Last week, investors suffered a nasty surprise.

Daily Shot

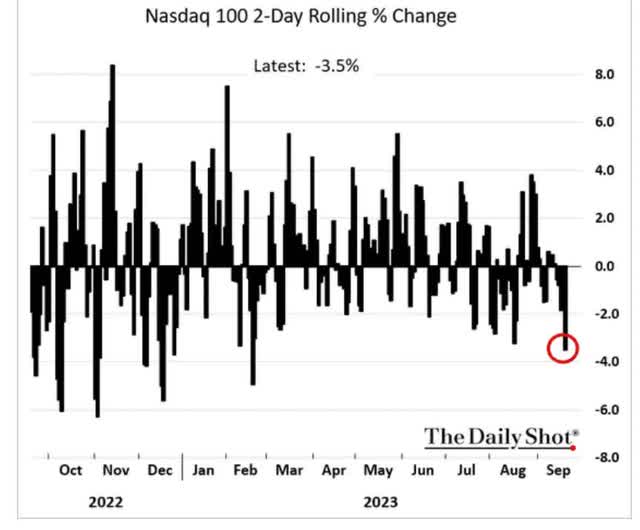

The S&P (SP500) fell 3% in two days and the Nasdaq 3.5%. That’s the worst two-day period in seven months.

The Fed Is Still On The Inflation-Fighting War Path…Kind Of

The Fed didn’t raise rates last week, which was a 99% probability going into the decision. So why did the market react so violently? Because it was overvalued, and the Fed dropped this bombshell.

FOMC

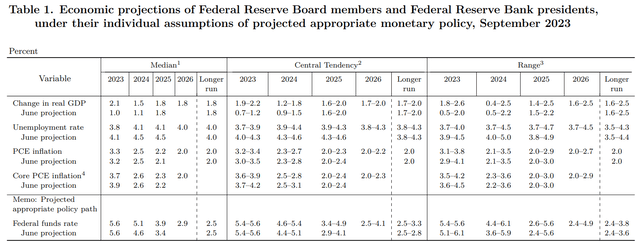

The latest summary of economic projections, or SOP, shows more robust growth and two fewer rate cuts next year, down from four to just two, possibly not until November and December.

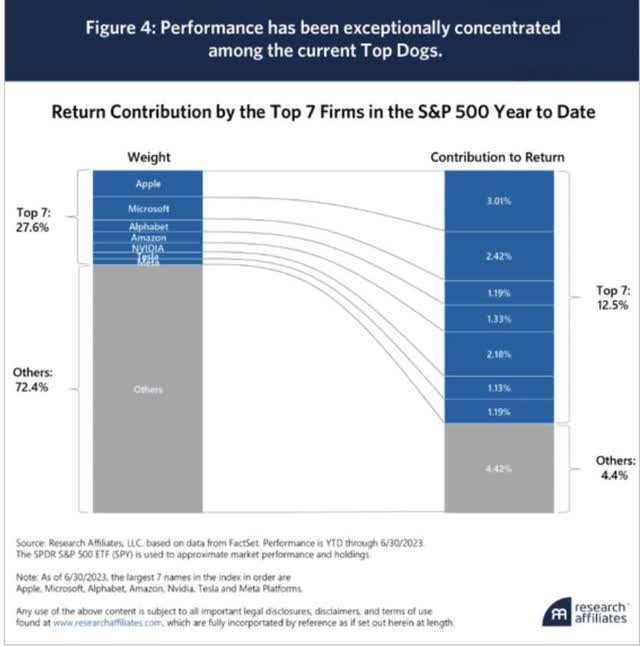

Remember who is leading the market higher this year: the magnificent seven.

Daily Shot

About 75% of the market’s gains this year are from these seven mega-cap tech stocks.

Daily Shot

It’s not the S&P 500 or Nasdaq 100. It’s the S&P 7 and Nasdaq 7.

Well, guess what?

JPMorgan Asset Management

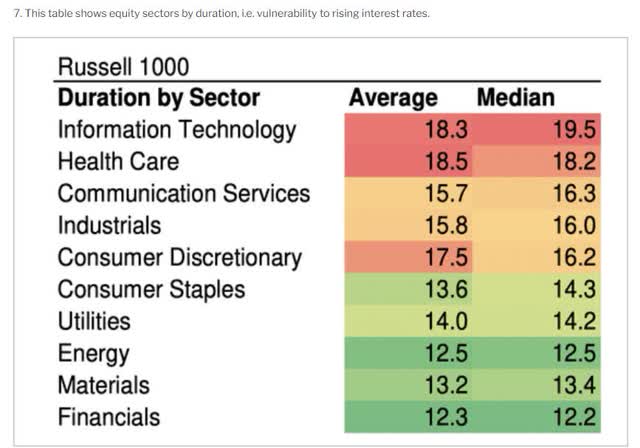

Tech is the longest-duration sector in the stock market.

For 15 years, the stock market cared only about the Fed. So, with the Fed expected to start cutting rates aggressively in 2023, the market took off early this year.

But now the Fed is pouring water on an overheated market where the Nasdaq is 30% historically overvalued, and the S&P hit a peak premium of 20%.

Daily Shot

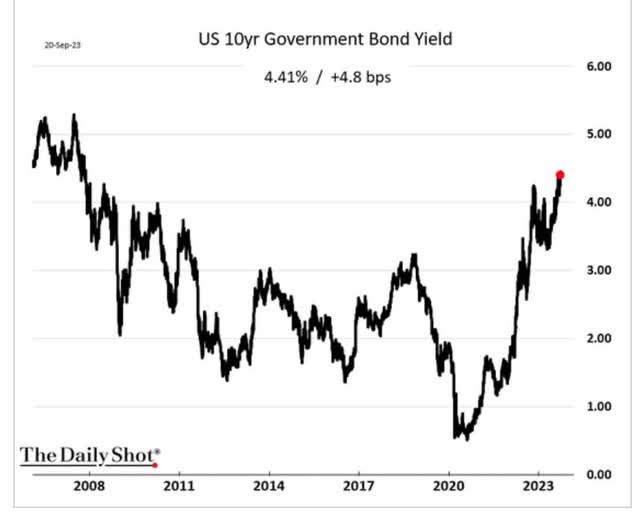

On Thursday, the 10-year yield, the proxy for long-term rates, hit 4.5%, new cycle highs, and the highest levels in 15 years.

The S&P was trading at almost 20X forward earnings, assuming an unprecedented no recession from the most aggressive Fed rate hiking cycle in 42 years.

When Fed rates were zero, 20X earnings was an insane valuation to pay for stocks, and when rates are headed to 5.5% per the Fed’s latest consensus? It’s even crazier.

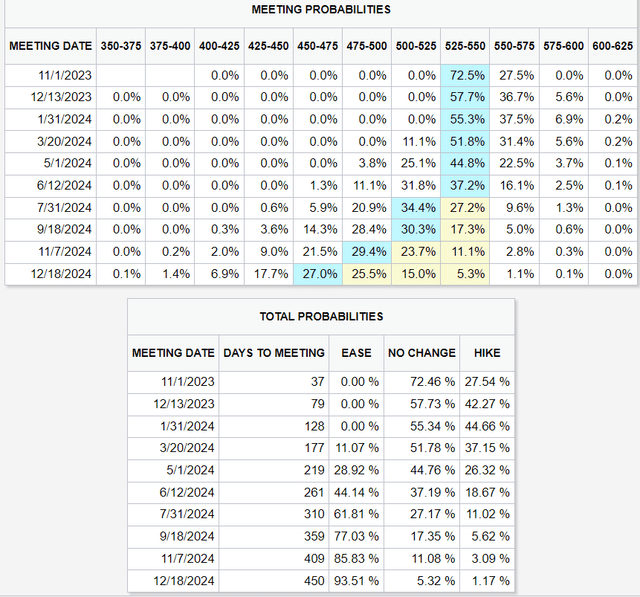

And guess what? The bond market still doesn’t believe the Fed, at least not entirely.

CME Group

The Fed says it will hike to 5.5% in November, and the bond market believes there is a 55% chance the Fed is done hiking. The largest risk of one final hike is January 2024.

- Goldman expects CPI inflation to keep rising and peak in January.

The bond market now expects the Fed to start cutting in September of 2024 and cut three times next year.

The Fed expects to cut twice and possibly not start until November.

For the bond market to catch up to the Fed would require slightly higher short-term rates but potentially much higher long-term rates. Those are the ones investors care about, tech investors most of all.

Daily Shot

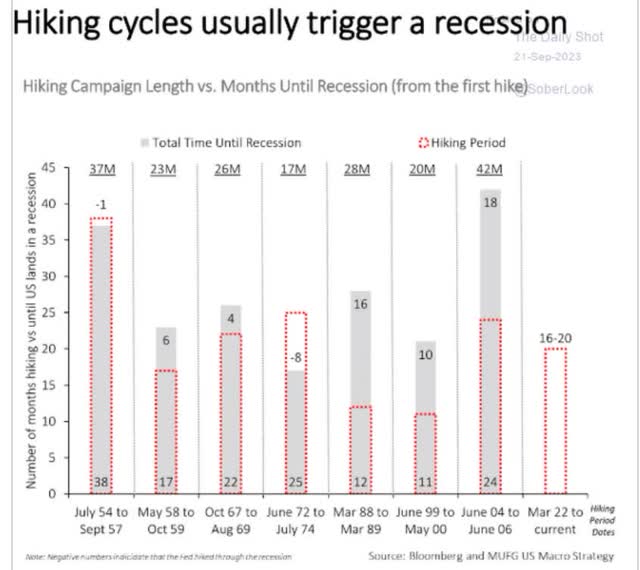

The Fed has been hiking for 18 months; sometimes, it takes 42 months before the Fed causes a recession.

So, if you’re wondering where the recession is, it might not arrive until 2026.

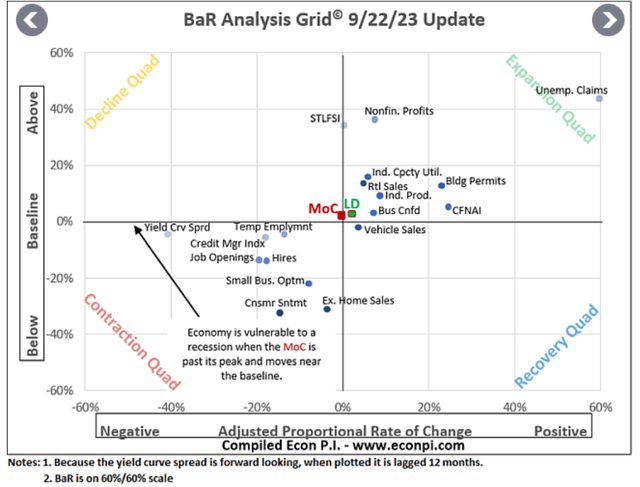

David Rice

Here is where 18 economic indicators are compared to a 30-year historical base-line and how rapidly they change month-over-month.

The red Mean of Coordinates or MOC dot is the average of all 18 and the eight leading indicators; the green LD dot is now slightly above and accelerating.

The economy is getting slightly stronger, risking a reacceleration of inflation.

Daily Shot

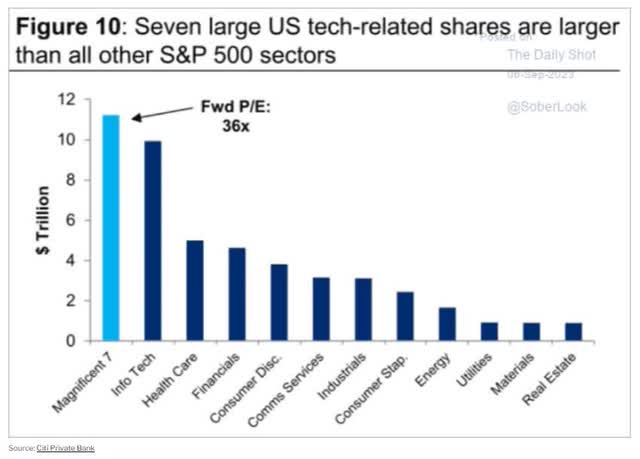

That means there is a lot of risk in tech stocks, especially the magnificent seven with their 36X forward P/E.

Are the magnificent seven great companies? They are world-beaters.

But even in the zero rate world, the long-term average P/E for the magnificent 7 is 25X, not 36.

- do you want to pay a 31% premium over their historical market-determined fair value

- in a higher longer rate world of 5.5% interest rates?

So why not just sit in cash? Why not clip 5.5% coupons on short-term bonds?

While the recession is coming (93% probability of recession in 2024, according to the bond market), it might not arrive until 2026.

Do you know what would happen if the recession arrived that late? The market might not fall much from here. It might just trade flat for the next two years.

But do you know the best investment in such a scenario?

A-Rated Aristocrats: The Ultimate Port In The Storm

Daily Shot

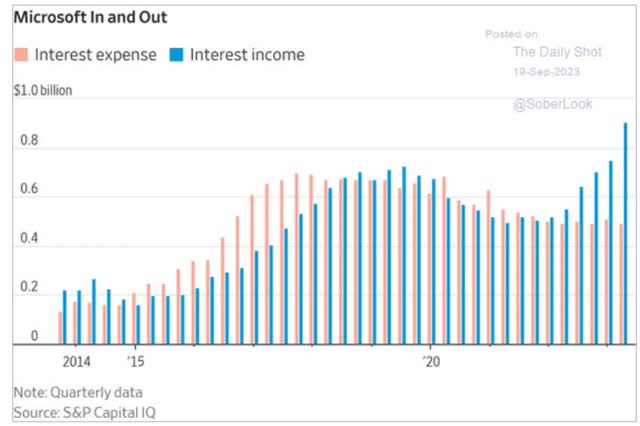

MSFT isn’t an aristocrat yet, but it will be in five years. But note how, thanks to locking in record-low rates in the Pandemic, MSFT is minting money the higher rates go.

Its cash is invested in bonds earning 5.5% while its interest costs are fixed, and it continues to mint cash at a rate of $5.2 billion per month.

MSFT is the most extreme example of how cash-rich A-rated world-beaters have nothing to fear from 5.5% Fed rates that persist all next year.

- some Bloomberg analysts think that’s what will happen next year

- no rate cuts and one final hike in November.

What’s better than buying Buffett-style “wonderful companies at fair prices”? How about Buffett-style wonderful companies at a 30% discount?

The S&P is 15% overvalued. How would you like to buy world-beater A-rated aristocrats at a 30% discount? Well, that’s what we’re here to help you do.

How To Find The Best A-Rated Aristocrat Bargains In 1 Minute

The Dividend Kings ZEUS Research Terminal is the screening tool I use for every article.

- 504 of the world’s best blue-chips

- including every dividend aristocrat, champion, king, and foreign aristocrat

- and future aristocrats

- and Ultra SWANs (mostly wide moat aristocrats)

- and 40 of the world’s best growth stocks (to turbocharger income growth).

| Step | Screening Criteria | Companies Remaining | % Of Master List |

| 1 | “lists” and “Dividend champions” | 135 | 27.00% |

| 2 | Non-Speculative (No Turnaround Stocks, investment grade) | 116 | 23.20% |

| 3 | BHS Rating “reasonable buy, good buy, strong buy, very strong buy, ultra value buy” | 68 | 13.60% |

| 4 | A-Credit Rating Or Higher | 30 | 6.00% |

| 5 |

Sort By Discount To Fair Value |

0.00% | |

| 6 | Top 5 Dividend Aristocrats | 5 | 1.00% |

| Total Time | 1 minute |

So, let’s look at the best A-rated aristocrat bargains for this dangerous market.

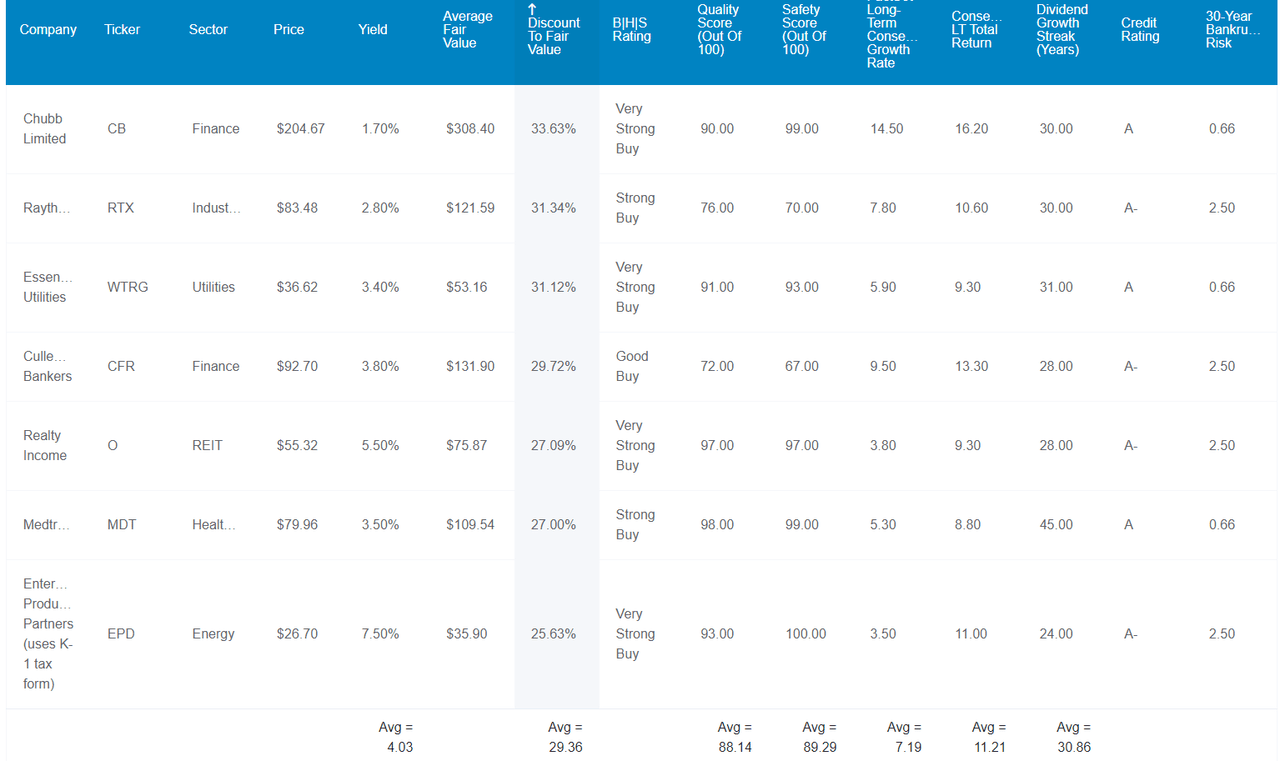

The 5 Best A-Rated Dividend Aristocrat Bargains To Buy Now

I’ve linked to articles exploring each company’s investment thesis and risk profile.

Dividend Kings Zen Research Terminal

- Chubb (CB)

- Raytheon (RTX)

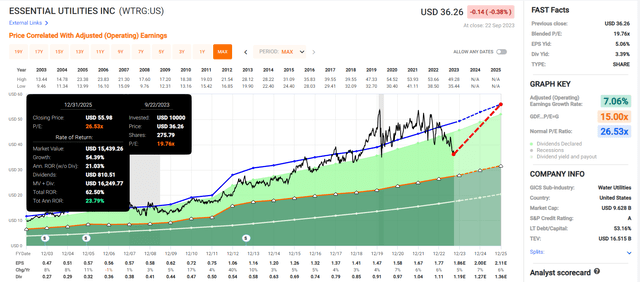

- Essential Utilities (WTRG)

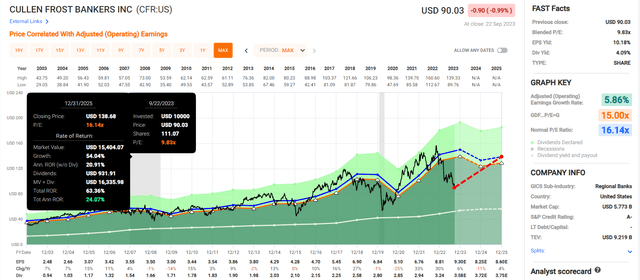

- Cullen/Frost Bankers (CFR)

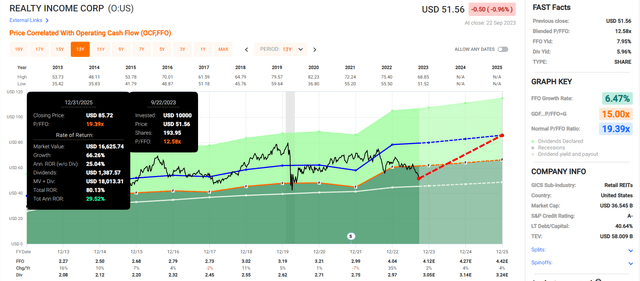

- Realty Income (O)

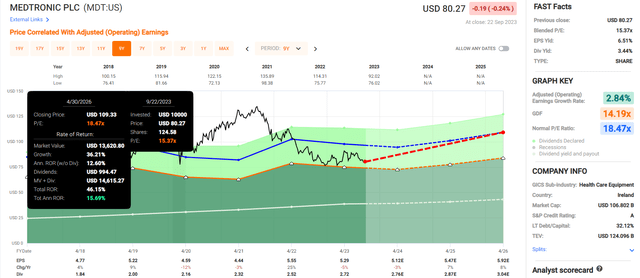

- Medtronic (MDT)

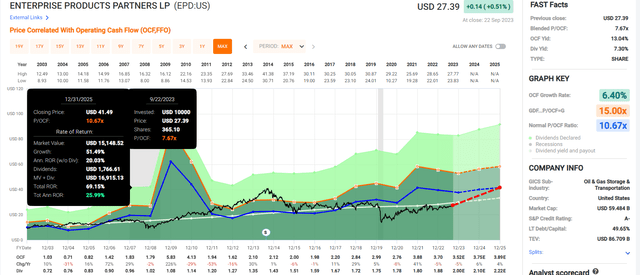

- Enterprise Products Partners (EPD) – K1 tax form.

Fundamental Summary

- Yield: 4.0% (3X S&P)

- dividend safety: 89% (1.55% dividend cut risk )

- overall quality: 90% 13/13 Ultra Sleep Well At Night, dividend aristocrats

- dividend growth streak: 31 years (since 1992)

- credit rating: A- stable (1.71% 30-year bankruptcy risk)

- LT growth consensus: 7.2%

- potential LT total return consensus: 4.0% yield + 7.2% growth = 11.2% CAGR vs 10.2%

- discount to fair value: 29%

- DK rating: potentially very strong buy (6% above Ultra Value Buffett “fat pitch” buy)

- 10-year valuation boost: 3.5% per year

- 10-year consensus total return: 4% yield + 7.2% growth + 3.5% valuation boost = 14.7% CAGR vs 8.7% S&P 500

- 10-year consensus total return cumulative: 294% vs 130% S&P.

4% yield today, A-credit rating, 30-year dividend growth streak, long-term market-beating return potential, and potentially quadruple your money in the next decade.

Do you think the S&P is going to quadruple in the next decade? If so, I have a bridge in Brooklyn to sell you;)

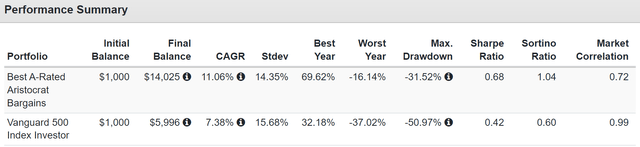

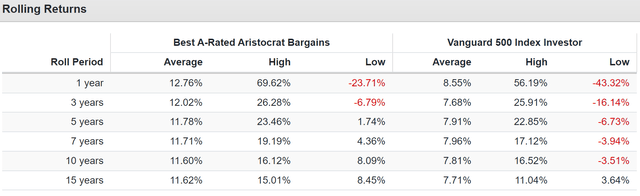

Historical Total Returns Since 1998

(Source: Portfolio Visualizer Premium) (Source: Portfolio Visualizer Premium)

How realistic is it that stable-blue-chips that have historically delivered 11.1% to 12.8% returns for 25 years will keep delivering 11.2% returns in the future? Statistically 97%.

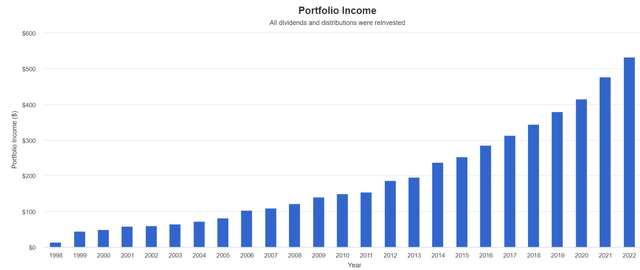

11% Annual Income Growth For 24 Years And 11% Expected In The Future

(Source: Portfolio Visualizer Premium)

2025 Consensus Total Return Potential

- if and only if these companies grow as analysts expect

- and return to historical market-determined fair value

- these are the returns you will make, including dividends.

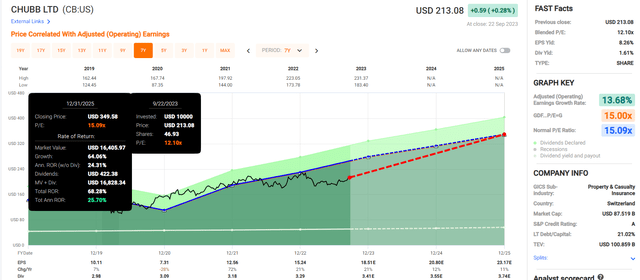

Chubb

FAST Graphs, FactSet

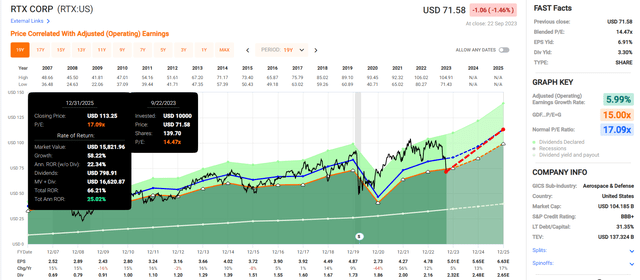

Raytheon

FAST Graphs, FactSet

Essential Utilities

FAST Graphs, FactSet

Cullen/Frost Bankers

FAST Graphs, FactSet

Realty Income

FAST Graphs, FactSet

Medtronic

FAST Graphs, FactSet

Enterprise Products Partners

FAST Graphs, FactSet

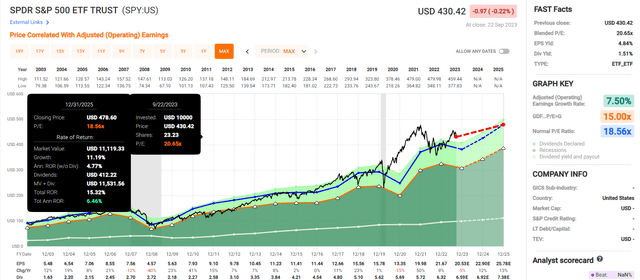

S&P 500

FAST Graphs, FactSet

S&P 2025 consensus is 15% total return or 7% annually.

Most undervalued A-rated aristocrats: 65% or 25% annually.

4X the return potential of the S&P 500 and 3X the much safer yield.

Bottom Line: Don’t Fear The Fed, Trust In The Kings Of Dividend Quality

Many people ask me in the comments, “Why are you recommending anything if a recession is coming and stocks are going to fall?”

Charlie Bilello

Because the economy isn’t the stock market, market timing doesn’t work, and it’s always and forever a market of stocks, not a stock market.

You can get 5.5% in T-bills right now, with zero duration risk or fundamental risk.

But these aristocrats are A-rated, yield 4% today, and offer a 25% annual return potential through 2025.

Long-term, they offer about 3X the returns of bonds, and don’t forget about the 11% annual income growth analysts expect long-term.

- that’s 4X the rate of inflation

- bonds have no inflation hedge ever.

And also don’t forget this from legendary investor Peter Lynch who delivered 30% annual returns for 13 years at Fidelity before he retired a legend.

Nobody can predict interest rates, the future direction of the economy, or the stock market. Dismiss all such forecasts and concentrate on what’s happening to the companies in which you have invested.” – Peter Lynch.

I can tell you that CB, RTX, WTRG, O, MDT, and EPD are thriving. There is nothing broken with these dividend aristocrats.

Aristocrats with A-credit ratings, a 31-year dividend growth streak, and that are 30% historically undervalued and offering 4X the market’s return potential over the next two years.

If you buy these seven? I’m 80% confident (Marks/Templeton certainty limit) that in 5+ years, you’ll be thrilled you did.

Because buying these A-rated aristocrats is practicing disciplined financial science, the math behind getting and staying rich on Wall Street.

Read the full article here