Introduction

Hochtief (OTCPK:HOCFF) is one of the world’s most recognized infrastructure group with exposure to construction, services and concessions (including public-private partnerships) and some of the best known buildings it has worked on include the Yankee Stadium and the Burj Khalifa. The last time I had a closer look at the company was in 2021 as I wanted to check up on its financial health subsequent to 2020 to see how the company was able to deal with the COVID pandemic and the fallout.

Yahoo Finance

Hochtief has its primary listing in Germany where it’s trading with HOT as its ticker symbol with an average daily volume of 75,000 shares. This means the volume in Germany is clearly superior to any other secondary listing, so the German listing should be the preferred way to trade in the company’s shares. The current market capitalization of Hochtief is approximately 7.4B EUR based on the current share price of approximately 98 EUR and the current share count of 75.2M shares (net of treasury shares). I will use the Euro as base currency throughout this article.

The company’s website mainly contains ‘download only’ links, but you can find all relevant information I will refer to here.

The cash flow: still strong

Hochtief doesn’t appear to be impacted too much by the weakening world economy as the company reported a 9% revenue increase while the net income increased by a similar percentage: this indicates the company was able to protect its margins.

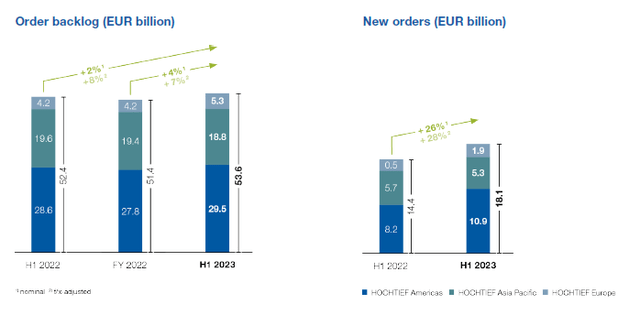

Also important was the very strong backlog increase. While the total revenue for the first half of the year was approximately 13B EUR, the company reported approximately 18.1B EUR in new orders. Not only is that an increase of 28% compared to a year ago (which further isolates Hochtief from the current economic weakness), it also is a book-to-bill ratio of almost 140%, bringing the LTM book-to-bill ratio to approximately 110%. This also resulted in a total order backlog of 53.6B EUR and excellent visibility for the next 21 months.

Hochtief Investor Relations

Long story short, as long as the current economic uncertainty doesn’t last several years, odds are Hochtief won’t even notice it as its near-term order book is pretty full anyway. So even if the order intake falls by 50% in the next year, the order book will likely remain filled until the end of 2025. And that likely is the main reason why Hochtief’s share price on the financial markets is holding up surprisingly well.

It’s not the sole reason as Hochtief’s strong margins are likely another contributor to the strong share price.

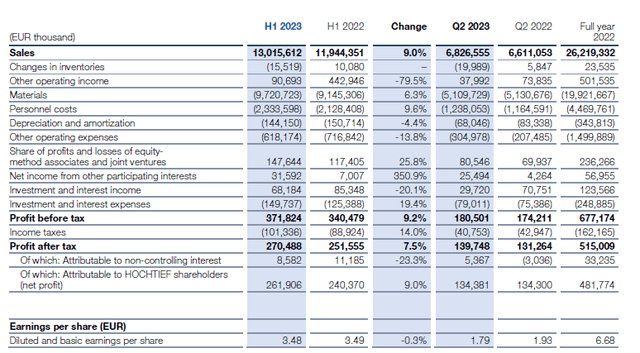

During the first half of the current financial year, Hochtief reported a total revenue of just over 13B EUR, resulting in an EBIT of approximately 450M EUR (of which 230M EUR was generated in the second quarter). This resulted in a pre-tax income of 372M EUR and a net income of 270.5M EUR of which 262M EUR was attributable to the shareholders of Hochtief.

Hochtief Investor Relations

That represents an EPS of approximately 3.48 EUR , fueled by a strong Q2 performance with an EPS of 1.79 EUR thanks to a relatively lower effective tax rate of just under 22.6% compared to 27.2% in the entire first semester.

And that’s a good result. While the EPS in Q2 was lower than in the same quarter last year, the H1 EPS was pretty stable.

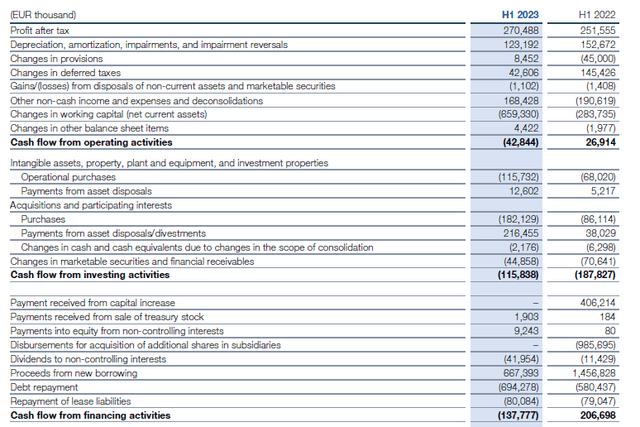

I also wanted to keep an eye on the cash flows to make sure the construction company wasn’t just booking ‘paper profits’. The reported operating cash flow in the first half of the year was a negative 43M EUR but this was mainly caused by the 659M EUR investment in the working capital. Adjusted for this, the underlying operating cash flow was 616M EUR. And after deducting the 42M EUR in dividends to non-controlling interests (this was pretty high and will likely be lower in the future) and the 80M EUR in lease payments, the adjusted operating cash flow was 494M EUR.

Hochtief Investor Relations

As you can see above, the total capex was 116M EUR in the first semester, resulting in a net free cash flow of 378M EUR. If you would also deduct the 43M EUR in deferred taxes, the underlying free cash flow was approximately 335M EUR in the first semester. That’s 4.45 EUR per share and higher than the reported net income thanks to a 8M EUR difference in capex paid versus depreciation expenses, while the income statement was negatively impacted by a 168M EUR non-cash expense.

The full-year outlook also appears to be very robust: Hochtief has confirmed its guidance for 2023 and the company still expects to generate a net profit of 510-550M EUR. Adjusted for the net income attributable to non-controlling interests, the net income attributable to Hochtief’s shareholders should be around 490-530M EUR. The midpoint of that guidance (510M EUR) would represent an EPS of approximately 6.8 EUR.

Hochtief’s dividend policy calls for a 65% payout ratio and applying that percentage to the anticipated 6.8 EUR EPS would result in a dividend of 4.4 EUR per share. This would be a 10% increase compared to the 4 EUR dividend it paid out over FY 2022. The dividend withholding tax rate in Germany is 26.375%.

Investment thesis

Hochtief’s performance in the first semester was very strong and I am pleased with the stable margins and the very strong order intake. The existing order book provides excellent visibility for almost two years and every additional order the company can secure in the current semester will further help Hochtief to get through an economic contraction without too many issues.

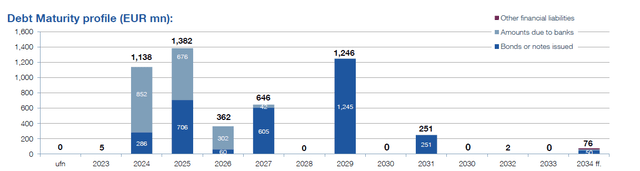

Meanwhile, the balance sheet remains very strong (the company completed a rights issue in 2022 when it also acquired full ownership of Australia-based CIMIC) and as of the end of June, the balance sheet contained a net cash position of 346M EUR (including the marketable securities). This means the upcoming bond maturity dates shouldn’t be an issue given the 4.4B EUR in cash readily available on the balance sheet. This also means Hochtief has the luxury to just repay debt as it comes due rather than being forced to pay through the nose when it comes to interest expenses.

Hochtief Investor Relations

The financial markets also don’t appear to think Hochtief is a risky investment: the yield to maturity for the 2029 bonds is currently just 4.2.

This doesn’t mean I’m a buyer at the current share price. I think the share price has moved up too fast and too high as the stock is trading at a multiple of approximately 15 times this year’s earnings and 14 for 2024 based on the analyst consensus estimates. I think the company is a ‘hold’ at best, at the current share price as even a buyout offer from its largest shareholder ACS (which currently owns about 70% of the shares) is unlikely.

I currently have no position in Hochtief. I also am not a buyer at these levels.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here