Canada. The map below from the last company presentation shows the KGS mine locations.

Kinross presentation

The Great Bear project in Great Lake, Canada, is anticipated to go into production in 2029. I hope the Great Bear project will justify its high price. The project has an initial indicated resource of 2.7 million ounces and an inferred resource of 2.3 million ounces. Kinross paid an early-stage project price of $1.8 billion or $360/oz. The plans are to reach an annual production of 5 million ounces and expand its resource base to 10 million ounces. Additionally, it is still being determined how much it will cost to put Great Bear into production. For a mine of this scale, costs might probably reach the $2–3 billion level (perhaps higher if inflation remains high).

The Manh Choh Project in Alaska is 70% owned. Throughout its approximately 5-year mine life, the mine is expected to produce 640,000 attributable gold equivalent ounces. The Fort Knox mill, upgraded to handle the new ore, will process the Manh Choh ore. Kinross is still on target to begin production in the second half of 2024 after obtaining crucial operational licenses in May.

Kinross’s flagship producing mines are La Coipa in Chile, Tasiast in Mauretania, and Paracatu in Brazil. The company owns three producing mines in the US. Their total output is 15% of KGC’s annual production. Tasiast mine is the leading asset, with an output of 610 thousand ounces annually. Respectively, La Coipa brings 240k ounces, and Paracatu 580k ounces.

Q2 Review

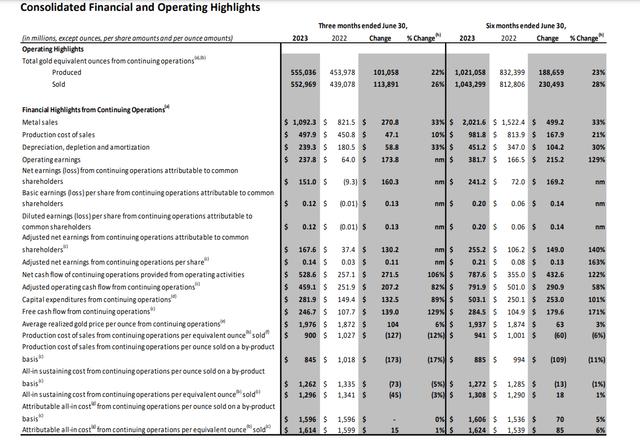

Revenues came to $1,092.3 million for the second quarter of 2023, and net income came to $151.0 million. The table below from the 2Q23 financial report shows financial and operational highlights.

Kinross 2Q23 report

Kinross exceeded expectations, helped by a $100 increase in average realized gold prices compared to the previous year. Besides that, a 22% increase in production from the prior year and All-in-sustaining costs of $1,296 per ounce contributed to that result.

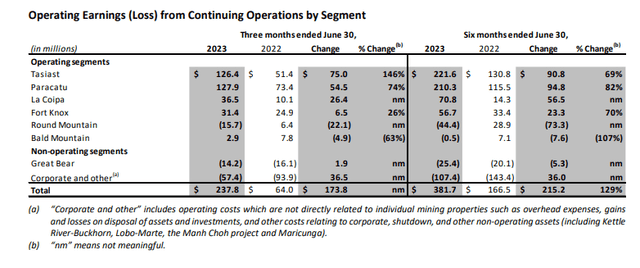

Looking at the results by mine, Tasiast realized sizable growth of operational earnings. The table below shows operating earnings by mining assets.

Kinross 2Q23 report

US mines Bald Mountain and Round Mountain have been a drag, with declining earnings at 63% and realized losses, respectively.

Company Financials

KGC has a neat and clean balance sheet. Its growing production figures and higher gold prices notably improved the company’s liquidity and solvency. The table below shows the Kinross balance sheet metrics I use to evaluate its quality. The data is taken from the last financial report.

|

EBITDA/Interest expenses |

22 |

|

EBITDA – CPX/Interest expenses |

5.4 |

|

Quick ratio |

0.51 |

|

Current ratio |

1.57 |

|

Net debt/EBITDA |

1.38 |

|

Net debt/EBITDA – CPX |

4.65 |

|

Long-term debt/Equity |

31.0% |

|

Total debt/Equity |

41% |

|

Total liabilities/Total assets |

73.1% |

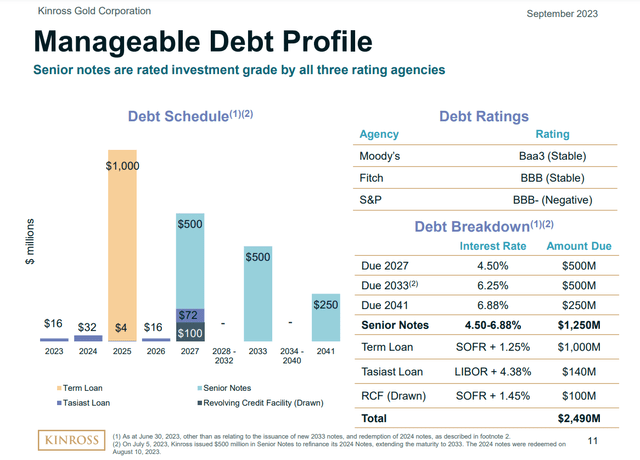

It’s worth mentioning the company’s debt profile. The image below shows debt parameters.

Kinross presentation

In 2025, a large portion of the company’s debt will mature. I do not expect issues repaying that debt due to steady production, stable AISC, and higher gold prices for longer. The remaining debt is well distributed by maturity: $672 million is due in 2027, $500 million in 2023, and $250 million in 2041.

The last few years have been great for gold majors despite rising inflation, COVID-19, and geological turmoil. Kinross is among the top performers among the big players. The table below shows the company’s profitability. The data is taken from the 2Q23 financial report.

|

FCF/EV |

3.6 |

|

Sales/EV |

4.8 |

|

FCF Margin |

7.5% |

|

Gross Margin |

47.4% |

|

ROI |

3.84% |

|

ROE |

3.22% |

|

Net income per Employee |

$21,431 |

All figures are higher than the industry average and KGC’s five-year average. The exception is Net income per employee. In 2022, Kinross realized losses of $642 million due to the divestiture of its Kupol mine. The losses carried over and impacted TTM net income, thus significantly reducing net income per employee.

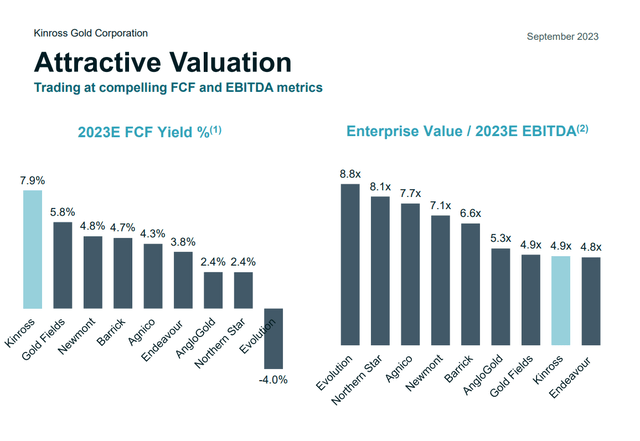

KGC’s FCF yield is higher compared with other majors. The image below weighs up KGC’s FCF yield and EV/EBITDA.

Kinross presentation

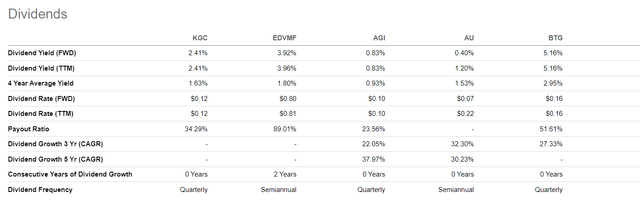

The company generates solid cashflows compared to other miners and, in the meantime, is cheaper. On top of that, Kinross pays dividends with adequate yield, as seen in the table below.

Seeking Alpha

Valuation

Kinross is a gold miner, and as such, I use three valuation methods:

- Net asset value based on the company’s plausible reserves, current assets, and total liabilities.

- Conventional comparison based on EV/Sales and Price/Cash Flow.

- Miners special assessment weighting up EV to Annual production, EV to Plausible reserves, Plausible reserves to Fully diluted shares.

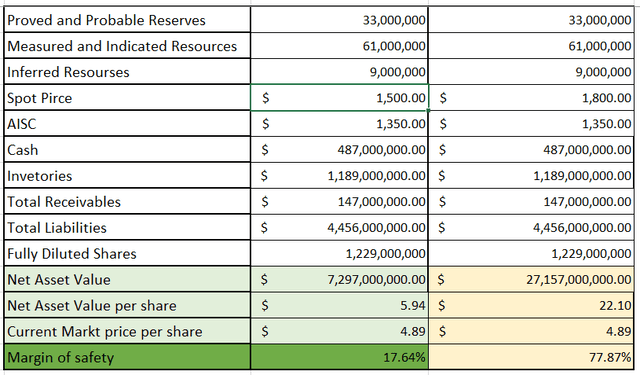

I calculate net assets as follows:

NAV = PR*(SP-AISC) + cash + inventories + total receivables – total liabilities

PR (plausible reserves) = 100% * P&P Reserves + 50%*M&I Resources + 30%*Inferred Resources

Author`s database

I examined two scenarios. One conservative with spot gold $1500/oz. The other is the base scenario using the $1800/oz price.

Conservative NAV per share = $ 5.94

Base NAV per share = $ 22.10

Current Market Price = $ 4.89

Even using $1500/oz gives an adequate margin of safety at 17.6%. However, using base case figures, KGC’s margin of safety moves to 80%.

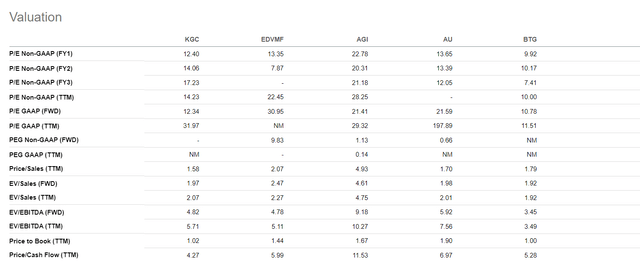

The image below compares Kinross with the following companies:

- Endeavour Mining (OTCQX:EDVMF)

- Alamos Gold (AGI)

- AngloGold Ashanti (AU)

- B2Gold (BTG)

Seeking Alpha

Comparing KGC to other major miners using EV/Sales and Price/Cash Flow it looks cheaper, too. Even overlooked miners with assets concentrated in the Sahel region, like Endeavour, command high multiples.

Last but not least is to compare Kinross based on EV/annual production, EV/Plausible reserves, and Plausible reserves/Fully diluted shares.

Author`s database

EV/Annual production illustrates how much we pay per ounce of annual output. Kinross, with $4100/oz, holds the middle ground. However, measured by EV/Plausible reserves, KGC is the second cheapest to AngloGold. Buying KGC and covering its debt obligations, we pay $128/oz. For AGI, EDV, and BTG, we have more than $200/oz.

Sensitivity to the gold price is measured with Reserves to shares multiple. The higher the ratio, the better. Owning one KGC share means holding 0.05 ounces of gold. Compared to its peers, it is below the mean value.

Risk

The mining business carries enormous risks. On top of that, they vary significantly by the measures required to mitigate them. Kinross had a high-risk profile with its Russian and Mauritanian assets. The divestiture of Kupol Mine significantly reduced the political risk. Tasiast mine is the asset with the highest country risk due to its location in West Africa. Mauritania is one of the countries in the Sahel region with the lowest economic, political, and social metrics. Besides that, Tasiast brings more than 25% of KGC’s annual production. KGC’s other assets are well distributed across mining-friendly jurisdictions such as Brazil, USA, and Chile.

Financially, Kinross has solid standing. Regardless of the difficulties in 2022, the company maintains a robust balance sheet. In 2025, KGC must pay a $1 billion term loan. Considering KGC’s improving profitability, I do not expect any complications.

The metallurgical and geological risks are always present but difficult to assess. The company’s producing assets are well-known parameters. However, the Manh Choh and Great Bear carry some risks. The former is expected to go into production 1H24, though the latter is in the early validation stage as a viable project.

The market risk was a factor impacting gold miners’ share prices negatively. Despite that, Kinross has been a standout performer among its peers this year. Its shares have increased by about 18%, significantly outpacing the VanEck Junior Miners Index (GDXJ) and the VanEck Gold Miners Index (GDX).

Conclusion

Kinross is a quality mining company with a well-diversified portfolio and robust balance sheet. KGC has two projects in its pipeline. The Great Bear project has to prove it is worth its steep price at $360/oz. I hope the Pre-Feasibility Study will validate the project’s potential, thus justifying the high price. Mahn Choh in Alaska is expected to come into production next year. Mr. Market misprices KGS, thus providing a margin of safety at 17% even in a conservative scenario with the gold spot price at $1500/oz. Given all the facts, I give Kinross a buy rating.

Read the full article here