By Warren Patterson, Head of Commodities Strategy

Tighter balance supports the move in oil

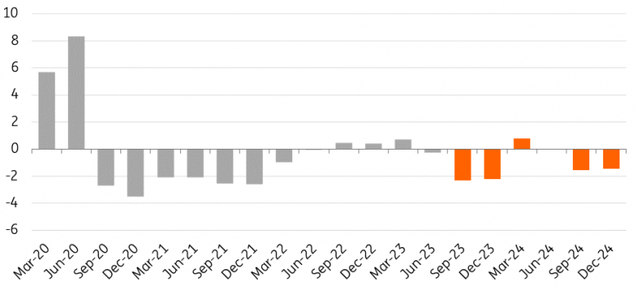

OPEC+ supply cuts have had their desired effect on the oil market – at least from OPEC+’s perspective, though less so for consumers. The additional voluntary cuts from Saudi Arabia, which have been extended through until the end of this year, have ensured that the market will remain in deep deficit for the remainder of 2023. This should keep both the flat price and timespreads well-supported.

The move in oil prices is well-telegraphed. However, getting less airtime is the move that we have seen in the timespreads. The prompt ICE Brent timespread widened to a backwardation of more than $1.40/bbl at one stage this week, up from around $0.60/bb at the start of the month, whilst the December 2023 – December 2024 spread is edging closer towards $10/bbl. The deep backwardation in the forward curve only reinforces the tightness in the physical market.

As things stand, there is little relief for the market in the short term, with the deficit environment set to persist through year-end. Our balance shows a deficit of more than 2MMbbls/d through the fourth quarter of this year. This tightness, along with strong refinery margins (largely a result of tightness in middle distillates), suggests that oil prices are likely to see further strength in the short term. Assuming OPEC+ doesn’t budge with its supply cuts in the near term, it is only a matter of time before Brent breaks above $100/bbl, given the scale of the deficit. However, we do not believe such a move would be sustainable, which is why we are holding onto our current forecast for Brent to average US$92/bbl over the fourth quarter of this year.

Oil market in deep deficit for remainder of 2023 (MMbbls/d)

ING Research, IEA, EIA, OPEC

Pressure on OPEC+ likely to grow

The reason we are reluctant to revise higher our oil forecasts is mainly due to the growing political pressure that OPEC+ is likely to face if prices continue to strengthen. OPEC historically always said that its goal is to stabilise markets and that the group does not target certain price levels. Saudi Arabia’s energy minister this week repeated these comments at a conference in Canada. However, with a deficit of more than 2MMbbls/d and prices approaching $100/bbl, it is difficult for the group to make these claims when OPEC+ output is more than 3.5MMbbls/d below target production levels.

Governments around the world will likely become increasingly concerned about inflationary pressures once again due to the strength in oil, and therefore likely to ask OPEC to open the taps a bit more. In addition, there are elections in two key oil-consuming countries next year – the US and India – which suggests possibly even more pressure from these two governments.

OPEC+ will also want to be careful about overtightening the oil market. They will be shooting themselves in the foot if they push prices to levels where we start to see an increased risk of demand destruction. Already, demand growth in 2024 is expected to slow to around 1MMbbls/d from around 2MMbbls/d this year due to expectations of weaker GDP growth. Higher oil prices could mean we see even more modest demand growth.

OPEC+ will continue to review supply cuts on a monthly basis, so we could very well see the group – or at least Saudi Arabia – gradually ease its additional voluntary cuts this year, which would help take some pressure off the market.

Unfortunately, the market will have to rely on action from OPEC+. The lack of drilling activity in the US means we are seeing only modest supply growth from the US, and not enough to offset the large deficit forecast. The US Energy Information Administration (EIA) sees US crude oil output growing by less than 70Mbbls/d between August and the end of this year. It’s difficult to see the US government tapping into its strategic petroleum reserves (SPR) after significant drawdowns last year left SPR at its lowest levels since 1983.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more.

Original Post

Read the full article here