As long-term investors, it is crucial to select companies with a track record of consistent historical performance and strong pricing power, particularly during periods of economic uncertainty. Furthermore, when considering future investments, it’s essential to identify companies well-positioned for long-term growth. In the technology sector, finding businesses that can sustain growth over extended periods can be challenging. Autodesk (NASDAQ:ADSK) stands out as a company that fulfills these criteria. Its history of reliable performance, demonstrated pricing power, and forward-looking positioning make it a compelling potential choice for investors seeking stability and growth potential in the ever-evolving tech landscape.

However, for cautious long-term investors, it’s important to note that the margin of safety is currently low. The stock may indeed be a good long-term investment, but only if it drops below $170, based on DCF analysis.

Autodesk’s dominant position in the market contributes to its pricing power

Autodesk’s pricing power in the market is underpinned by its status as the primary choice for design and engineering software. In various industries, including architecture, engineering, and construction, Autodesk’s products are considered indispensable due to their comprehensive features and industry-specific tools. This lack of viable alternatives positions Autodesk as a virtual monopoly in these sectors. With few comparable options available, customers often have little choice but to continue using Autodesk’s software, providing the company with substantial pricing power.

One key product that exemplifies Autodesk’s dominance is AutoCAD, the leading software in computer-aided design (CAD). AutoCAD has secured an impressive 39% market share, making it the go-to solution for professionals in need of CAD software. Its extensive capabilities and compatibility with industry standards have cemented its status as an industry standard. This overwhelming market share not only solidifies Autodesk’s position but also reinforces its pricing power, as users are reluctant to switch to lesser-known alternatives, ensuring a stable revenue stream for the company.

Hence, the company has demonstrated its ability and willingness to take pricing actions over the years, which is summarized well by GS Investing in a recent Seeking Alpha article:

Looking back the past few years, we can see that ARPU has been increasing:

“So you raised prices at the end of March, and I’m sure that’s all embedded in your guidance and it allows you to invest appropriately and get to the margins you want.” 1Q23 earnings call

“The uptick in the conversion rate was expected as our maintenance renewal prices increased by 20% in the second quarter, making it more cost-effective for customers to move to subscription.” 3Q2020 earnings

“Effective earlier this month, for all maintenance contracts up for renewal, the price to move to subscription increases 5%, and maintenance plan prices increase 10% if they choose to stay on maintenance.” 1Q19 earnings

As the company continues to expand its push into the subscription revenue model (subscription revenue increased by 12% in constant currency year-over-year in Q2 FY2024), we can anticipate that pricing actions will have an increasingly significant impact in the future.

Additionally, Autodesk’s complete dominance of the European market (it is stated that Autodesk has a market share of 66% in the CAD category in Europe) offers a substantial avenue for revenue growth. With approximately 35% of its revenue originating from Europe, there is significant untapped potential within this region. As the European economy continues to evolve and industries expand, Autodesk’s suite of design and engineering software is poised to play a pivotal role in driving innovation and efficiency.

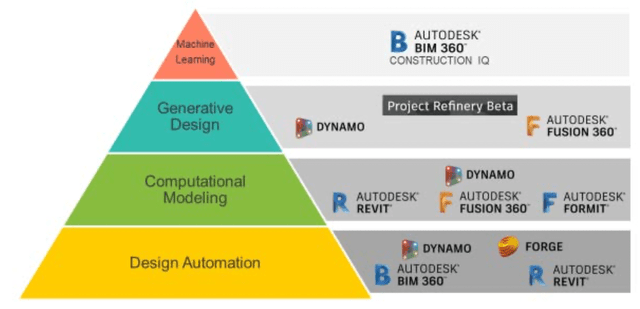

AI is not just a buzzword for Autodesk

Looking into the future, Autodesk is set to revolutionize the design stage by harnessing the power of artificial intelligence (AI) across multiple domains within the design and engineering process. This AI-driven transformation will involve various approaches, each with distinct capabilities:

- Parametric Design: Establishing relationships between design elements.

- Design Automation: Automating tasks within parametric models with scripts.

- Computational Modeling: Explicitly describing processes to create design outcomes.

- Option Generation: Exploring design variations given specific rules.

- Design Optimization: Defining goals and exploring model states to meet them.

- Machine Learning: Using historical data to generate designs based on stated outcomes.

- Project Refinery: Autodesk’s tool for exploring and optimizing designs using AI algorithms and data-driven decisions.

This AI-driven approach aims to facilitate decision-making by presenting multiple design outcomes, resulting in higher-quality work, increased productivity, and cost savings. By connecting generative design processes to mainstream building production applications like Revit, Autodesk aims to revolutionize the design stage in architecture, engineering, and construction, offering a more intelligent and efficient way to design and build structures.

“The application of Autodesk generative design solutions results in higher quality work, greater speed/productivity, and lower costs.” (Source)

Autodesk

Given the rapid pace of Gen AI development, we can anticipate significant advancements in Autodesk’s products in the near term. Consequently, the company can further enhance its pricing power and ensure a consistently high subscription renewal rate in the years ahead.

The company has demonstrated phenomenal financial performance over the past years, with steady revenue growth and a safe balance sheet

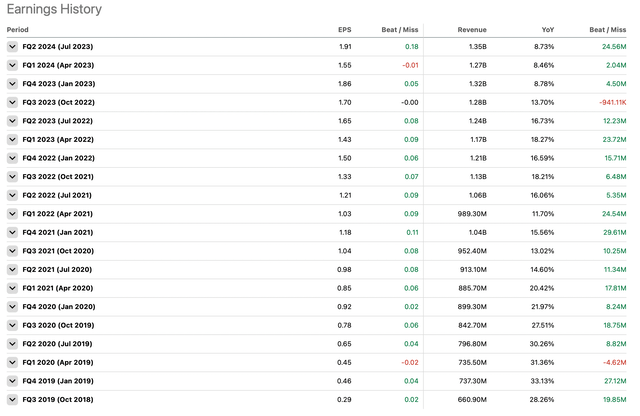

Autodesk’s historical financial performance paints a remarkable picture of a solid and thriving company in the tech industry. One standout achievement is the company’s impressive track record of double-digit revenue growth, spanning at least 17 consecutive quarters from the third quarter of 2019 to the same period in 2023.

Seeking Alpha

Moreover, over the last three quarters, the company has maintained a solid revenue growth rate of around 9%. This resilience highlights Autodesk’s ability to weather challenging economic conditions and its capacity to continue providing value to its customers, even in turbulent times.

Autodesk’s financial strength is further exemplified by its expanding operating margin. In just a few years, the company has significantly improved its operating margin, soaring from a mere 1% in 2019 to a robust 20% at present. This impressive transformation signifies Autodesk’s effective cost management and operational efficiency, which have contributed to its sustained profitability. As the company holds significant pricing power and increases its share of revenue from subscriptions, we can expect the margin expansion to continue in the future.

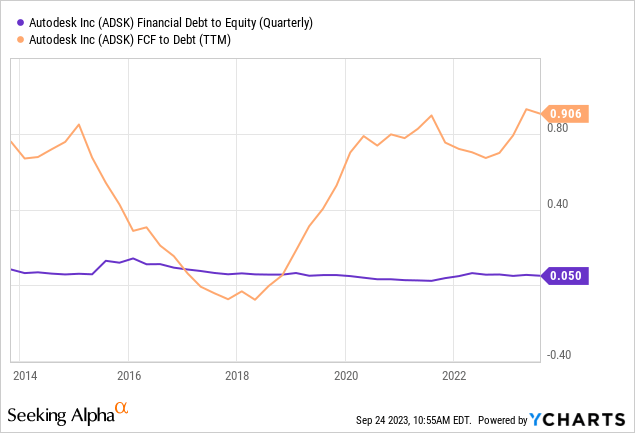

Furthermore, Autodesk’s consistent debt-to-equity and debt-to-cash ratio over time is a testament to its prudent financial management, showcasing its minimal dependence on borrowed funds for day-to-day operations and expansion strategies. This financial strength not only underscores the company’s fiscal responsibility but also highlights its capacity to allocate substantial resources towards future ventures, particularly in the realm of AI.

These points enhance ADSK’s appeal as a potentially secure option for long-term investors, assuring them of the company’s ability to weather uncertainties and embrace future growth opportunities.

Assessing the margin of safety: a DCF analysis

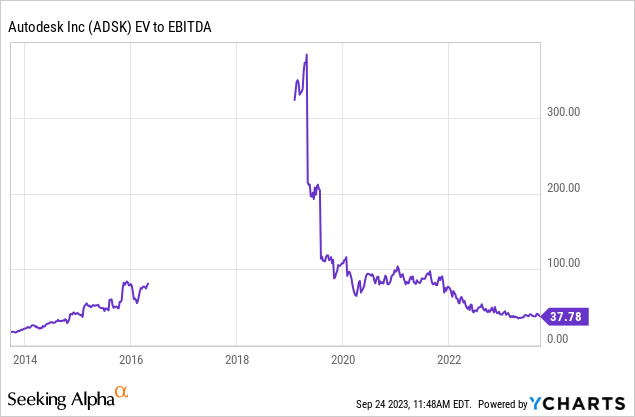

Despite the positive points above, ADSK stock appears overvalued at the moment, with about 8 P/S, 37 EV/EBITDA, and 27 forward P/E (non-GAAP). To assess an appropriate entry point, I use DCF analysis.

My analysis is based on the following key assumptions:

1. The average annual revenue growth over the horizon period of five years is estimated to be around 10.4%, with a 9% increase in 2023 (FY2024) and 12% growth between 2024 and 2027, based on analysts’ earnings estimates and adding a fraction of potential AI-driven growth.

2. EBITDA margin will increase to 25% and remain stable throughout 2027.

3. Then goes the WACC.

The after-tax cost of debt is 2.6% (using 15% tax rate), based on the latest Q-10 filings. The cost of equity capital (17.8%) is calculated using CAPM, with 1.49 beta, 4.4% risk-free rate, which is the current U.S. 10-year bond yield, and 9% market premium. The WACC is, therefore, estimated to be around 17%.

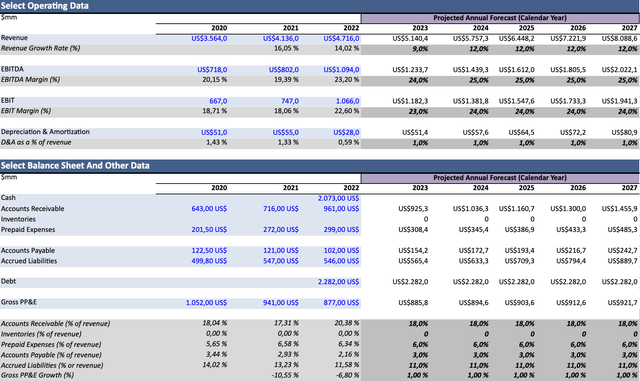

Here is the operating and balance sheet data used in the modeling:

The author’s DCF model

As a result of these calculations, AMD’s fair price range is approximately $173-183, which is about 10% lower than the current stock price.

Note that this price range assumes that the EV/EBITDA multiple will be around 29-31 after the 5-year forecast period, which is still a bullish assumption. This level is the current average EV/EBITDA of design/software peers like Dassault Systèmes (OTCPK:DASTY) and Roper Technologies (ROP). Importantly, before 2015, ADSK traded at around 25 EV/EBITDA for a long time.

As always, this does not mean that the stock will necessarily drop to the aforementioned level in the near future, as the market might price in different assumptions for Autodesk. However, for a long-term value investor, ADSK provides no margin of safety, which means we should wait for a drop below $170 before investing.

Key takeaways

In summary, Autodesk stands as a beacon of financial stability with an impressive history of double-digit quarterly revenue growth, increasing margins, and low debt. Autodesk’s dominance in the design and engineering software market, exemplified by its irreplaceable products and substantial market share, solidifies its exceptional pricing power.

Looking ahead, Autodesk’s commitment to harnessing AI across various design domains promises to revolutionize the industry. As Gen AI development accelerates, Autodesk is poised to further enhance its pricing power and maintain a high subscription renewal rate in the foreseeable future.

However, despite these positive aspects, it’s essential to note that Autodesk currently lacks a significant margin of safety for investors. With an estimated fair price range of approximately $173-183 based on DCF analysis, which assumes a bullish EV/EBITDA multiple after the forecast period, caution is warranted. To ensure a margin of safety, potential investors may want to consider entry points below $170.

Read the full article here