Introduction

Ares Management Corporation (NYSE:ARES) is a global investment management company (it has 30 offices across 15 countries in North America, Europe, APAC, and the Middle East) that specializes in the alternative investment space. ARES offers its clients (predominantly institutions) a range of investment strategies across different but complementary asset classes, namely credit (this is the bread-and-butter, accounting for over 60% of group AUM), private equity, real estate, and infrastructure assets.

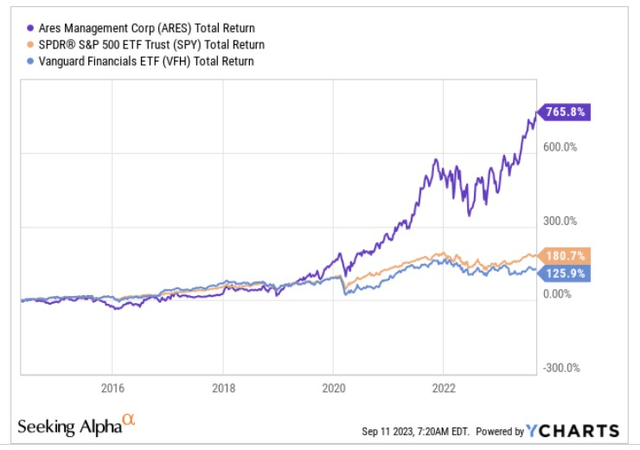

ARES came to the bourses nearly 10 years ago, in early May 2014; since then, it’s proven to be an astounding source of alpha, delivering over 4x the returns of the S&P 500, and over 6x the returns of the Vanguard Financials ETF.

YCharts

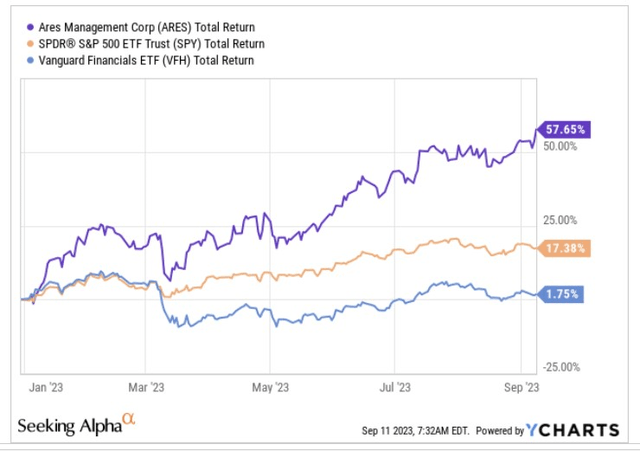

Even this year, when the markets have been so volatile, and the financial sector has received plenty of negative press, ARES’s stock has coasted along without too many hiccups, delivering ~58% on a YTD basis, and beating both the markets and its financial peers quite handsomely. Why does the market like this stock so much?

YCharts

ARES – A Lot To Admire

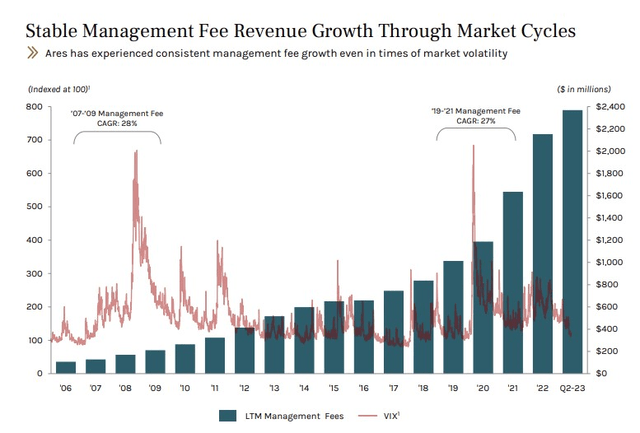

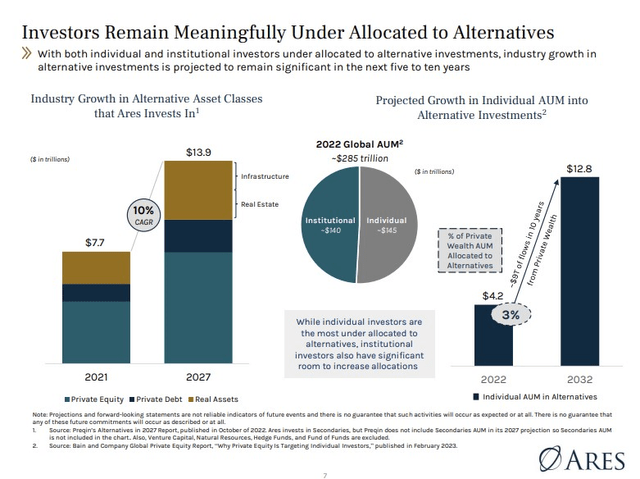

Investor Presentation – Aug 2023

We know that the market is prepared to pay top dollar for stable businesses, and ARES- it’s fair to say – has been a beacon of stability for many years now. Regardless of the volatility threshold in the markets at any point in time, note that ARES’s management fees never goes through a blip. For context, during some of the most volatile periods in recent decades, such as the GFC or even during COVID, management fees were growing at impressive rates of 27-28%. Also, ARES is significantly exposed to credit funds, and here so long as credit fundamentals are robust, one tends to get predictable growth in fee income. Speaking of credit, also note that portfolio quality remains top-notch, despite an increase in policy rates in recent periods. For context, in Ares Capital Corporation (a proxy for ARES’s US direct lending business), the non-accruals ratio continues to trend well below the 15-year average).

Investor Presentation – Aug 2023

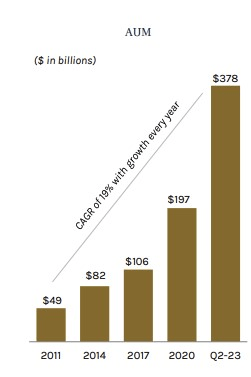

ARES’s management fees are predominantly a function of the AUM that the firm has accumulated over time, and here too ARES has done well to attract the attention of investors with the AUM metric growing at a CAGR of 19% from 2011. For context note that the AUM across the entire industry (be it within the North American region, Western Europe, or even Asia Pac) during this similar period has largely only come in at 10-14%. Currently, ARES has around $378bn of AUM, and hopes to get to $500bn of AUM by 2025, which would represent around 15% CAGR going forward. Hitherto much of ARES’s growth has come from the institutional segment, but don’t dismiss the prospective firepower of the retail segment, as they are still heavily underexposed to the “alternative investment” universe (currently only 3% of private wealth AUM is deployed in the alternative space). It is believed that over the next 10 years, the private retail AUM here could expand by 3x and hit $12.8bn!

Investor Presentation – Aug 2023

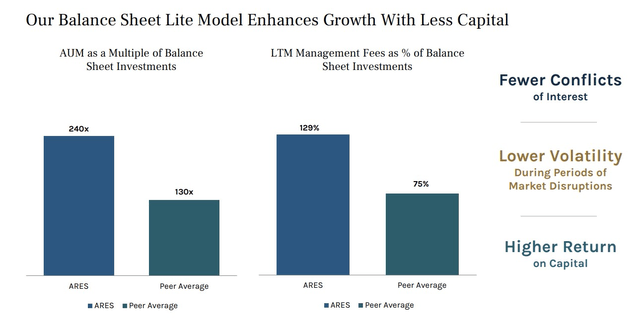

Also note that ARES’s AUM growth is such, that it currently stands at over 240x the level of balance sheet investments; this positioning is almost twice as much as what the industry sees. Also, an overwhelming majority of the AUM is linked to long-dated funds or perpetual capital that only boosts the stability quotient of ARES’s capital.

Investor Day Presentation

When you have such a sticky AUM base, you become less susceptible to the vagaries of the market and thus are better positioned to generate asset and management fee growth.

Investor Day Presentation

What investors also need to recognize is that ARES isn’t predominantly growing its AUM by accumulating new investors over time; rather, -and this speaks to the general stickiness of institutional customers in ARES’s business – over 92% of their institutional fundraising, comes from either those institutions that signed up for a new product or lifted their financial commitments to a subsequent fund vintage within the same product. It certainly also helps that there’s a greater sense of agency associated with ARES investment ethos as the firm and its professionals also invest capital in the funds that they sponsor and manage. Needless to say, when there’s skin in the game, you bring an added degree of credibility to the business.

Currently, ARES also has a substantial “shadow AUM” arsenal (growing at 20% CAGR- Source: Investor Day Financial Review) or AUM that is waiting to be deployed for future fee-generating potential. Management noted that the deployment pipeline has been trending up over the past three quarters, and when there’s greater visibility on the Fed’s terminal rate, expect this to pick up.

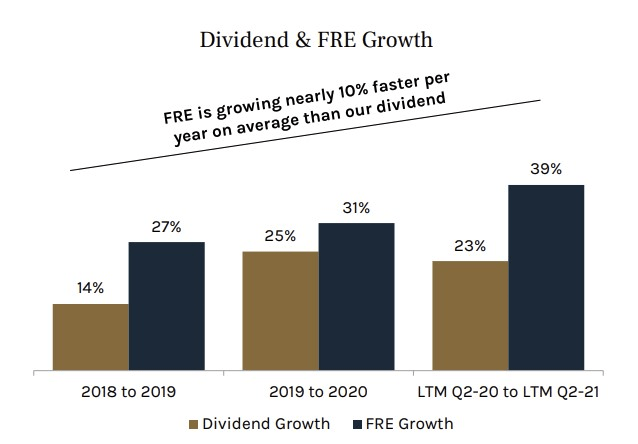

One also needs to consider the stellar dividend narrative associated with this business. Most businesses in the financial sector grow their dividends at a mid-single digit to high-single digit pace, but in FY22 and this year, ARES has grown its quarterly dividends at an impressive 30% and 26% respectively. Going forward, management has confirmed that dividends will grow at 20% over the next two years. It’s unusual for a company to have such strong confidence in its dividend outlook, and this stems from the fact that ARES’s dividends are closely linked to its post-tax fee-related earnings (FRE) which are a lot more stable (compared to performance-related income which can oscillate YoY based on a whole host of variables) and comfortably cover the dividend.

Investor Day Presentation

Of late ARES has been doing well to control its G&A expenses and compensation ratio which has helped boost the FRE margin from levels of 28% in FY17 to 40.3% as of Q2. Looking ahead, ARES expects its FRE growth to come in at impressive levels of 20% through FY25, making the dividend even more safe.

Forward Earnings and Valuations

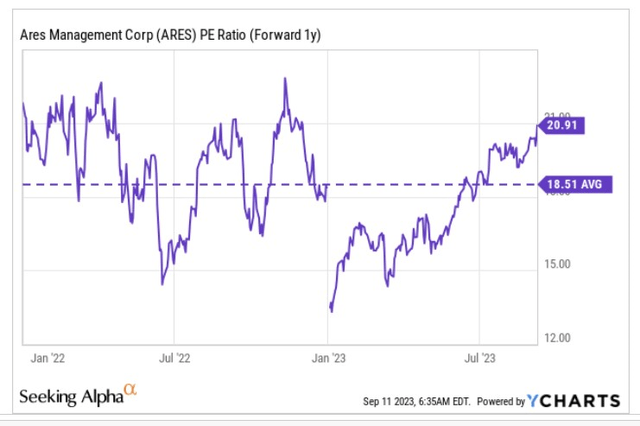

Prima facie, it would appear that ARES’s stock is not a cheap stock to own, trading at 21x forward P/E (based on the FY24 EPS), a 13% premium to its 5-year average multiple.

YCharts

Having said that, it may also be worth questioning if a 13% premium is too prohibitive, particularly when you consider the medium-term earnings growth you could be getting at that multiple.

Well, as covered previously, at the heart of ARES’s operating model is this relentless high-growth fee-based income line, and the benefit of having such a profound fee-based cog is that the conversion to the net income level tends to be very high. Now according to YCharts estimates, over the next two years (FY24 and FY25), ARES is on course to deliver impressive YoY earnings growth of 35% on average. Sure 21x P/E is not cheap, but when you learn that you’d be getting 35% earnings growth (an implied PEG ratio of only 0.6x) two years on the trot, that certainly makes the valuation picture look a lot more palatable.

Closing Thoughts – Is Ares A Good Buy Now?

Even though there’s a lot to like about ARES, developments on the charts and recent stakeholder positioning suggest that it wouldn’t be the most opportune time to get in.

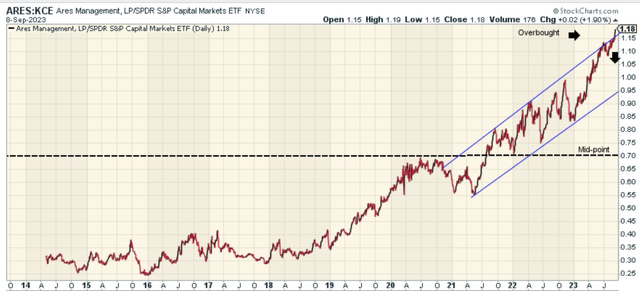

The chart below seeks to ascertain if ARES could benefit from some rotational interest from prospective investors who are fishing in the capital markets universe.

StockCharts

For ARES to make the rotational watch list, one would need to see the current ratio trading well towards the lower end of the chart, with a substantial gap from the mid-point of its long-term range. Conversely, not only is the relative strength ratio at record highs, but it is also trading well above the upper boundary of its ascending channel (two blue lines), giving one a sense of how overbought it looks currently. In light of this status quo, we wouldn’t be surprised to see some investors rotate out of ARES into other undervalued plays in the capital markets universe.

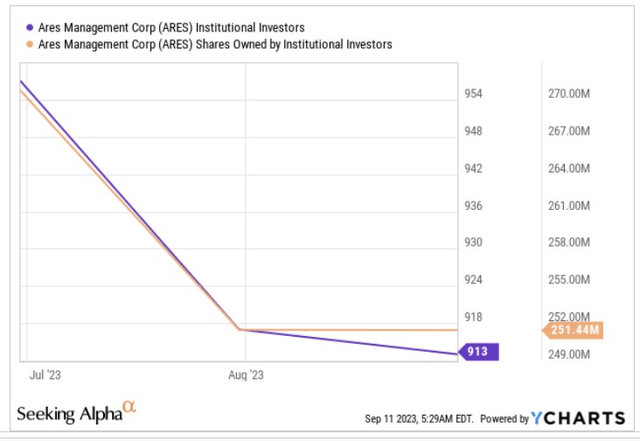

In fact, you’d be interested to know that the smart money has already started trimming its positions in ARES. Data from YCharts show that over the past three months, the number of institutions owning ARES’s stock is down by -5%, whilst the net shares owned by them are down by a larger margin of -7%.

YCharts

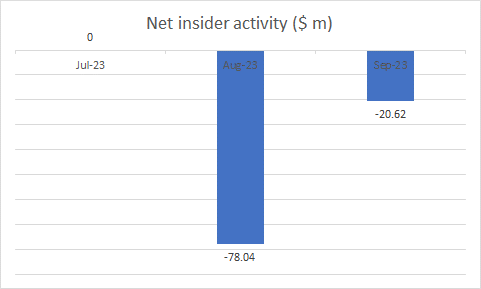

It isn’t just the institutions; if one scours the insider transaction page for discretionary trades, you’d note that after no transactions whatsoever in July, notable insiders (including the founders) sold large quantities of the shares in August (there was only one insider purchase worth less than $1m), with the selling carrying on in September as well.

Barcharts

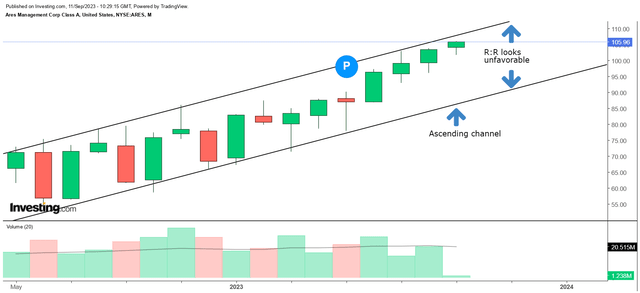

Finally, if one looks at ARES’s own price imprints on the monthly timeframe, we can see that over the last 17 months, the stock has been trending up within an ascending channel. Over the last four months, we’ve seen a series of green-bodied candles (implying that the close was higher than the open), but now the price is on the cusp of hitting the upper boundary of the channel, thus dampening the allure of a prospective long position. Thus given the sub-par reward-to-risk we would rate the stock as a HOLD.

Investing

Read the full article here