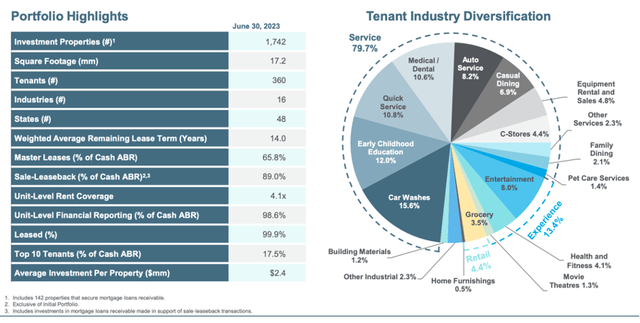

Essential Properties Realty Trust (NYSE:EPRT) is a net lease REIT similar to Realty Income (O). The REIT focuses on smaller single-tenant properties leased to service-oriented tenants, with an average asset size of $2-5 million. The small building focus is great because these properties are generally more fungible and easier to release or sell if need be.

EPRT

Sale leasebacks

Their strategy is quite unique in that they focus a lot on sale leaseback transactions. These are generally great for the landlord as well as the tenant.

Firstly, by selling the property, the tenant is able to raise capital to run its core business. This is especially valuable to companies below investment grade, which may have a hard time accessing capital, given the recent rise in interest rates and a tightening credit market.

On the other hand, this type of transaction is also great for the landlord, because they generally get very landlord-friendly lease terms. These include a long lease period of 20+ years, above standard rent escalations clauses that average 1.6% and financial reporting on a unit level, which allows EPRT to know the exact rent coverage in its properties.

Growth prospects

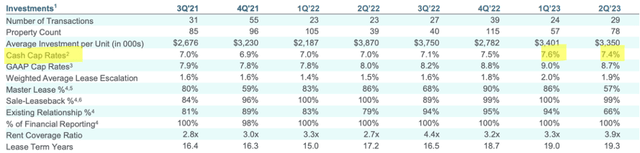

Beyond good lease terms, which the company has been able to lock in, sale leasebacks have also enabled EPRT to recently acquire properties at above market cap rates. This is because at times when the tenant needs capital, they might be able to sell for a lower price. Over the past two quarters, the REIT has locked in a handful of new properties at an average cap rate of 7.5% on a cash basis.

EPRT

Going forward, management expects cap rates to plateau around mid-7% for several quarters, before coming back down, so now is a really good time for the company to go shopping, especially when we consider its low cost of capital which stands at just 3.4%.

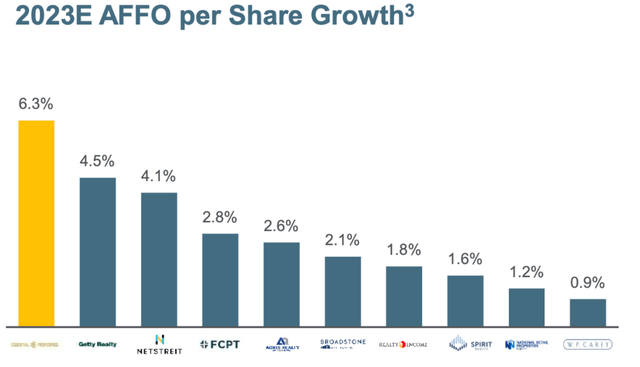

What sets EPRT apart from the competition is their forecasted growth. While established players, such as Realty Income or NNN REIT (NNN) are expected to see sub-2% AFFO growth, Essential Properties is guiding to 6.3% this year.

This superior growth is a direct consequence of their strategy, which results in higher-than-average rent increases, as well as access to cheaper properties for acquisition. Management has stated on previous earnings calls that they expect this edge over competition to diminish over time as more REITs focus on sale-leasebacks, but in the meantime, EPRT is well positioned to lock in great terms for years to come.

EPRT

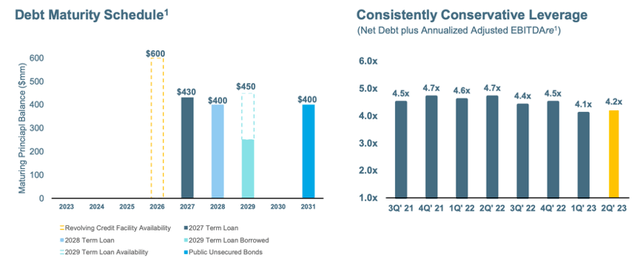

Future growth will be supported by a strong balance sheet with low leverage of 4.2x EBITDA, low cost of capital of 3.4%, and no debt maturities until 2026 when their revolving credit line matures. As such, EPRT’s interest rate risk over the next three years is very low, which positions it very well for a high interest rate environment. The company has about $800 million in liquidity which is the highest level ever – this is great because it will enable the company to go shopping for quality deals now, that prices are low.

EPRT

I realize that many investors look at REITs for their dividends. Historically, net lease REITs have been very rewarding on this front, with O and NNN have multi-decade track records of increasing their dividends. EPRT in particular pays a 4.8% dividend yield, supported by a very healthy 65% payout ratio. Going forward, I fully expect the dividend to grow at around the same rate as AFFO (about 5% per year).

Valuation

The stock currently trades at 14x FFO, which is below the historical average of 19x. Given the stock’s relatively short history, I don’t think the historical average is particularly useful, which is why I also include a 10-year average P/FFO of Realty Income of 19x and of NNN of 17.5x.

Relative to these two, EPRT is expected to grow higher but likely isn’t as high quality as O, which is why I see a fair multiple somewhere between the two, say 18x.

That leaves about 28% of upside from multiple expansion, on top of a nearly 5% dividend and about 5-6% AFFO growth.

FastGraphs

If EPRT can manage to re-rate to 18x FFO within two or three years, investors will earn double-digit returns.

Catalysts and risks

The question is what catalysts will be needed for this to happen. Well, for one, a decrease in interest rates would help significantly.

My base case is that the Fed will decrease rates somewhat over the next 12 months, either because they get inflation under control or because unemployment ticks up (the inverted yield certainly indicates that a recession is likely) forcing the Fed to reverse course. This would likely result in the double-digit upside we talked about being realized.

The risk, of course, is that interest rates stay higher for longer. In this case, I wouldn’t expect the multiple to decrease from today’s levels, but with a nearly 5% dividend yield, 5% FFO growth and a balance sheet with minimal interest rate risk, I think the REIT is relatively positioned to deliver positive returns even under this risk scenario.

Therefore, I rate EPRT as a BUY here.

Read the full article here