Introduction

Founded in 1989, Michigan-based Vericel (NASDAQ:VCEL) is a commercial-stage biopharmaceutical leader specializing in advanced therapies for sports medicine and severe burn care. It markets three FDA-approved products in the U.S.: MACI for knee cartilage defects, Epicel for extensive burns, and recently approved NexoBrid for eschar removal in thermal burns. Vericel primarily operates in the U.S., focusing on research, product development, and distribution of cellular therapies and specialty biologics.

Recent Developments: Vericel’s Q2 GAAP EPS of -$0.11 and revenue of $45.9M beat expectations. 2023 revenue guidance raised to $190-197M.

The following article discusses Vericel’s Q2 2023 financial performance, strong liquidity, and future growth prospects. It recommends a “Hold” stance on the stock.

Q2 Earnings Report

Looking at Vericel’s most recent earnings report, Q2 2023 total net revenue rose 24% to $45.9M, driven by MACI and Epicel revenues. Gross profit was $29.9M or 65% of net revenue, up from 62% last year. Operating expenses increased to $35.9M, mainly from higher sales and marketing and R&D costs. The company posted a net loss of $5M. Non-GAAP adjusted EBITDA was $4.4M. Vericel held $147M in cash and investments with no debt. 2023 revenue guidance was raised to $190M-$197M.

Cash Flow & Liquidity

Turning to Vericel’s balance sheet, the sum of ‘Cash and cash equivalents’, ‘Short-term investments’, and ‘Long-term investments’ amounts to $43.0M, $54.8M, and $21.0M, respectively, yielding a total of $118.8M in highly liquid assets. The “Net cash provided by operating activities” for the first six months of 2023 is $18.1M.

The company exhibits strong liquidity with $118.8M in easily accessible funds. Additionally, there’s no discernable debt on the balance sheet. Given its positive cash flow from operating activities and strong liquid asset position, securing additional financing, if required, appears feasible for Vericel . These are my personal observations, and other analysts might interpret the data differently.

Capital Structure, Growth, & Momentum

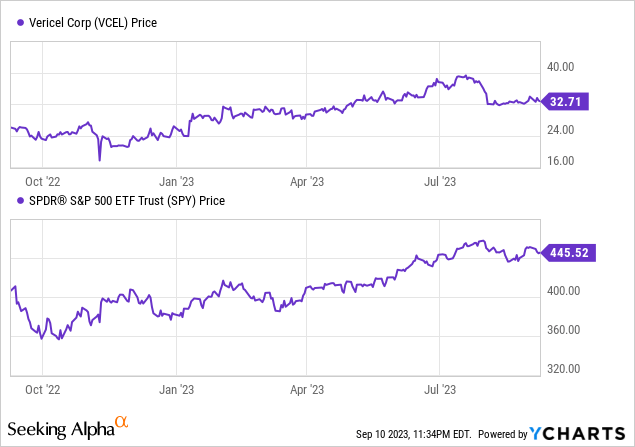

According to Seeking Alpha data, Vericel Corporation has a moderate capital structure with a balance between cash and debt levels relative to its $1.56B market cap. Its enterprise value is $1.54B. On the growth front, the company is at a commercial stage, showing promising revenue and earnings trajectory. Analysts project revenues of $239.10M and $282.46M for 2024 and 2025, respectively, which aligns with the company’s B- growth score and a consistent YoY revenue growth rate. Regarding stock momentum, Vericel has outperformed the S&P 500 in the 9M and 1Y metrics, suggesting a relatively strong market favorability.

Vericel Ups Revenue Guidance Amid Expanding Product Line

In their most recent earnings call, Vericel management expressed optimism based on strong Q2 performance, with significant revenue growth and a 12th straight quarter of positive adjusted EBITDA. They noted a 27% Y/Y growth for their MACI product, primarily driven by an expanded surgeon base and strong biopsy numbers. Management increased full-year MACI revenue guidance to $159 to $163 million, representing more than 20% growth.

Anticipating a commercial launch of arthroscopic MACI in the first half of 2024, the company highlighted positive market research suggesting this innovation could further penetrate the cartilage repair market. The research indicated surgeons find arthroscopic MACI less invasive, resulting in quicker recovery for patients.

Turning to their burn care franchise, second-quarter Epicel revenue grew by 40% QoQ and 17% YoY, driven by a higher proportion of biopsies for patients moving on to treatment. However, they also mentioned a delay in the commercial availability of NexoBrid due to a deviation in third-party testing, yet the product is still expected to contribute significantly in 2024.

Overall, management raised their 2023 total revenue guidance based on improved Epicel trends and anticipated procurement revenue from BARDA. They expect company growth to accelerate to over 20% in 2024, with contributions from new product launches.

My Analysis & Recommendation

In conclusion, Vericel demonstrates an impressive combination of prudent financial management and aggressive growth strategies. The company is sitting on a solid cash reserve with no visible debt—a testament to the management’s financial acumen. It’s worth noting that Vericel’s positive cash flow puts them in a strategic position for future capital-intensive endeavors or acquisitions, should they choose to go that route.

Focusing on the growth opportunities, Vericel is not just riding on current portfolio strengths but also has an eye on the future. The market for cartilage repair is evolving, and the anticipated 2024 launch of arthroscopic MACI could offer a less invasive treatment, potentially enlarging their market share in this segment. On the burn care side, despite setbacks in NexoBrid’s availability, the product promises to be a game-changer, adding to Epicel’s already strong performance.

Investors should particularly watch for:

- The commercial launch of arthroscopic MACI—this could be a market disruptor.

- The resolution of the third-party testing delay for NexoBrid as this could be a significant revenue generator in 2024.

Given these dynamics, it’s hard to argue against the company’s robust portfolio and savvy management, making it a compelling option in the biopharmaceutical sector. Based on the current valuation and upcoming growth catalysts, my advice would be a “Hold” for Vericel. The company appears fairly valued at these prices; however, it could become a more attractive buying opportunity if the market provides a dip or if upcoming product launches exceed expectations.

Read the full article here