Investment thesis

Our current investment thesis is:

- Jill’s growth has been underwhelming, as its niche demographic and competitive pressures have impeded the company’s progress. This has worsened in recent quarters, with negative growth and a lack of new stores. We suspect the business will continue to struggle.

- Offsetting this issue is margins. Jill is highly profitable and significantly outperforming its peers. Margins appear defensible, although we are concerned due to the lack of growth.

- For these reasons, we are hesitant to rate the stock a buy despite its attractive valuation.

Company description

J.Jill, Inc. (NYSE:JILL) is an American retail company headquartered in Quincy, Massachusetts. Established in 1959, J.Jill specializes in women’s apparel, accessories, and footwear. The company primarily targets women over 40 with a focus on casual and versatile clothing.

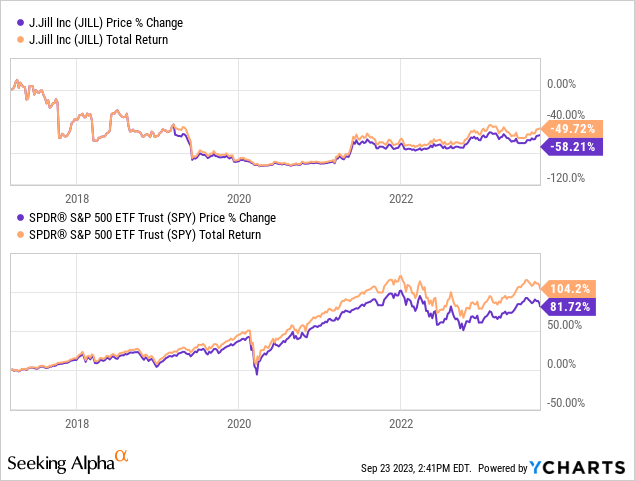

Share price

Jill’s share price performance has been disappointing, losing over 50% of its value in a short period of time. This is a reflection of poor financial results alongside a questionable commercial position.

Financial analysis

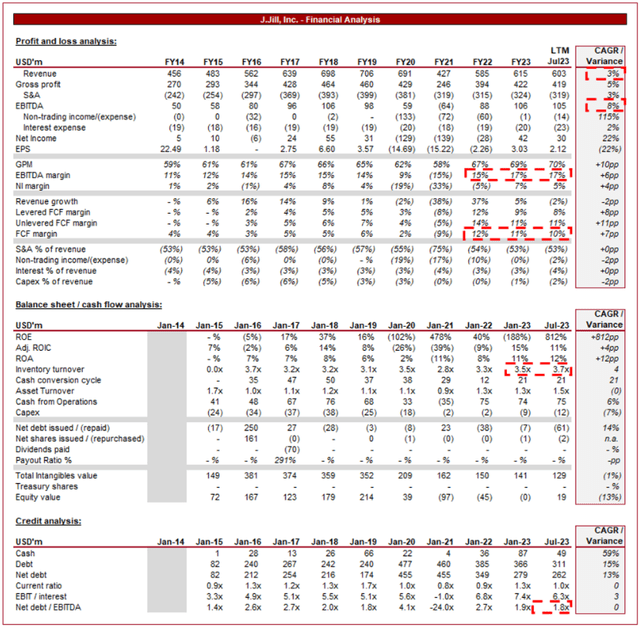

J.Jill Financials (Capital IQ)

Presented above are Jill’s financial results.

Revenue & Commercial Factors

Jill’s revenue has grown at a mediocre 3% during the last decade, with the business struggling following the pandemic. The business has yet to return to its FY20 level, with a downward trajectory following the end of FY23.

Business Model

Jill focuses on a niche market of women who value comfort and style. Its target audience is generally older, seeking clothing that is both fashionable and comfortable for everyday wear. Through targeting this niche, Jill is seeking to tap into a more affluent demographic that is less influenced by trends and taste, reducing volatility.

The company offers a range of women’s apparel, including tops, bottoms, dresses, outerwear, and accessories. The clothing is known for its relaxed fit, soft fabrics, and versatile designs. Jill’s objective is to “keep it simple”, with a focus on function, combined with broadly classical and universally appreciated designs.

The retail industry for women is highly lucrative, as women comprise over 50% of the US population and control/influence over 85% of buying decisions. This has allowed women-focused segments (such as Beauty), as well as apparel to outperform their respective wider industry. We suspect this is a reason for Jill’s strong pricing, reflected in its margins.

The downside of its niche approach, however, is that Jill’s has limited its potential customer base and so growth is somewhat limited. As fashion trends and preferences evolve, the brand may struggle to attract the aging demographic moving into its remit. This is particularly the case as the brand is often associated with classic and timeless clothing, but it has faced challenges in staying relevant and innovative. This said, if Jill does achieve this, an aging US population could contribute to accelerating growth.

Jill operates both physical stores and an e-commerce platform, providing customers with various shopping options. The omnichannel approach aims to create a seamless shopping experience and respond to pressures from e-commerce-only businesses, which utilize a lower fixed cost profile to undercut the traditional operators.

Jill has a loyalty program that rewards customers with discounts, early access to sales, and special offers. This program is designed to build and retain a loyal customer base, contributing to strong engagement and recurring sales.

Jill competes with other women’s fashion retailers such as Chico’s, Talbots, and Coldwater Creek. Additionally, it faces competition from larger retailers like Nordstrom (JWN) and Macy’s (M).

Competitive Positioning

We believe the following factors are key reasons for the company’s poor top-line financial performance:

- Competitive Landscape – The apparel industry is highly competitive, with many brands catering to various customer segments. With the rise of e-commerce, Jill has faced increased competition that it has been unable to respond to, with heavy reliance on its brand (which has not worked).

- Brand Identity – Despite the no-nonsense, classic design approach, we suspect the need to refine its identity to better resonate with modern consumers is needed. This essentially diminishes its attractiveness as the business is facing the same trend/taste changes that the broader industry is.

Margins

Jill’s targeted approach (lucrative demographic) and brand development have allowed the business to generate impressive margins, with an EBITDA-M of 17%. This appears to reflect positive pricing action and reduced discounting, with GPM improving, as well as operational efficiencies as Management has sought to specifically reduce S&A.

This appears sustainable given the near-term resilience (discussed below), although we are hesitant given soft growth will always encourage increased discounting. The business could easily face a downward spiral with discounting and slow growth compounding to a lose-lose situation. Many apparel brands have suffered with this in the last decade and Jill does not benefit from operating a multi-brand approach.

Economic & External Consideration

Current economic conditions are potentially problematic for the business. With elevated interest rates and high inflation, consumers are reducing discretionary spending as living costs rise. The expectation is that Jill’s target demographic will be less impacted, however, we are still concerned that sustainable revenue growth in the short term is unlikely.

The takeaways from its recent quarterly results are:

- Revenue growth has ground to a halt, with its last 4 quarters being (1)%, +1.7%, (4.9)%, and (2.9)%. This reflects a prolonged period of reduced spending (coinciding with rising rates).

- EBITDA-M has remained surprisingly robust, suggesting (unusually) inherent interest is reduced rather than pricing necessarily being an issue.

- Margin improvement is attributable to operational improvement and strong inventory management.

- Store growth has been non-existent, implying little confidence in future growth by Management, particularly given the strong FCF (it can be funded if needed). This is disappointing to see given the weakness in same-store growth.

Balance sheet & Cash Flows

Management’s strong operational capabilities are reflected in its CCC, with a consistent decline YoY (collecting cash quicker), while also having a higher inventory turnover in arguably one of the most difficult quarters. This is supremely good and is reflected in the strong FCF.

This has allowed Management to deleverage the balance sheet (ND/EBITDA of 1.8x), creating the potential for future distributions via buybacks or dividends.

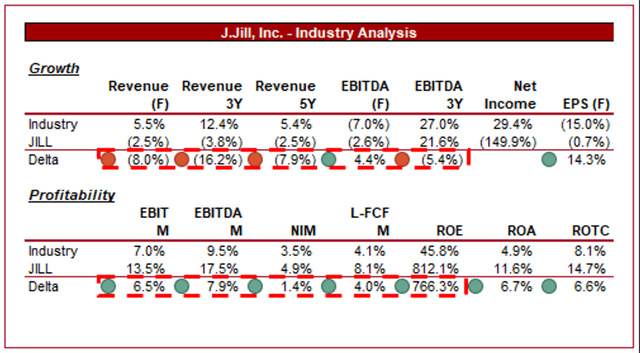

Industry analysis

Apparel (Capital IQ)

Presented above is a comparison of Jill’s growth and profitability to the average of its industry, as defined by Seeking Alpha (31 companies).

Jill performs respectably when compared to its peers. The company’s growth is a key area of concern, with a noticeable negative delta. This suggests a fundamental weakness in the business model, aligning with our prior analysis. The risk is that the company is losing market share despite maintaining (and in some cases improving) its margins.

Jill’s key value driver is its margins. The company is substantially above the industry average in every metric, with an EBITDA-M and FCF-M delta large enough to be sustainable in the medium term. This advantage is a reflection of its target market and premium model, allowing the business to price well.

Given the maturity of the industry, our preference is margins, as growth contributes to net gains. This said, we remain hesitant given the risks associated with margin erosion to maintain a positive growth trajectory.

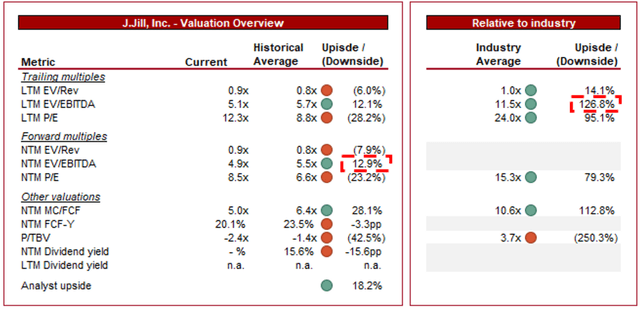

Valuation

Valuation (Capital IQ)

Jill is currently trading at 5x LTM EBITDA and 5x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average appears unreasonable in our view, primarily due to the margin improvement achieved and operational excellence, allowing for strong cash returns despite low growth, The lack of material revenue improvement is clearly a concern, however, this is partially offset by the margin improvement we feel. This implies the business is undervalued by c.12% if we assume parity is reasonable.

Further, Jill is trading at a 127% discount to its peers on an LTM EBITDA basis, 80% on a NTM P/E basis, and 113% on a NTM FCF basis. This is a wildly unjustifiable level in our view. This likely reflects investor hesitancy as to the future performance of the business if revenue continues to be a struggle to achieve. We agree with this concern as it is a slippery slope once margins start to erode alongside weak revenue growth. Further, TowerBrook also owns c.50% of the shares, likely seeking an exit at the “right” price.

Broadly, however, we do consider the business undervalued. a discount to its historical average is difficult to rationalize while the discount to its peers is far too big to reasonably utilize. This said, we do not think the stock is attractively priced, yet, due to macro conditions and the risk of margin erosion. We would be swayed if its NTM FCF yield exceeded the historical average level but this is not the case.

Final thoughts

Jill is the perfect example of carving out a niche to succeed in a highly competitive industry. Growth has suffered because of this, with its target market inherently limited and not growing at a substantial level. This does not mean the business is immune to trends, as our analysis suggests, which is disappointing to see (but the company cannot be blamed).

We do believe the company has attractive qualities, namely its impressive FCF, good brand visibility, and margin resilience. This said, we would like to see greater upside to justify the investment given the numerous risks associated with this highly competitive industry and current conditions. It is unlikely we will see positive price action in the near term, so patience around margin development could be beneficial.

Read the full article here