Intro

We wrote about Mercer International Inc. (NASDAQ:MERC) back in January of last year when we reiterated our belief that the pulp, timber & paper operator remained heavily undervalued. In fact, given how the company was just off the back of a strong earnings beat in its fiscal third quarter of 2021 and how ongoing acquisitions were adding value to the firm, we rated MERC a BUY at the time of writing. Shares at the time were trading at just under $12 a share and managed to surpass $17 a share (46% return) over the following eight months before we witnessed a cyclical top in August of 2022.

Since August of last year, however, the bears have been in full control as all we have seen over the past 13+ months is a sustained pattern of lower lows and lower highs. In saying this, shares have managed to remain above their June lows ($7.48 per share) so it will be interesting to see if the pulp manufacturer can now go on a long overdue cyclical uptrend. Mercer’s present implied volatility (October) comes in at an above-average 52%. This means the market expects a sizable move (either bullish or bearish) in Mercer over the next 12 months. Therefore, in order to ascertain which direction Mercer is more likely to trade over the next year or so, we will first consult the stock’s technicals and particularly Mercer’s volume trends in recent months.

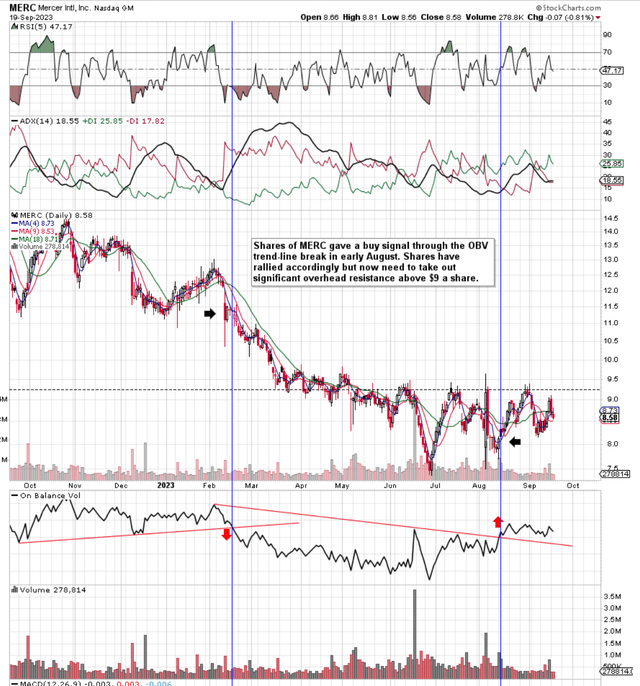

Volume Trend On Mercer’s Daily Chart

When studying consolidation patterns (which Mercer has been undergoing for many months now), the respective stock’s volume trends can give us insights into where shares may be headed over the near term. One of the easiest ways to follow a stock’s volume trend is through the use of the OBV indicator (On Balance Volume) where the trend of the indicator is the most important factor in its setup. As we see from the chart below, using trendlines in conjunction with the OBV line very often is a sound way to spot trend changes in the underlying. Furthermore, given that volume trends many times precede share-price action, it was encouraging to see that we had a bullish OBV trendline break in early August this year at about $8 a share. Since then, the share price has rallied accordingly but still remains below heavy overhead resistance just above the $9 a share level. Price would first need to clear this resistance point before entertaining any thoughts of initiating a fresh cyclical bull run.

Mercer International Daily Technicals (Stockcharts.com)

Profitability Headwinds

Although as mentioned, shares of Mercer printed their cyclical top in August of last year, earnings growth was the main precursor for the significant rally. Mercer earned $247 million in net profit for the year or $3.71 in earnings per share. Earnings growth, however, began to decelerate significantly in Q4 last year and this trend unfortunately has carried through into the first two quarters of this year.

Net earnings fell from a negative $30.6 million in Q1 of this year to a large -$98.3 million in the second quarter. However, management decided to record a non-cash $51 million impairment charge on the company’s inventory due to the significantly lower pulp prices in the quarter. Hardwood & softwood prices declined in China, the US & Europe as demand continues to take its toll on pulp markets.

Suffice it to say, the market needs to see a clear line of sight to higher pulp prices so the financials can change for the better on Mercer’s income statement. What the company can do internally is reduce its costs ( as well as capital expenditure spend) as much as possible while at the same time reducing inventory to remain as asset-light as possible in this present cycle. Then, externally, more ongoing third-party mill closures combined with better economic conditions, especially in China & Europe would really increase the demand side. In fact, green shoots are beginning to appear in the softwood segment with respect to how the supply of the same has been tightening.

Cheap Valuation But EPS Outlook Remains Weak

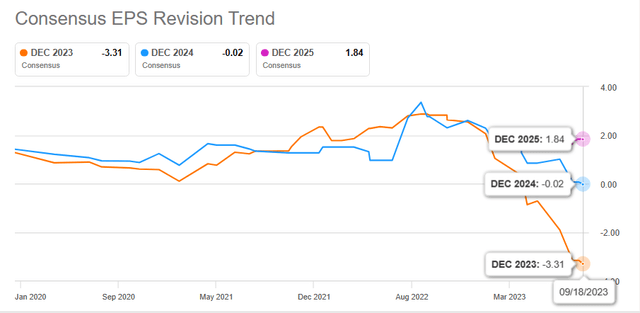

From a valuation standpoint, shares trade with a forward sales multiple of 0.29 and a forward book multiple of 0.89. Although these multiples come in well below Mercer’s historic averages, we must also remember that debt has been rising ($1.361 billion), the company as mentioned is not profitable and recently announced senior notes offering to hopefully bring in $200 million into company coffers. Furthermore, as we see below, forward-looking earnings estimates and revisions have been under pressure not only for the remainder of fiscal 2023 but also for next year where consensus believes at present that Mercer will struggle to make a profit. Suffice it to say, the below trends would have to change meaningfully for another cyclical bullish run to ensue in Mercer.

Mercer Consensus EPS Revision Trend (Seeking Alpha)

Conclusion

To sum up, although the shares of Mercer have been showing signs of encouragement on the daily chart, low pulp prices mean that management needs to reduce spending significantly in order to protect the company’s financials in earnest. The stock remains a Hold but needs to be watched accordingly. We look forward to continued coverage.

Read the full article here