Ytterbium: IONQ specializes in utilizing trapped ion qubits formed from ytterbium, a rare-earth metal isotope.

Capital markets have been on a wild ride over the last few years. And that includes 2023 with interest rates and high-growth stocks both rising rapidly. In this report, we review the current macroeconomic environment, share data on over 50 top growth stocks (ranked by revenue growth rates, among various other important metrics), and then review three names from the list that are particularly interesting and worth considering. We have a special focus on quantum-computing company IonQ (NYSE:IONQ), including its business, market opportunity, financials, valuation, risks and our strong opinion on investing. We conclude with a critical takeaway about investing in these select top growth stocks in the current market environment.

The Current Macro Environment: Interest Rate Drama

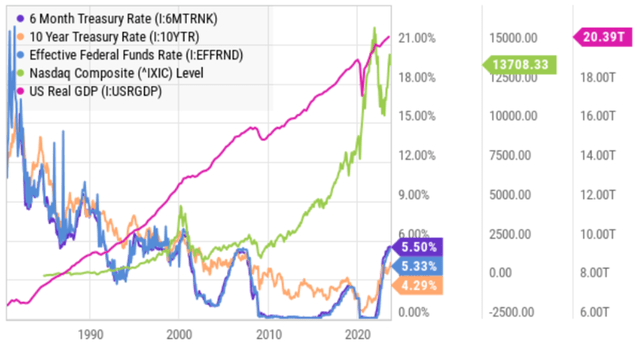

As you are likely aware, interest rates have risen rapidly over the last two years (as the fed attempts to undo that massive inflation they helped to create in the first place though pandemic stimulus). Of course low interest rates help the economy grow (because it becomes less expensive to borrow money to fund growth) and higher interest rates slow economic growth (because it makes funding growth more expensive). This was a huge factor in fueling the pandemic bubble among growth stocks in particular, and then bursting that bubble when rates first started to rise so rapidly, as you can see in the chart below.

YCharts

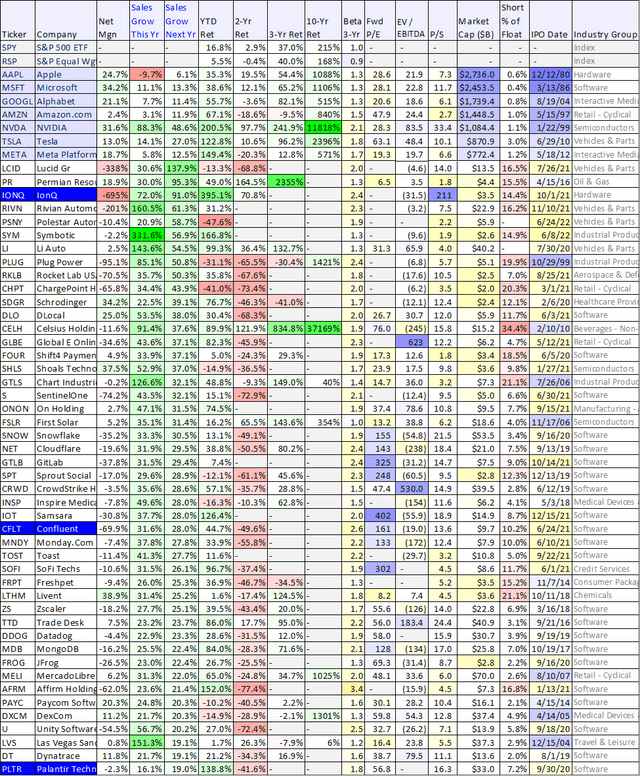

This year, growth stocks have rebounded hard since the pandemic bubble burst, but many of them are still trading dramatically lower than they were just two years ago, as you can see in the table below.

50 Top Growth Stocks, Ranked

The following table includes data on over 50 top growth stocks, ranked by revenue growth rates for both this year and next year. You probably recognize a least a few of your favorites on this list.

Data as of Friday’s close 15-Sep-23 (source: StockRover)

(AAPL) (NVDA) (TSLA) (META) (CELH) (SNOW) (NET) (SOFI) (TTD) (DDOG) (MELI) An extended and downloadable version of the table is available here.

The above table includes stocks with high sales growth expectations (for this year and next). And for reference, the 7 mega-caps are also included at the top, as well as the S&P 500 (SPY) and the “equal weighted” S&P 500 (RSP) to make it more clear what a huge impact on the S&P 500 the 7 mega-caps strong performance has had on this index this year. Beyond this, the companies are ranked by expected sales growth for next year.

The table also includes data on bottom-line profitability (net margins), valuation (such as forward P/E, P/S and EV/EBITDA) as well as various other metrics you may find helpful when considering opportunities for further research.

Busted Pandemic IPOs

Another metric we find interesting (in the above table) is IPO date. This stands for initial public offering date, and it represents the date each company first began trading in the public markets (technically, some of them came public via SPAC deals, but I digress). IPO date is important because companies (and investment bankers) typically try to bring companies public at a time when market valuations are high (because they can get more money for selling shares publicly at that time). And that is exactly what happened, as you can see many of the companies that went public in 2020-2022 have since fallen in share price dramatically since their IPO’s. If you are the company or the investment banker that underwrote the deal—nice job (you made a lot of money), but if you bought during the pandemic bubble—my apologies (you’re probably down big on your purchase). And if you are looking to invest in any of these companies now—good for you (prices are a lot less expensive than they were two years ago—see 2-year total return column, above).

And for reference, each of the 3 top-growth stocks we review in the remainder of this report are pandemic-era IPOs. We have a special focus on quantum computing company, IonQ, so let’s start with that one.

IonQ Overview:

IonQ

This may sound like science fiction, but IonQ harnesses the power of atomic ions found in nature to develop quantum computing systems that are widely regarded as surpassing traditional computer technologies in both quality and scalability. Founded in 2015 and first trading publicly in late 2021, the company is relatively small ($3.5 billion market cap), but growing rapidly (see sales growth rate in our earlier table) and supported by very large long-term secular disruption opportunities.

What is Quantum Computing?

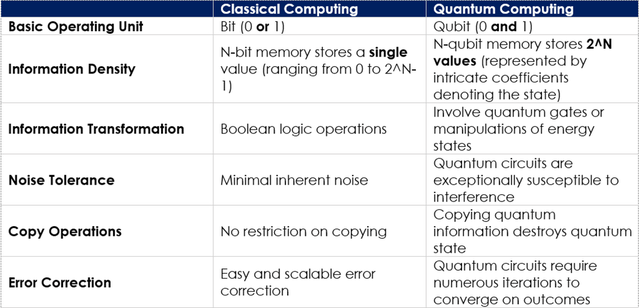

Quantum Computing is a swiftly emerging revolutionary technology harnessing the principles of quantum mechanics to tackle contemporary intricate challenges that classical computers are incapable of handling. While conventional computing relies on bits, denoted as 0 (“off”) and 1 (“on”), to store data, quantum computing operates through quantum bits (qubits). These qubits, being fundamental units, can exist in a state of both 0 and 1 simultaneously, a phenomenon known as superposition. This unique attribute enables quantum computers to effectively address a range of complex issues that traditional computers would struggle to solve or would require an impractical amount of time – examples include simulating quantum systems, performing number factoring for decryption, and solving complex optimization problems.

The Quantum Daily Source: The Quantum Daily

IonQ Background and Revenue Sources:

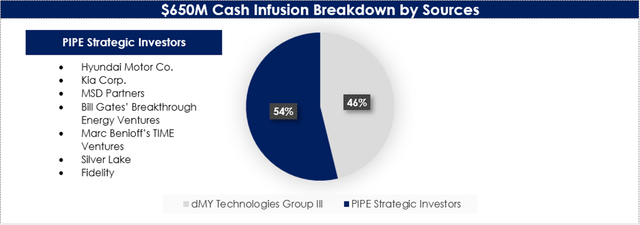

Founded by its current CTO and Chief Scientist, Jungsang Kim, along with Dr. Chris Monroe in 2015, IONQ emerged after a collective research journey of over two decades in the field of quantum physics. The company secured $2M in initial funding from New Enterprise Associates as seed capital, followed by an additional $20M infusion from prominent backers like Google Ventures (GOOGL) and Amazon Web Services (AMZN). Under the leadership of its current President & CEO, Peter Chapman, IONQ garnered an additional $55M in investment from notable stakeholders, including Samsung, Lockheed Martin (LMT), Airbus Ventures, Bosch, HP, and Mubadala. IONQ chose to go public in October 2021 by engaging in an unconventional route through a Special Purpose Acquisition Company (“SPAC”). This strategic move entailed a merger with dMY Technologies Group III, a SPAC. The company received $650M in cash and 64% ownership of the newly combined entity.

Forbes Source: Forbes

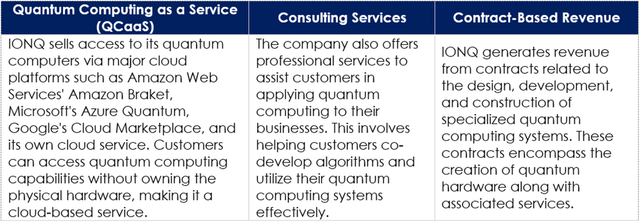

The company generates revenue through various avenues related to quantum computing and its services. Below is a breakdown of the revenue sources.

Quarterly Report Source: 10-Q

Leveraging Trapped-Ion Qubits Touted for its Low Error Rate

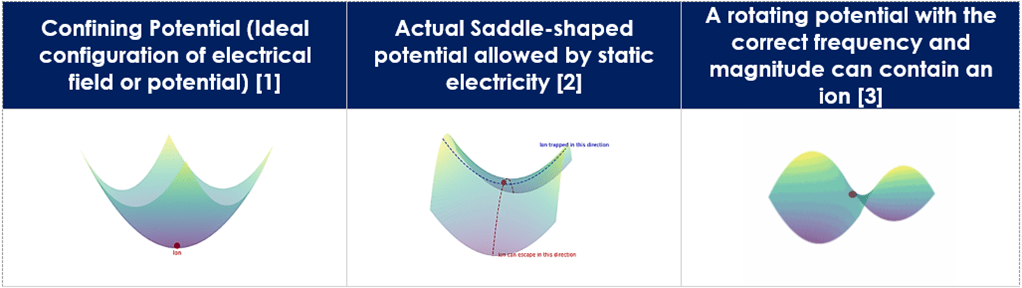

Numerous quantum computing technologies are currently available in the market, encompassing superconducting, photonics, silicon-based, spin qubits, trapped ions, and various others. IONQ specializes in utilizing trapped ion qubits formed from ytterbium, a rare-earth metal isotope. To understand trapped ions, it’s essential to grasp the concept of ions. Ions are atoms that have undergone electron loss or gain, resulting in an electrical charge. Due to their charge, ions prove challenging to confine using static electric fields, as they consistently migrate between areas of high and low potential based on their charge (see chart [2]). Trapped ion technology employs an oscillating electric field to confine ions within a Paul trap (see chart [3]). Through this oscillating electric field, stable equilibrium zones are generated, effectively containing the ions. These oscillating fields can be finely adjusted to create forces countering the ions’ movement, thus counteracting their inherent tendencies. Once trapped, the ions can be cooled and manipulated into distinct quantum states using lasers emitting various frequencies.

Pennylane Source: Pennylane

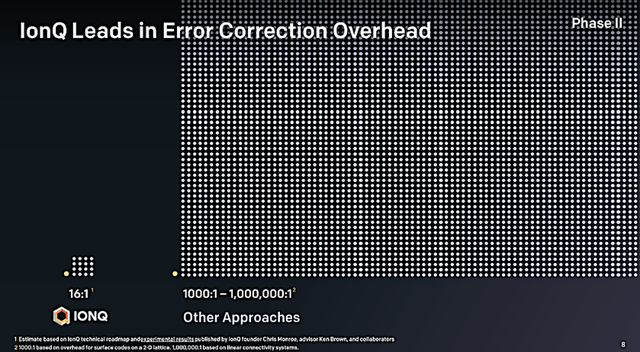

Trapped-ion qubits offer various advantages compared to other quantum technologies. These include extended periods of coherence, the ability to individually control each qubit, accurate high-quality operations, and more. According to the company’s investor presentation, their method of error correction is particularly efficient. The company only needs 16 unstable qubits, known as “dirty” qubits, to produce a single error-corrected qubit. In contrast, other quantum systems require thousands of these unstable qubits to achieve the same error correction. It’s important to note that qubits are highly sensitive to their surroundings and can easily lose their special properties (like being both “0” and “1” at once) due to factors such as temperature, electromagnetic signals, and other interactions.

Investor Presentation Source: Investor Presentation

Leading in a Market that is Nascent and Poised for Significant Expansion

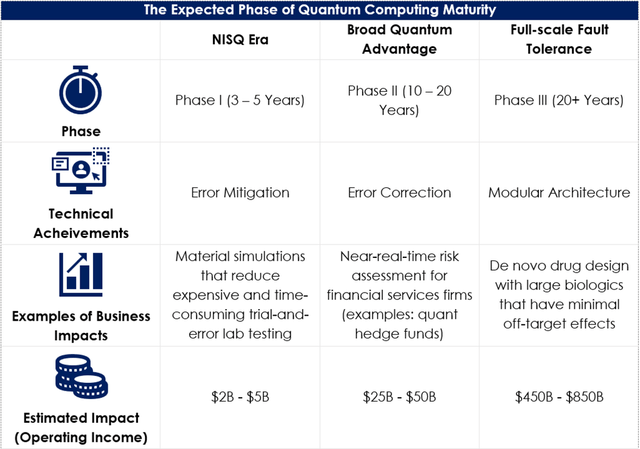

Based on the 2019 study conducted by BCG titled “Where will Quantum Computers Create Value – and When?”, the present stage of quantum computing is defined by the era of Noisy Intermediate-Scale Quantum (NISQ) devices. These devices possess the capability to execute practical and distinct operations, although they do so at a notable error rate that hampers their functionality. Over the forthcoming 10 to 20 years, this period is projected to witness widespread quantum advantage. During this phase, quantum computers are poised to exhibit superior performance, predominantly in industrial applications of significance. Following the span of broad quantum advantage, the trajectory of quantum computing is anticipated to transition into the era of full-scale fault tolerance. In this phase, quantum devices are set to become mainstream and are projected to create significant value. In fact, as per the report, quantum computing is expected to add $450B – $850B incremental operating income, evenly split between incremental annual revenue streams and recurring cost efficiencies across a wide variety of industries by 2050.

BCG Source: BCG

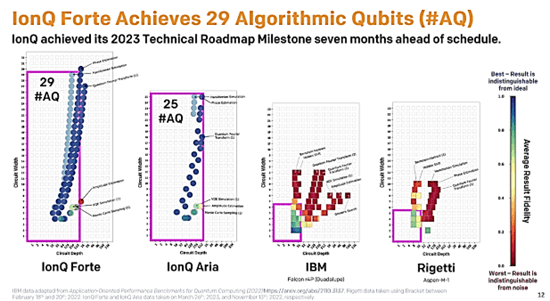

Hitting Technological Milestones Earlier than Expected

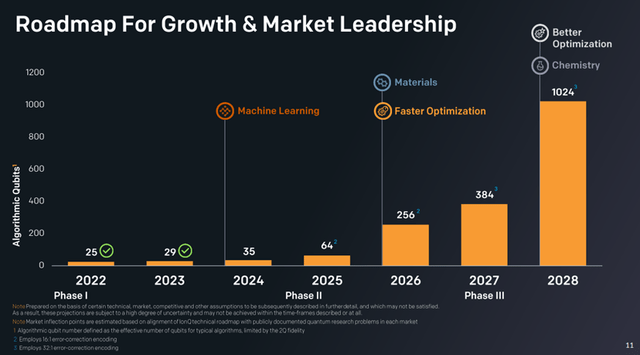

Since going public in late 2021, the company has significantly ramped up its investments in research and development. This strategic maneuver has led to a noteworthy improvement in the precision and dependability of its quantum systems, as gauged by Algorithmic Qubits (AQ). In the year 2022, the company effectively accomplished its goal of reaching 25 AQ by unveiling IonQ Aria. Interestingly, it surpassed its 2023 technical roadmap target by seven months by introducing IonQ Forte, featuring 29 AQ. It is worth noting that each additional AQ roughly equates to a doubling of valuable computational capacity. The company’s subsequent pivotal technical objective is to reach 35 AQ, a task that will progressively become more demanding and costly for its clients to simulate on conventional computers. As such, it is highly likely that as the company continues to hit its forthcoming milestones, there will likely be an increase in hardware revenue, as customers choose to purchase quantum systems rather than utilizing their classical computers to run simulations on the cloud. To address potential future demand, the company will open the first quantum computing manufacturing facility in the US, supported by the US Congressional delegation from Washington state.

“Our next major technical milestone is achieving 35 AQ, which is particularly significant. At 35 AQ, simulating the operations of quantum algorithms using classical hardware can become exceedingly challenging and costly. We expect at 35 AQ, some customers will have an increasingly clear business case for running models on actual quantum computers, rather than attempting to simulate those models with classical computers.” – Peter Chapman, President & CEO

Investor Presentation

IonQ Forte, initially limited to select partners, has now been expanded for use in both commercial and government contexts, alongside other systems such as IonQ Aria (#AQ 25) and IonQ Harmony (#AQ 11). The company’s partners are actively implementing algorithms or have signed agreements to utilize IonQ’s quantum platform for algorithm executions in the future.

Press Release

Strong Top-Line and Bookings Growth, Indicating Robust Demand Pipeline

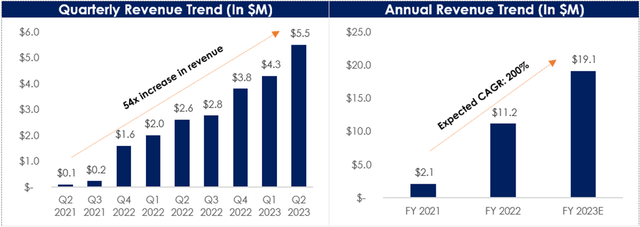

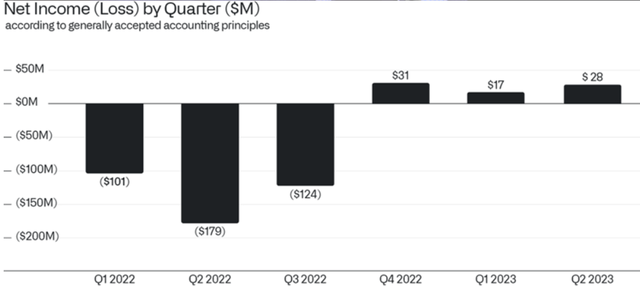

As a nascent disruptor in its initial phases, IonQ has witnessed a strong upward trend in revenue over the past three years, aligning with the company’s initiation of commercial activities. In Q2 2023, the company reported $5.5M in total revenue as compared to $2.6M in Q2 2022, translating into a YoY growth of 112%. The driving forces behind this expansion are the robust demand for the company’s quantum systems delivered through cloud technology, coupled with the company’s ability to achieve technological milestones ahead of schedule, leading to the earlier execution of customer contracts.

Company Filings

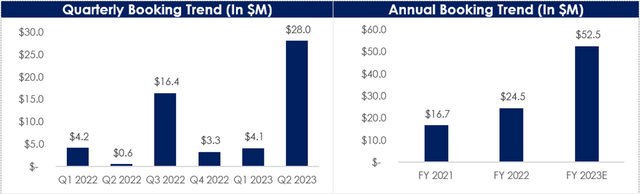

IonQ achieved $28M in new bookings in Q2 2023, bringing total bookings to $32M on a YTD basis and total cumulative bookings to $100M within the first three years of its commercialization journey. Given rising interest in its systems, IonQ has revised its guidance for both revenue and bookings. The company’s revised projections anticipate revenue ranging from $18.9M to $19.3M, while bookings are expected to fall within the range of $49M to $56M in 2023.

Company Filings

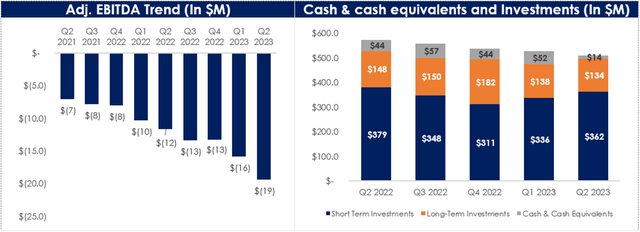

Navigating Early-Stage Growth and Investments via Robust Balance Sheet

Similar to other rapidly growing companies in their early stages, IonQ is grappling with challenges related to achieving profitability. In Q2 2023, the company registered an adjusted EBITDA loss of $19.4M, a notable increase from the $11.6M adjusted EBITDA loss reported in Q2 2022. This loss can be attributed primarily to a significant surge in research and development expenses, which is justifiable given the company’s positioning within the rapidly evolving quantum computing landscape. Despite these losses, we believe that IonQ boasts a robust financial position capable of supporting its internal investments. By the end of Q2 2023, the company had amassed $509M in cash, cash equivalents, and investments. Assuming that IonQ continues to report adjusted EBITDA losses of $62 million on a TTM basis in the future, the current cash reserves of $509M are deemed sufficient to sustain these losses for the subsequent 8 years.

Company Filings

Valuation

So far this year, IonQ’ stock has seen a substantial increase of around 395%, attributed to its endeavors in commercialization and successful partnerships. However, it is still hovering at a discount to its peak value in late 2021. Due to its nascent developmental phase, the conventional approach of evaluating the company’s valuation through market multiples is inappropriate. Despite that, considering the potential of the quantum computing market, we believe that the company’s market capitalization of $3.5B could ascend further as it attains successive technical milestones, improving the quality of its quantum computing systems.

IonQ Share Price (Seeking Alpha)

Risks

Customer Concentration Risk: The majority of the company’s revenue comes from three significant customers, i.e., those contributing over 10% of the total revenue. While concentration risk is worth keeping an eye on, we believe that it will diversify as quantum computing market moves into the phase of widespread adoption.

Intense competition: IonQ operates within a fiercely competitive market landscape. Its rivals include industry giants like IBM (IBM), Google (GOOGL), Honeywell (HON), Intel (INTC), and Microsoft (MSFT). Moreover, it faces competition from emerging contenders like Rigetti (RGTI), Xanadu, D-Wave Systems (QBTS), and Quantum Computing Inc. (QUBT). Despite the intense rivalry, IonQ’s quantum technology based on trapped ions stands out, boasting numerous advantages over alternative approaches, particularly in terms of scalability and fidelity.

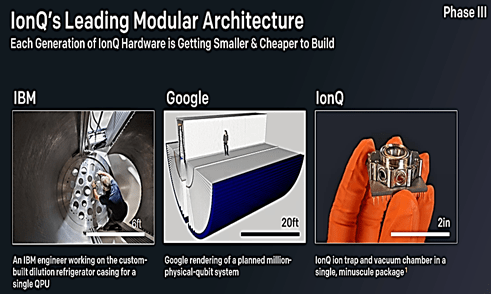

The company’s most recent quantum systems, the #29 AQ IonQ Forte and #25 AQ IonQ Aria, clearly outperform IBM’s Falcon r4P (Guadalupe) and Rigetti’s Aspen-M-1 in terms of quantum advantage and quality. This is evident from the comparison provided below. Furthermore, IonQ’s utilization of trapped-ion technology allows each successive hardware generation to become more compact and cost-effective to produce. This provides the company with a significant edge over the hardware development of competitors like IBM and Google.

Investor Presentation Investor Presentation

IonQ Bottom Line:

IonQ stands out with its trapped-ion quantum technology, strategically placing the company within the fast growing quantum computing market, which is currently in its early phase of expansive development. As a pure play quantum computing entity, backed by co-founders with substantial expertise in quantum research spanning several years, the company possesses a distinctive advantage over its competitors. This advantage was evident through the company’s recently unveiled IonQ Forte that excels in both quality and scalability relative to other available systems in the market. Considering the substantial market potential and significant strides already achieved, we perceive this as a promising prospect for patient investors who believe the notion that “quantum computing is the future.”

Confluent (CFLT):

Confluent![]()

Switching gears to another top growth stock, Confluent is on a mission to “set data in motion.” The company provides a data platform which is designed to help businesses manage and process data in real-time from various sources. For some perspective, traditional database technologies typically focus on storing and retrieving data that is at rest, meaning data that has been persisted to disk or stored in databases. In contrast, Confluent’s platform is built around Apache Kafka, an open-source distributed streaming platform, which enables the processing of data in motion or data streams. This becomes extremely important considering the explosion of cloud data in recent years, especially with regards to new Artificial Intelligence opportunities and demands.

Confluent has plans to integrate its platform with popular AI systems, further expanding its product offerings and strengthening its position in the industry. The shares currently trade at only a fraction of their 2021 IPO price, and considering the very high growth rate (see earlier chart) and large total addressable market, we believe Confluent is worth considering. We recently wrote up Confluent in great detail (i.e. business model, market opportunity, financials, valuation, risks) in this report, and if you are a long-term investor that can handle a healthy dose of high volatility, the shares are worth considering.

Palantir (PLTR):

Palantir Palantir Share Price (Seeking Alpha)![]()

Palantir is a great example of a busted-IPO stock that has continued to make dramatic growth progress despite the steep post-pandemic share price declines. Palantir is a big-data software company previously focused on government clients, but has expanded very successfully into commercial clients in recent years. And now most recently, the company’s Artificial Intelligence Platform (“AIP”) has opened a new wave of very high growth opportunities for years to come. Here is what CEO Alex Karp had to say about it in his most recent shareholder letter:

“The demand for AIP is unlike anything we have seen in the past twenty years. We are currently in discussions with more than three hundred additional enterprises to deploy AIP within their organizations, all of which are searching for an effective and secure means of adapting the latest large language models for use on their internal systems and proprietary data.

We have built the integration platform that they require, and the traction we are seeing, only months after its release, has been transformative for our company.”

Now trading at 16.3x sales, and with a very healthy double digit growth rate (see table above), with a large total addressable market (not to mention a positive net margin in each of the last three quarters), Palantir is an attractive long-term growth stock.

Palantir Shareholder Letter

Palantir is one of those names where if you can drown out the constant drumbeat of volatility and naysayers, the shares can be trading dramatically higher in the years ahead. We currently own shares, and have no intention of selling.

The Bottom Line

As you are likely aware, markets have been particularly volatile in recent years. And although top growth stocks have performed very well this year, many of them are still well below their pandemic-era highs. There is certainly no guarantee that any of these stocks won’t revert dramatically lower again (especially considering the ongoing macroeconomic dynamics). However, over the long-term, some of these opportunities are particularly compelling.

Most importantly, it’s critical for you to select only investment opportunities that are consistent with your personal situation and individual goals. For example, if you are a volatility-averse income-focused investor, don’t go dumping your nest egg into high-growth stocks. But if you do have a long-term horizon (and a strong stomach for volatility), select names from this report (such as the three we highlighted, IonQ, Confluent and Palantir) have the potential to go dramatically higher in the years ahead. Disciplined, goal-focused, long-term investing continues to be a winning strategy.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here