It’s no big secret; we’re not big fans of volatility-based income ETFs.

This includes the likes of QYLD, JEPI, and other funds in the ‘Enhanced Income’ category.

Many flock to these covered call strategies as a way to increase their monthly income distributions, but as we’ve explained before in articles like “QYLD: The Yield is a Mirage“, and “QYLD: Substandard Returns Set To Continue“, these funds hurt long term shareholder value by mechanically selling calls and increasing their holdings’ underlying cost basis – not a recipe for long term success.

TLTW, a bond Buy-Write fund, has historically seemed to be the best ticker in this category, because the underlying bonds in the fund are less volatile and should (in theory) trigger less permanent loss as a result of the fund’s underlying strategy.

That said, almost all income funds on the market today seem to have some significant drawback that makes the income seem unattractive or not worth the risk.

That is, except for NYSEARCA:SVOL.

SVOL, the Simplify Volatility Premium ETF, is a short volatility ETF that seeks to generate significant income off of the back of a unique volatility strategy that we prefer considerably vs. other covered-call based methods, like the one JEPI uses.

Today, we’ll break down how SVOL works, explain the associated risks, and summarize why we think this unique ETF deserves a spot in your portfolio.

How It Works

For those who are unaware, SVOL is an income-oriented ETF that sells VIX futures as its primary way of generating revenue.

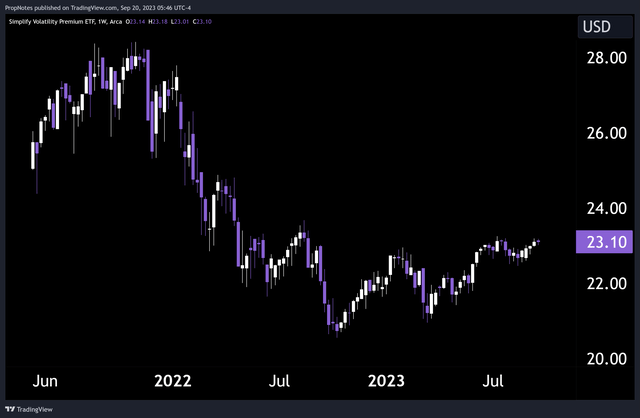

Here is how the ETF has performed since inception, not counting distributions:

TradingView

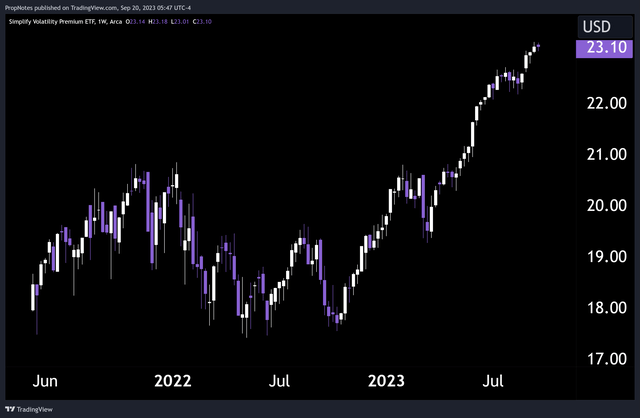

Here is the long-term performance of the ETF since inception, inclusive of distributions:

TradingView

As you can see, income plays a big part in the total returns of the ETF – a characteristic it shares with the other aforementioned enhanced income ETFs.

However, the fund generates income in a much different way.

Selling VIX futures is a unique strategy with a unique risk profile.

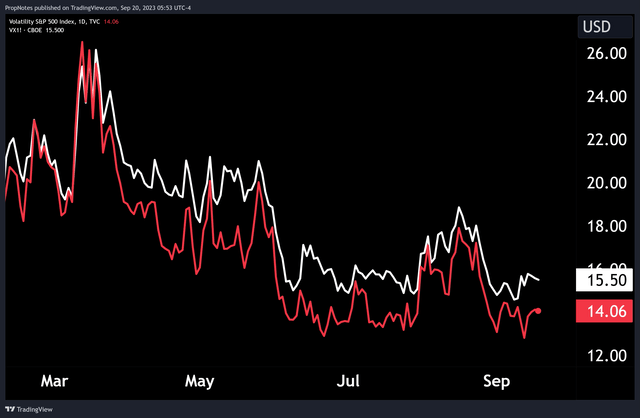

The underlying strategy of SVOL looks to take advantage of a big discrepancy in the volatility markets; the fact that VIX futures are almost always in Contango.

In the real world, this means that VIX futures are almost always priced higher than the VIX itself. Visually, you can see this below, where the red line is the VIX, and the white line is the front month VIX future:

TradingView

The reasons for this premium are many, but it basically has to do with the fact that VIX futures are a traded instrument, and those with exposure to it are always at risk of the VIX exploding in value, and so the fair value of VIX futures has to bake in this possibility, thus distorting price higher.

The VIX, however, is just the VIX, which means that most times it will trade lower than the futures, but occasionally it will spike up above them. This is the risk inherent in the asset class, simply due to the nature of fear and panic itself – it comes in clusters.

Practically speaking, though, it means that the ETF is selling futures at the white line and buying them back (letting them cash settle) at the red line. When done over and over, this produces profit when the VIX is flat or going down.

Because the VIX is mean reverting, this is what happens most of the time.

Risks

But what about when the VIX goes up, or explodes higher like in 2018 or 2020 when many short-vol funds like XIV blew up?

Diesel, a fellow SA contributor, did a great breakdown on how the fund would perform in a worst-case scenario. Definitely check that out if you’re interested in the math.

However, in short, the fund does well when volatility drops, stays flat, or spikes significantly. The only situation where it loses over a longer period are when volatility remains elevated for a while – like in 2022:

“What would happen if VIX were to suddenly jump to 20 overnight? This would result in a NAV drop of 6% for SVOL which isn’t bad considering VIX is almost doubling overnight in this scenario (from ~13).

What if VIX climbs to 30 overnight? We’d see the fund lose about $59 million of NAV or 15%. It might sound scary but VIX rarely climbs from 13 to 30 overnight and the fund still seems to be far from being blown up.

[What about if the] VIX suddenly jumps to 40 overnight? VIX 50 options will jump from 29 cents to $2.05 in value because IV of VIX itself will also rise significantly. This softens to blow by quite a lot and the fund only loses 18% in NAV.

What happens if VIX quickly jumps to 80 like it did in March 2020? The fund loses $330 million from its futures contracts but gains a whopping $934 million from its VIX call options which means a gain of $604 million or 150%.”

You may have noticed in the quote above the mention of options – and this brings us to the best part of this ETF: risk mitigation.

In short, where other vol funds expose investors to black-swan events, SVOL hedges the downside.

The return profile of most volatility selling strategies is similar – many small wins followed by the occasional big loss. In some cases, a loss big enough to wipe out everything (as was the case with XIV).

However, SVOL takes some collected cash premiums and re-invests them into VIX call options, which creates a ‘U’ histogram shape of returns.

On the left side of the ‘U’, when volatility is flat or goes down, SVOL makes money. On the right, when the VIX explodes higher, SVOL’s hedge makes more money than its short futures position loses.

Thus, the only market type where SVOL suffers in is one where volatility stays persistently high or increases slowly – this is the bottom bit of the ‘U’ distribution. In the business, a return profile like this is called “Convexity”.

Given that the final scenario is not how markets work typically, as spikes in volatility followed by slow ‘come-downs’ are most common, SVOL stands to do well in almost all market environments; exactly the opposite of other income instruments like QYLD or JEPI.

Finally, SVOL only uses about 25% of the fund’s assets to short this market. The remaining capital is held in bonds and cash, which provides a significant buttress against big losses. These are also assets that should see a big bid come into them in a black-swan scenario where the short VIX futures position gets killed.

Summary

All in all, SVOL is a great instrument for income seekers sick of the mechanical, suboptimal call-selling strategies found in other major income funds. Most investors may not be familiar with trading volatility as an asset class, but this fund does a good job bringing the benefits of it to the masses in a relatively low-cost package.

If you’re looking to add another asset class or buttress your income, you could do a lot worse than SVOL.

Cheers!

Read the full article here