Greif (NYSE:GEF) offers industrial packaging products worldwide. GEF recently announced disappointing Q3 FY23 results. I will analyze its Q3 FY23 results in this report. Its valuation seems high, and the technical chart is bearish. I think we might see volatility in the stock price in the coming times, and I don’t see the company giving any returns in the short term. Hence, I assign a hold rating on GEF.

Financial Analysis

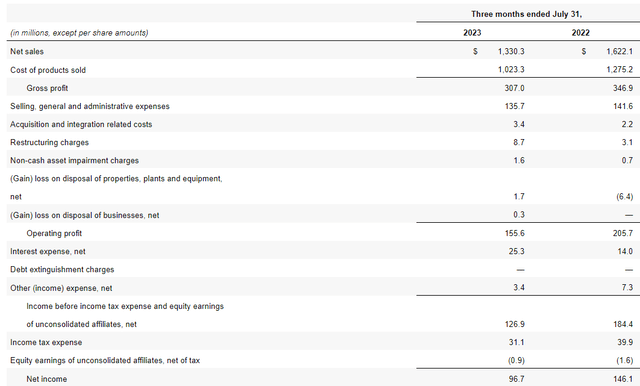

GEF recently posted its Q3 FY23 results. The net sales for Q3 FY23 were $1.3 billion, a decline of 18% compared to Q3 FY22. Its global industrial packaging and paper packaging & services segments underperformed, leading to a decline in sales. The sales from the global industrial packaging segment declined by 16% in Q3 FY23 compared to Q3 FY22. The average selling prices in this segment were 7.4% lower than in Q2 FY22, which I think was the main reason behind the underperformance. The sales from the paper packaging & services segment declined by 20.6% in Q3 FY23 compared to Q3 FY22. The average selling prices in this segment were also lower, which led to a decline in sales. The average selling prices in this segment declined by 5.9% in Q3 FY23 compared to Q3 FY22.

GEF’s Investor Relations

Due to a decline in sales, its gross profit and net income also declined. The gross profit and net income declined by 11.5% and 33.8% in Q3 FY23 compared to Q2 FY22. The Q3 FY23 result was disappointing and fell short of market expectations. When compared to FY22, they are much behind in FY23. By the end of Q3, the company’s sales were $4.8 billion in FY22, and in FY23, it was around $3.9 billion. The company is lagging way behind in FY23 compared to FY22, and with only one quarter remaining, I think we might see a disappointing FY23 annual result, with the company reporting sales way below FY22 sales, which can create volatility in the stock price in the next three months. Hence, I would suggest investors to remain cautious. In addition, the market environment is not looking favorable for the company; the steel prices in the U.S. are lower in FY23 compared to the previous year. So, I do not have high hopes for the upcoming quarter.

Technical Analysis

Trading View

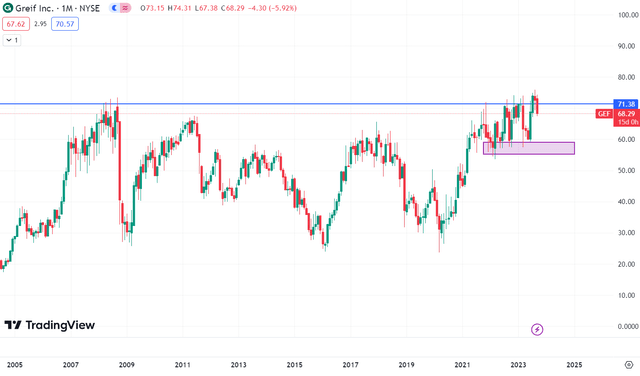

GEF is trading at $68.3. In the month of July, the stock broke its all-time high of $73.4, which the stock created in 2008. But it turned out to be a fake-out, and it is a classic case of bull trap. Now, the price has gone below the resistance level of $71. Since 2021, the stock has consolidated between the range of $56-$71. The stock used to reach $56 and rise up to $71, and when the price used to reach $71, it used to fall to the $56 level. This went on for three years, but after the recent breakout failure, I believe the stock is headed towards the $56 level. So, I believe one should avoid the stock as I see a downside of 15% from the current level.

Should One Invest In GEF?

The quarterly result has been disappointing, and the company has been underperforming in FY23 compared to FY22. Still, the stock price is trading near the all-time highs. But the recent price action has been showing early signs of reversal. The company’s financial performance hasn’t been up to the mark, and if we look at GEF’s valuation, I don’t see any value in the stock. GEF has a PEG [FWD] ratio of 1.56x compared to the sector median of 1.51x and a Price / Book ratio of 1.64x compared to the sector median of 1.58x. So, I think its valuation is on the higher side.

Additionally, I do not have high hopes for the upcoming quarter. I believe its FY23 sales might be lower than FY22 sales. Hence, considering the future outlook, weak technicals, and high valuation, I think it is better to avoid it, as I expect volatility in the stock in the coming times. Hence, I assign a hold rating on GEF.

Risk

Steel, resin, recycled coated and uncoated boxboard, containerboard, and used industrial packaging for reconditioning are the main raw materials they purchase or otherwise obtain in highly competitive, price-sensitive markets. These materials are also used in the manufacture of their products. Price and demand cyclicality have historically been present for these raw commodities. Additionally, they produce specific component parts for their own line of rigid industrial packaging solutions as well as those of a few rival companies. Some of these materials and component parts have been in short supply and could become so in the future. For instance, a significant economic downturn in the industries that supply any of those raw material requirements or competition for the use of raw materials and component parts in other regions or countries may unexpectedly disrupt the availability of these raw materials and their ability to purchase and transport these raw materials and/or produce and transport these component parts. They may continue to see considerable raw material price rises in the future, which would probably harm their operating margins. As a result, raw material costs may rise.

Bottom Line

Currently, I see no value in the company. Their financial performance has been disappointing, the price action is bearish, and the valuation seems high. I expect volatility in the stock price to be high in the coming times. Hence, I assign a hold rating on GEF.

Read the full article here