By William J. Luther

The Federal Reserve’s Federal Open Market Committee (FOMC) voted to hold its federal funds rate target range at 5.25 to 5.50 percent on Wednesday. However, FOMC members also signaled that another rate hike is likely in the fourth quarter of this year.

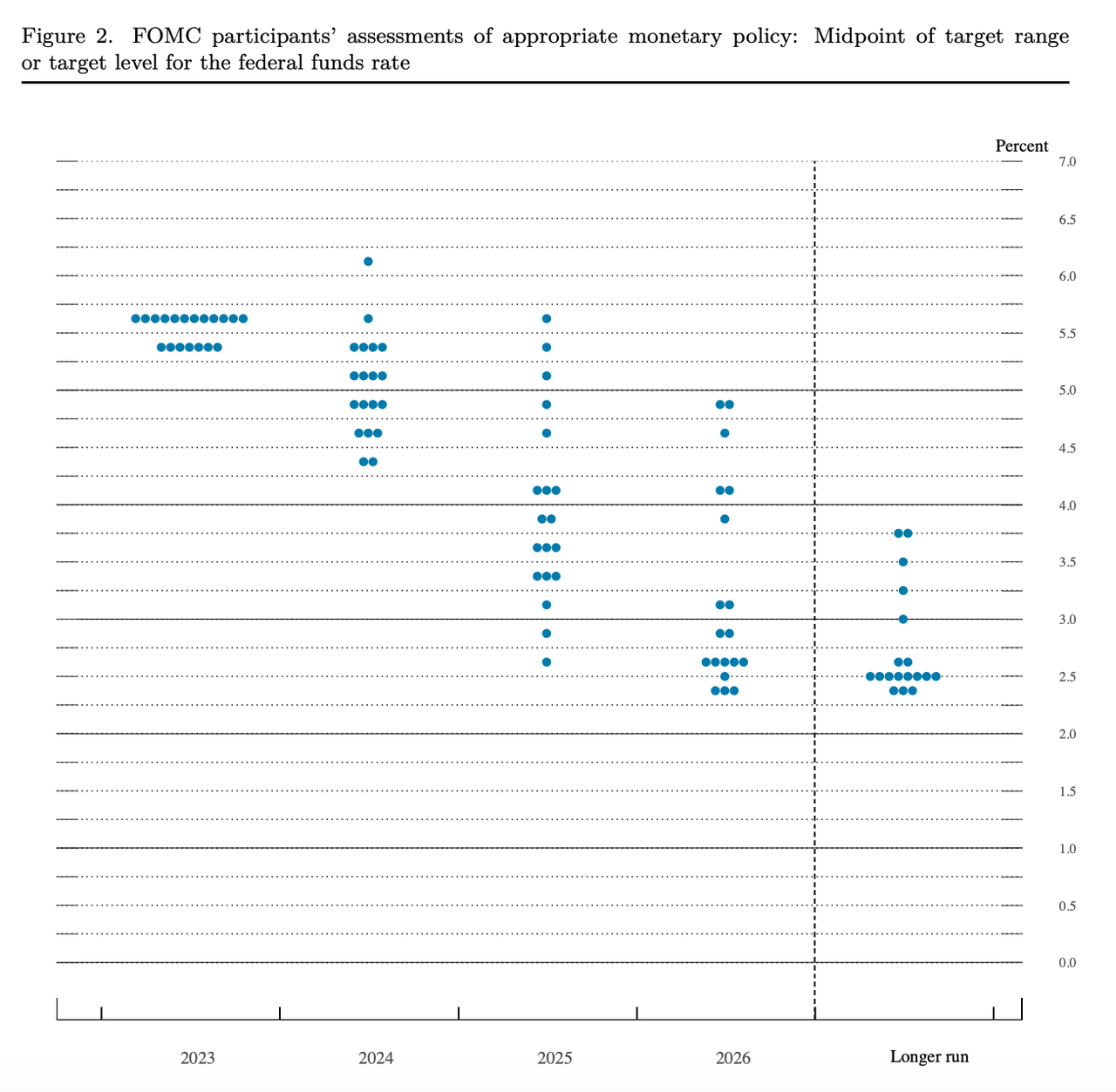

In the latest Summary of Economic Projections, twelve of nineteen FOMC members projected rates would fall between 5.50 and 5.75 percent by the end of 2023.

The remaining seven FOMC members projected rates would remain in the current 5.25 to 5.50 percent range. Only twelve members vote on the policy rate – the seven governors, the New York Fed president, and four of the remaining regional Reserve Bank presidents.

And we do not know what those specific twelve members have projected. Still, the latest projections suggest that another rate hike is on the horizon.

Ahead of this week’s meeting, several FOMC members warned about the risk of overtightening. Atlanta Fed President Raphael Bostic described monetary policy as appropriately restrictive.

“I think we should be cautious and patient and let the restrictive policy continue to influence the economy, lest we risk tightening too much and inflicting unnecessary economic pain,” he said.

Cleveland Fed President Loretta Mester took a more neutral position. “Future policy decisions will be about managing the risks and the intertemporal costs of over-tightening vs. under-tightening monetary policy.”

At the time of her statement, Mester said she still believed an additional rate hike will likely be needed, but that “it doesn’t have to be in September.”

Neither Bostic nor Mester are voting members of the FOMC this year.

Inflation has slowed considerably over the last year. The Personal Consumption Expenditures Price Index (PCEPI), which is the Fed’s preferred measure of inflation, grew at a continuously compounded annual rate of 3.2 percent over the 12-month period ending July 2023.

However, it grew faster over the first six months of that period (4.0 percent) than the last six months (2.5 percent).

The PCEPI for August 2023 has not yet been released, However, the Consumer Price Index, which was released last week, gives some insight into what one should expect. A surge in oil prices caused the CPI to grow faster in August.

Since monetary policy cannot increase the supply of oil, Fed officials should ignore the recent uptick in CPI inflation. But they may worry that inflation expectations will rise if they do not continue tightening in the face of an apparent reversal in the disinflation process.

“Energy prices being higher, that is a significant thing,” Powell said at the post-meeting press conference. “A sustained period of higher energy prices can affect consumer expectations about inflation. We tend to look through short-term volatility, and look at core inflation. So the question is how long are higher prices sustained.”

Core PCEPI has grown at a continuously compounded annualized rate of 3.8 percent year-to-date. It has grown at an annualized rate of 2.9 percent over the last three months.

The median FOMC member is projecting core PCEPI inflation will be 3.7 percent this year. Given that core PCEPI has grown slower in recent months and will likely continue to grow slower in the months ahead, it will probably be at or below 3.7 percent by the end of the year.

If core inflation is more or less on track, why are most FOMC members projecting another rate hike?

“What’s happened is growth has come in stronger, right, stronger than expected, and that’s required higher rates,” Powell said.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here